Dear Fellow Shareholders,

Across the globe, 2022 was another year of significant challenges: from a terrible war in Ukraine and growing geopolitical tensions — particularly with China — to a politically divided America. Almost all nations felt the effects of global economic uncertainty, including higher energy and food prices, mounting inflation rates and volatile markets, and, of course, COVID-19’s lingering impacts. While all these experiences and associated turmoil have serious ramifications on our company, colleagues, clients and the countries in which we do business, their consequences on the world at large — with the extreme suffering of the Ukrainian people and the potential restructuring of the global order — are far more important.

As these events unfold, America remains divided within its borders, and its global leadership role is being challenged outside of its borders. Nevertheless, this is the moment when we should put aside our differences and work with other Western nations to come together in defense of democracy and essential freedoms, including free enterprise. During other times of great crisis, we have seen America, in partnership with other countries around the globe, unite for a common cause. This is that moment again, when our country needs to work across public and private sectors to lead while improving American competitiveness — which also means re-establishing the American promise of providing equal access to opportunity for all. JPMorgan Chase, a company that historically has worked across borders and boundaries, will do its part to ensure the global economy is safe and secure.

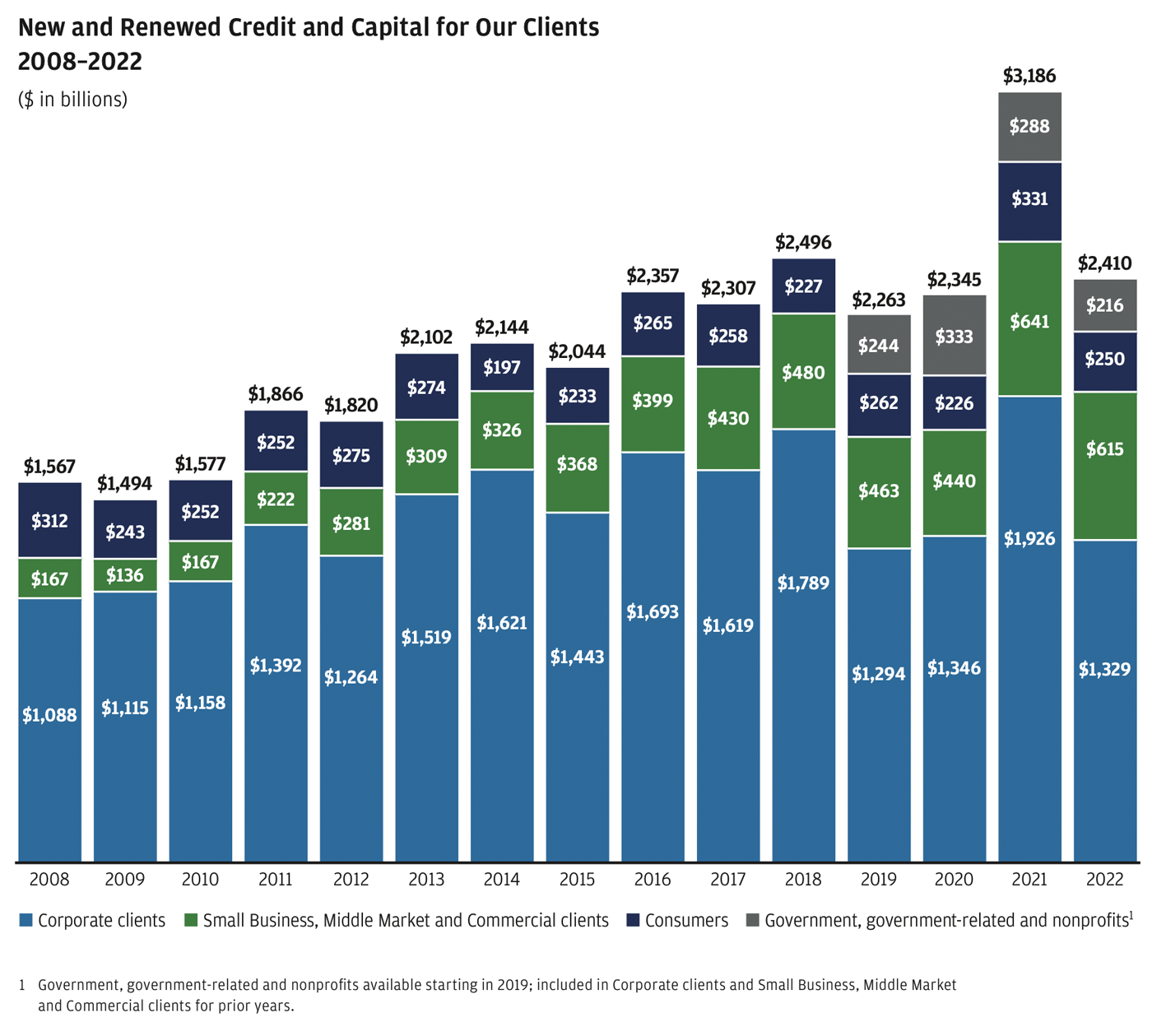

In spite of the unsettling landscape, 2022 was somewhat surprisingly another strong year for JPMorgan Chase, with the firm generating record revenue for the fifth year in a row, as well as setting numerous records in each of our lines of business. We earned revenue in 2022 of $132.3 billionReturn to footnote1 and net income of $37.7 billion, with return on tangible common equity (ROTCE) of 18%, reflecting strong underlying performance across our businesses. We also maintained our quarterly common dividend of $1.00 per share and continued to reinforce our fortress balance sheet. We grew market share in several of our businesses and continued to make significant investments in products, people and technology while exercising strict credit discipline. In total, we extended credit and raised capital of $2.4 trillion for our consumer and institutional clients around the world.

I remain proud of our company’s resiliency and of what our hundreds of thousands of employees around the world have achieved, collectively and individually. Throughout these challenging past few years, we never stopped doing all the things we should be doing to serve our clients and our communities.

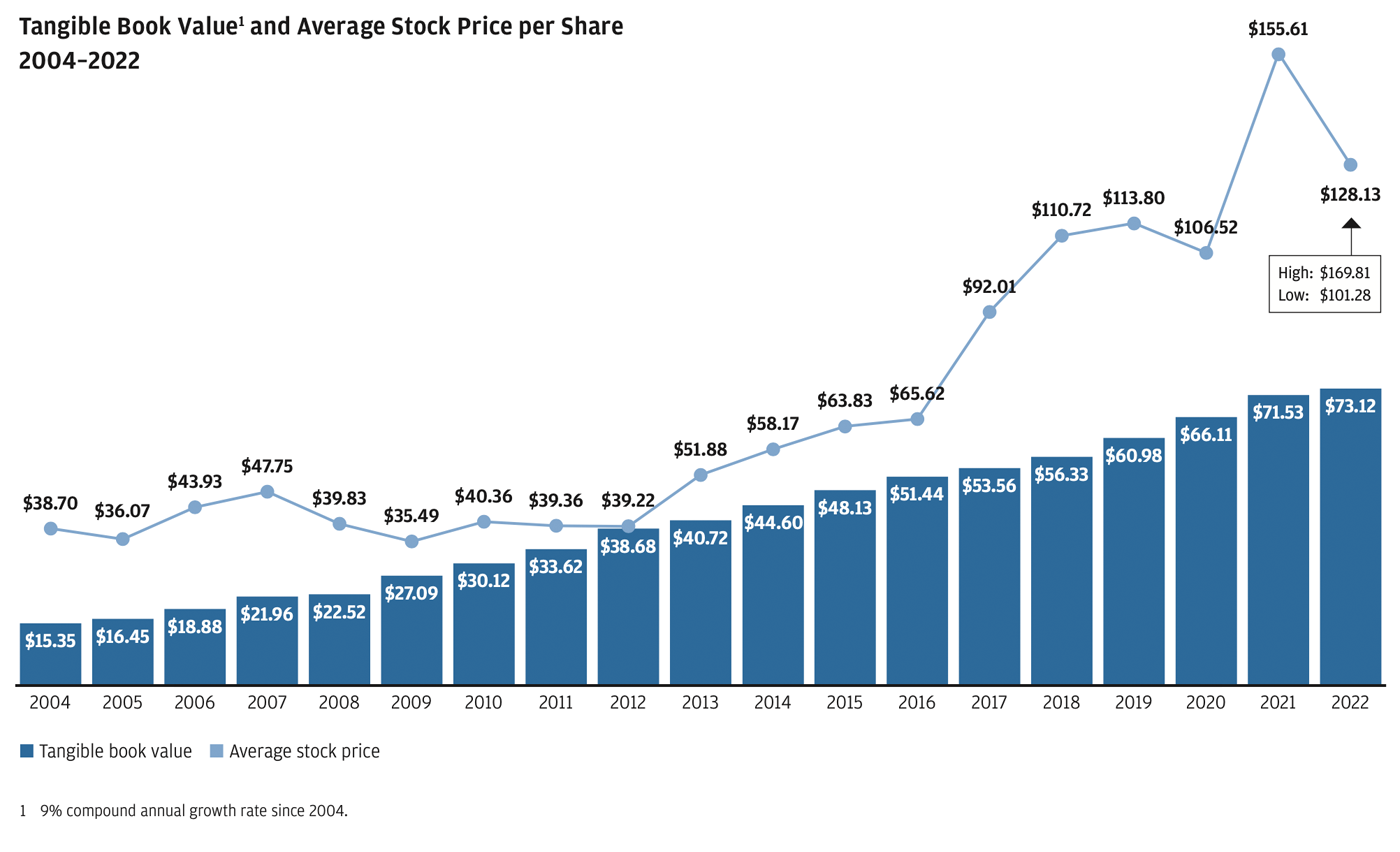

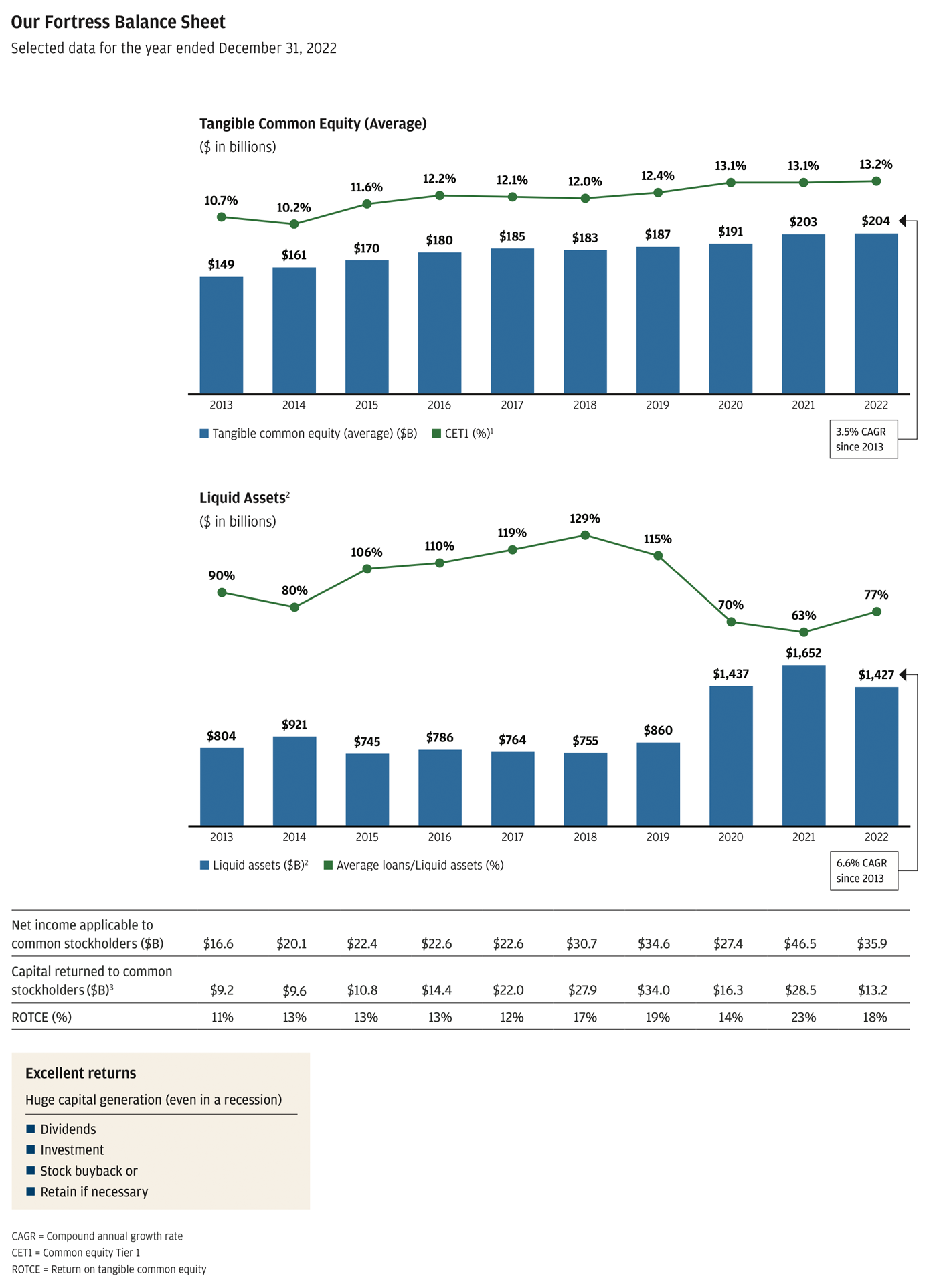

Adhering to our basic principles and strategies (see sidebar on Steadfast Principles below) allows us to drive good organic growth and properly manage our capital (including dividends and stock buybacks), as we have consistently demonstrated for decades. Our performance results are shown in the charts below, which illustrate how we have grown our franchises, how we compare with our competitors and how we look at our fortress balance sheet. I invite you to peruse them at your leisure. In addition, I urge you to read the CEO letters in this Annual Report, which will give you more specific details about our businesses and our plans for the future.

As you know, we are champions of banking’s essential role in a community — its potential for bringing people together, for enabling companies and individuals to attain their goals, and for being a source of strength in difficult times. As I often remind our employees, the work we do matters and has impact. We help people and institutions finance and achieve their aspirations, lifting up individuals, homeowners, small businesses, larger corporations, schools, hospitals, cities and countries in all regions of the world.

STEADFAST PRINCIPLES WORTH REPEATING

Looking back on the past two+ decades — starting from my time as CEO of Bank One in 2000 — there is one common theme: our unwavering dedication to help clients, communities and countries throughout the world. It is clear that our financial discipline, constant investment in innovation and ongoing development of our people are what enabled us to achieve this consistency and commitment. In addition, across the firm, we uphold certain steadfast tenets that are worth repeating.

First, our work has very real human impact. While JPMorgan Chase stock is owned by large institutions, pension plans, mutual funds and directly by single investors, in almost all cases the ultimate beneficiaries are individuals in our communities. More than 100 million people in the United States own stock; many, in one way or another, own JPMorgan Chase stock. Frequently, these shareholders are veterans, teachers, police officers, firefighters, healthcare workers, retirees or those saving for a home, education or retirement. Often, our employees also bank these shareholders, as well as their families and their companies. Your management team goes to work every day recognizing the enormous responsibility that we have to all of our shareholders.

Second, shareholder value can be built only if you maintain a healthy and vibrant company, which means doing a good job of taking care of your customers, employees and communities. Conversely, how can you have a healthy company if you neglect any of these stakeholders? As we have learned over the past few years, there are myriad ways an institution can demonstrate its compassion for its employees and its communities while still upholding shareholder value.

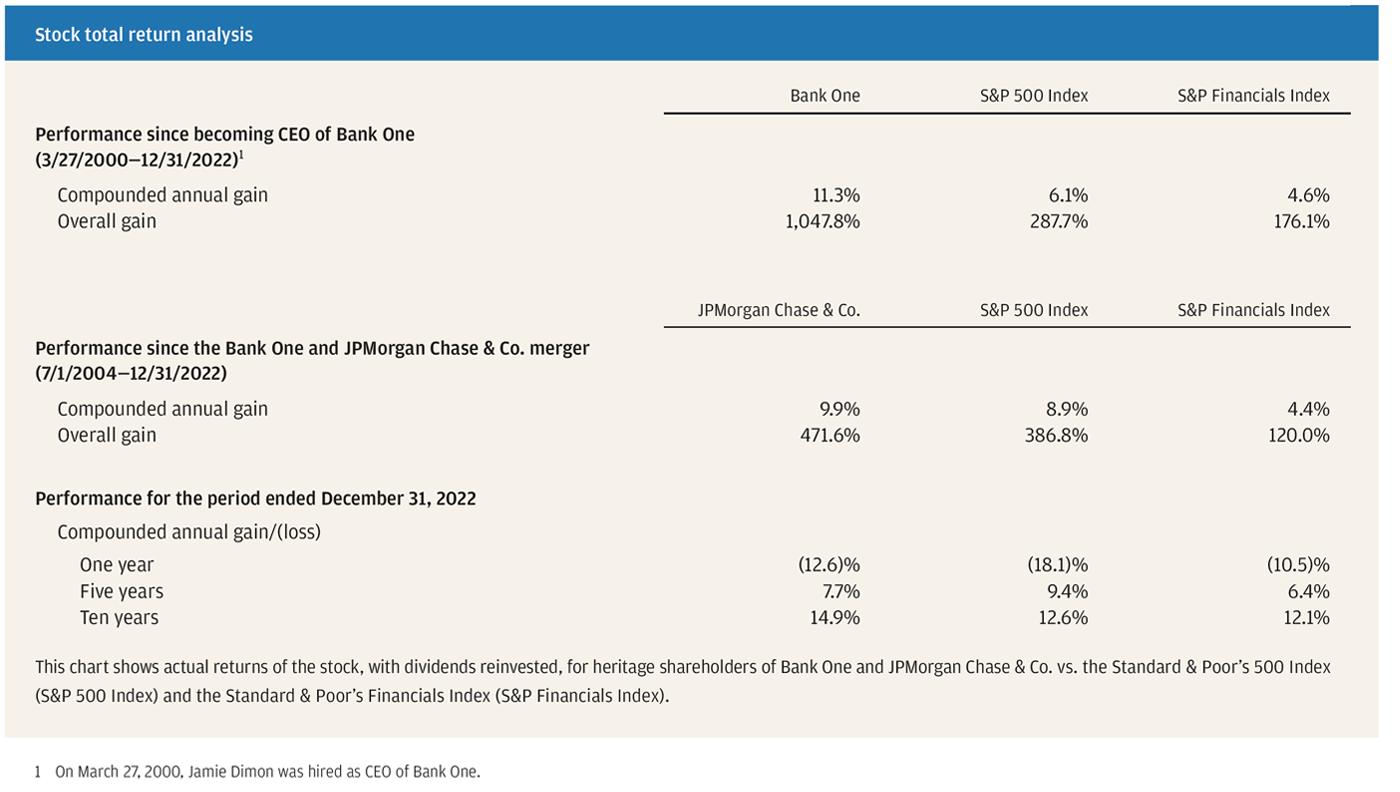

Third, while we don’t run the company worrying about the stock price in the short run, in the long run we consider our stock price a measure of our progress over time. This progress is a function of continual investments in our people, systems and products, in good and bad times, to build our capabilities. These important investments will also drive our company’s future prospects and position it to grow and prosper for decades. Measured by stock performance, our progress is exceptional. For example, whether looking back 10 years or even farther to 2004, when the JPMorgan Chase/Bank One merger took place, we have significantly outperformed the Standard & Poor’s 500 Index and the Standard & Poor’s Financials Index.

Fourth, we are united behind basic principles and strategies (you can see the How We Do Business principles on our website) that have helped build this company and made it thrive — from maintaining a fortress balance sheet, constantly investing and nurturing talent to fully satisfying regulators, continually improving risk, governance and controls, and serving customers and clients while lifting up communities worldwide. This philosophy is embedded in our company culture and influences nearly every role in the firm.

Fifth, we strive to build enduring businesses, which rely on and benefit from one another, but we are not a conglomerate. This structure helps generate our superior returns. Nonetheless, despite our best efforts, the walls that protect this company are not particularly high — and we face extraordinary competition. I have written about this reality extensively in the past and cover it again in this letter. We recognize our strengths and vulnerabilities, and we play our hand as best we can.

Sixth, we operate with a very important silent partner — the U.S. government — noting as my friend Warren Buffett points out that his company’s success is predicated upon the extraordinary conditions our country creates. He is right to say to his shareholders that when they see the American flag, they all should say thank you. We should, too. JPMorgan Chase is a healthy and thriving company, and we always want to give back and pay our fair share. We do pay our fair share — and we want it to be spent well and have the greatest impact. To give you an idea of where our taxes and fees go: In the last 10 years, we paid more than $43 billion in federal, state and local taxes in the United States and almost $19 billion in taxes outside of the United States. We also paid the Federal Deposit Insurance Corporation over $10 billion so that it has the resources to cover failure in the American banking sector. Our partner — the federal government — also imposes significant regulations upon us, and it is imperative that we meet all legal and regulatory requirements imposed on our company.

Seventh and finally, we know the foundation of our success rests with our people. They are the frontline, both individually and as teams, serving our customers and communities, building the technology, making the strategic decisions, managing the risks, determining our investments and driving innovation. However you view the world — its complexity, risks and opportunities — a company’s prosperity requires a great team of people with guts, brains, integrity, enormous capabilities and high standards of professional excellence to ensure its ongoing success.

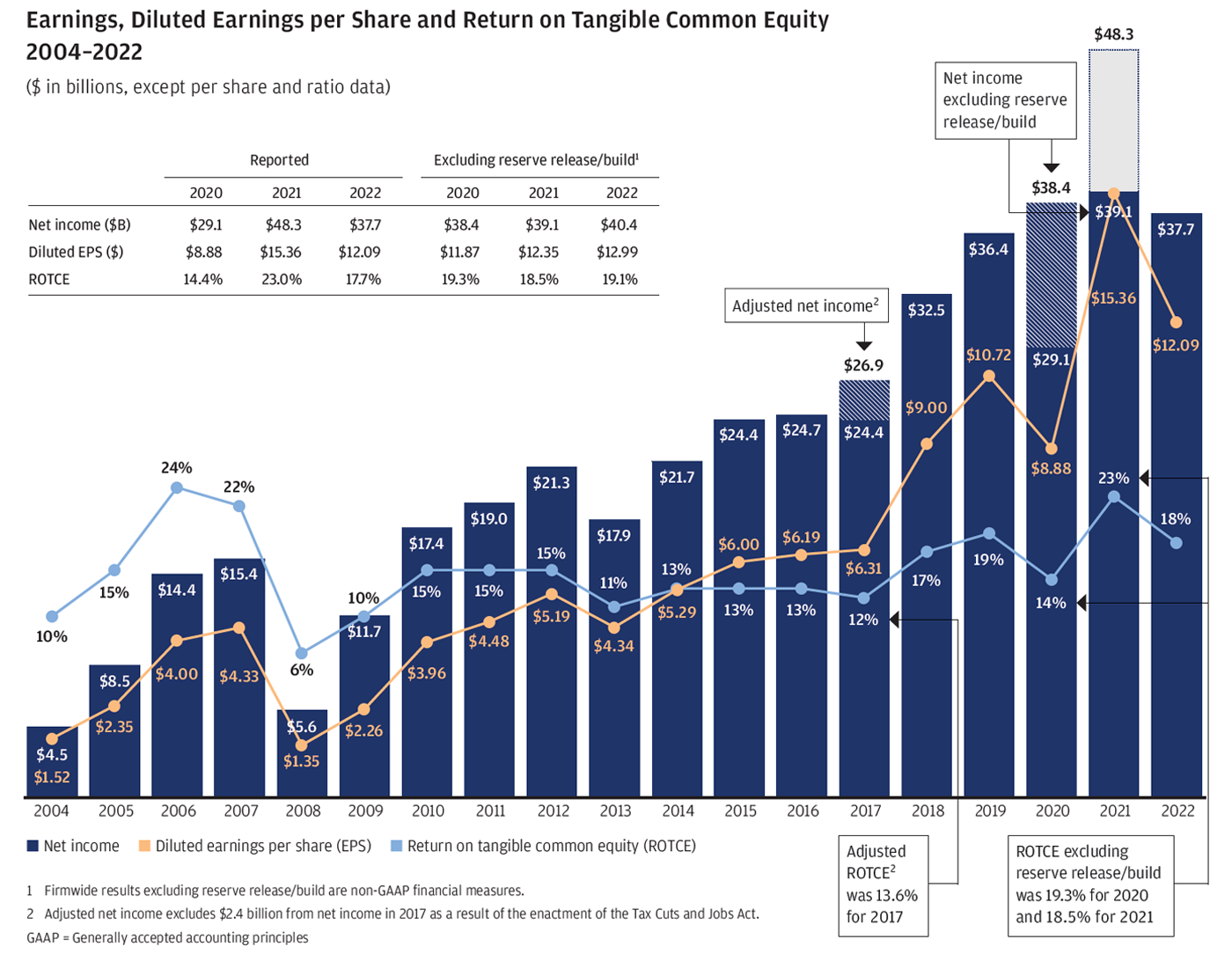

*An important note to describe why we are showing the table above: The loan loss reserve accounting rules — which are life-of-loan estimated losses based upon probability-based economic scenarios — generate huge swings in earnings that can be unrelated to actual credit performance. This was particularly true for the COVID-19 years when, during the first six months of the pandemic, we built approximately $16 billion in reserves. Then in the next six quarters, we released essentially the equivalent number. We did so only because the scenarios used to estimate future credit losses changed dramatically.

The table above shows reported net income, with and without loan loss reserve changes. Throughout this period, the credit portfolio was healthy, and charge-offs remained below pre-pandemic levels. Either way, the company had strong absolute and relative performance.

Read footnoted information here

Read footnoted information here

Read footnoted information here

Within this letter, I discuss the following:

Why We Are Proud of JPMorgan Chase

- United by principles and purpose

- Our purpose

- Highlighting our diversity, equity and inclusion efforts

- The state of Ohio: How JPMorgan Chase drives community growth

Update on Specific Issues Facing our Company

- Climate complexity and planning

- AI, data and our journey to the cloud

- Banking turmoil and regulatory goals

- Adjusting our strategy to the new regulatory reality (Basel III Endgame)

- Keeping an eye on all of our competitors

- Building true franchise value

- Learning from Investor Day

- Balancing a customer-centric approach with (excessive) risk

Some Commonsense Principles for Corporate Governance

- Promoting open communication and trust with the board

- Confronting succession planning

- Active engagement with asset managers

Evaluating and Managing the Economic and Geopolitical Risks Ahead

- The current economy: Pretty good but storm clouds ahead

- Potential trouble brewing from unprecedented fiscal spending, quantitative tightening and geopolitical tensions

- Preparing for what may be a new and uncertain future

Our Serious Need for More Effective Public Policy and Competent Government

- Developing effective policy and effective government

- The Wall Street Journal Op-Ed: “The West Needs America’s Leadership”

- Creating a comprehensive global economic strategy

Why We Are Proud of JPMorgan Chase

Our vision is simple and unchanged: We aim to be the most respected financial services firm in the world, serving corporations and individuals. To that end, it is imperative that we run a healthy, vibrant and responsible company. In addition to traditional banking, we do a lot to help the communities in which we operate, which, in turn, provides the foundation for increased opportunity and prosperity for all. And just to note, while we are proud of the good things we do every day, we are also an organization that acknowledges the mistakes we make along the way, which is important to do. And when we do make mistakes, we own up to them, learn from them and then move on.

UNITED BY PRINCIPLES AND PURPOSE

We’ve always had — and published — principles to guide how we do business, with values embedded within them, which I described in the preceding section. These tenets unite our company across the globe. To complement these guidelines, we recently developed a clearly stated purpose — Make dreams possible for everyone, everywhere, every day — to knit together our values with our everyday business principles and explain how we have done business for years.

While our company has a rich history, is proud of the critical role it plays in powering economic growth and has done exceptionally well over the past 200 years, research has shown that purpose-driven companies achieve stronger business results and have greater impact by doing better for their customers, employees and shareholders. Our intention in documenting our purpose for ourselves is to help energize our employees, differentiate our company from our competitors, and push our organization to innovate on behalf of our clients, colleagues and communities. In addition, we are launching a new effort — internally and externally — to showcase how the work we do matters and has tangible impact locally and around the world.

In detailing the elements of our purpose, shown in the following sidebar, we have tried to make every word meaningful.

We are also dedicated to corporate responsibility, and our efforts extend far beyond significant philanthropic contributions (which total more than $350 million a year globally). For example, at the local level, we support educational institutions and work-skills training programs around the world, as well as finance affordable housing and small businesses. In addition, we help formulate broad-based policies that are good for countries on issues such as healthcare, infrastructure, education and employment. Sometimes we promote specific initiatives; for example, programs that help individuals with a criminal background get a second chance. Lest anyone think that I’ve become a little soft, rest assured your CEO is a red-blooded, patriotic, free-enterprise and free-market capitalist (properly regulated, of course) and finds nothing inconsistent with the multifaceted ways we use our capabilities to lift up our communities.

Part of our corporate responsibility efforts are focused on progress toward diversity, equity and inclusion (DEI), which is detailed in the sidebar below shows how our work on the ground translates to a particular geography, in this case the state of Ohio.

HIGHLIGHTING OUR DIVERSITY, EQUITY AND INCLUSION EFFORTS

We seek to create a company that reflects the diverse communities that we serve, a workplace in which all employees feel they belong and are respected. We believe these efforts not only make us a positive work environment, but they also make our company stronger, our business more profitable and our institution a better global corporate citizen. This objective is integrated into how we do business every day. Some of our recent progress is highlighted below:

- We continue to identify ways to support our military veterans. In 2011, along with 10 other companies, JPMorgan Chase co-founded the Veteran Jobs Mission (VJM), a coalition committed to hiring at least 100,000 veterans by 2020. Since its founding, more than 300 member companies representing various industries across the United States have reported over 880,000 veteran hires. In 2022, VJM increased its goal to 2 million veteran hires and 200,000 military spouse hires over the next decade. JPMorgan Chase alone has hired over 18,000 veterans since 2011 and currently employs approximately 3,000 military spouses.

- We continue to make strides in developing a diversified workplace. By year-end, women represented 49% of the firm’s total workforce. Overall, Hispanic, Asian and Black representation grew to 21%, 18% and 14%, respectively. In 2022, the number of employees who self-identified as LGBTQ+ increased by 35% year over year, following 50% year-over-year growth in 2021.

- The firm’s Office of Disability Inclusion (ODI) continues to lead strategy and initiatives aimed at advancing careers while helping the firm be a bank of choice for people with disabilities. As ODI kicked off its business growth and entrepreneurship work in 2022, it provided business coaching to over 225 entrepreneurs with disabilities and commissioned research with the National Disability Institute, which identified unique opportunities and challenges among small business owners who have a disability.

An update on our $30 billion racial equity commitment

What began in 2020 as a $30 billion, five-year commitment is now transforming into a consistent business practice that our lines of business deliver each day to support Black, Hispanic, Latino and other underserved communities.

By the end of 2022, we reported nearly $29 billion in progress toward our original goal. But our focus is not on how much money is deployed — it is on long-term impact and outcomes.

Here are some details on our program’s progress through 2022:

- Supplier diversity. In 2022, our firm spent approximately $2.1 billion directly with diverse suppliers — an increase of 25% over 2021. As a part of our racial equity commitment, $400 million was spent in 2022 with over 200 Black-, Hispanic- and Latino-owned businesses — more than doubling the amount spent in 2021.

- Affordable rental housing. Through our Affordable Housing Preservation program, we approved funding of approximately $18 billion in loans to incentivize the preservation of nearly 170,000 affordable housing rental units across the United States. Additionally, we financed approximately $4 billion for the construction and rehabilitation of affordable rental housing.

- Homeownership. In a rising rate environment, we continue our efforts to provide homeownership opportunities for Black, Hispanic and Latino households across all income levels, including advocating for policies that reduce barriers to owning a home. The biggest barriers are upfront cash for a down payment and closing costs. In 2022, we expanded our $5,000 Chase Homebuyer Grant program to include over 11,000 majority Black, Hispanic and Latino communities. Since our grant program began in 2021, we have provided about 2,700 grants totaling $13.5 million. We have also assisted Black, Hispanic and Latino homeowners with 11,500 incremental home loans together worth over $4 billion, mainly driven by refinance activity when rates were low.

- Small business. In 2022, we launched a Special Purpose Credit Program, the first of its kind nationally, to expand credit access for small businesses in majority Black, Hispanic and Latino communities, which have traditionally been underserved. When I visited Houston last year, I met Sherice and Steve Garner, Chase customers who own a local barbecue business, Southern Q. They are examples of the types of customers we want to support. Previously, they had been using their personal bank account to run their business. We helped them secure a small business loan to purchase their business location. To assist more families like the Garners, we hired 45 local senior business consultants to provide one-on-one coaching and host educational events, community workshops and business training seminars to support minority entrepreneurs across 21 U.S. cities.

- Minority depository institutions (MDI) and community development financial institutions (CDFI). We invested more than $100 million in equity in diverse financial institutions and provided over $200 million in incremental financing to CDFIs to support communities that lack access to traditional financing. We also helped them build their capacity so they can provide a greater number of critical services like mortgages and small business loans. Additionally, we do not charge a fee for nearly all our participating MDI and CDFI customers who make a withdrawal at a Chase ATM.

- Access to banking. We helped more than 400,000 customers open low-cost checking accounts; we’ve also opened 13 Community Center branches (a total of 15 Community Center branches since 2019), often in areas with larger Black, Hispanic and Latino populations; and we hired over 140 Community Managers in underserved communities to build relationships with community leaders, nonprofits and small businesses. These Community Center branches are unique spaces in the heart of urban communities with more space than standard bank branches to host local events, small business mentoring sessions and financial health seminars. The majority were built with minority contractors from the community; we hire staff locally and we engage local artists to help ensure these locations complement their neighborhood. We have been pleased by the dramatic positive effect these specialized branches have had on their communities to date and expect to expand the program.

By driving inclusive economic growth, we can help create a brighter future for all, no matter where people live or the circumstances they’re born into. We provide regular updates on our corporate website about our progress toward equity and equality, and I encourage you to read about the meaningful impact we’re making within our firm and with the people we serve.

THE STATE OF OHIO: HOW JPMORGAN CHASE DRIVES COMMUNITY GROWTH

When JPMorgan Chase does business in a community, we do more than just open branches. We lend to small, midsized and big businesses; we hire, pay well and provide great benefits; and we finance hospitals, schools, grocery stores, homes, automobiles and governments. For more than 200 years, this approach has enabled us to make investments that have a lasting impact on local economies, families and neighborhoods while also supporting them in good and challenging times.

We have been in Ohio since 1812, and our experience there serves as a great example of how our resources drive growth on the ground.

Our support to government, higher education, healthcare and nonprofit organizations:

- We serve approximately 150 government, higher education, healthcare and nonprofit clients throughout the state, and over the last five years, we provided nearly $9 billion in credit and capital to them.

- Our clients range from University Hospitals Health System, Inc. to the Ronald McDonald House in Columbus and the University of Dayton in Dayton.

- We are the primary treasury bank for Ohio State University and the primary bank for the city of Columbus; we also bank nearly 50 counties, cities and school districts across the state.

Our support to investment and middle market banking clients:

- Our support includes $120 billion in credit and capital over the last five years for Commercial & Industrial clients such as energy, retail and auto businesses.

- We have over 4,800 large and midsized clients in Ohio, up over 70% compared with 2019, which also includes emerging middle market companies owned by veterans, women, LGBTQ+ individuals and people of color. This gives us leading market shares in the state compared with other banks.

Our support to local financial firms:

- We have provided nearly $20 billion in credit and capital over the last five years for financial institutions such as local banks, insurance companies, asset managers and securities firms.

- Importantly, we bank 19 of Ohio’s regional, midsized and community banks, helping them serve local communities and accomplish their other goals.

Our support to small businesses:

- By the end of 2022, loan balances for small business customers in Ohio totaled over $800 million — funds being used to run and grow companies and create jobs.

- Includes support for distribution of the federal government’s Paycheck Protection Program (PPP) to help small businesses navigate the pandemic in 2020 and 2021

- In 2022 alone, JPMorgan Chase helped over 160,000 small businesses thrive and grow through access to customers, capital and networks, giving us the second largest business banking market share in the state. We also offered some 106,000 hours of advice and support to small businesses.

Our support to consumer banking needs:

- We operate nearly 225 branches and over 530 ATMs across the state.

- To help Ohioans build wealth and be financially healthy, we have provided more than 4 million savings, checking and credit card accounts, enabling these consumers to gain access to resources such as free financial health services, as well as mortgage and auto loans.

- Ranked as the second largest provider of consumer banking in Ohio with over 2 million checking and savings accounts and customer deposits totaling nearly $37 billion in 2022

- In 2022, we oversaw more than $20 billion in investment and annuity assets for clients.

Our business and community investments:

- The firm’s national $30 billion racial equity commitment takes place very specifically on the ground. Since the program began, we have committed more than $260 million across the state, including:

- Over $163 million in loans for Black, Hispanic and Latino households to purchase or refinance a home

- $54 million financed through investments and loans for the construction and rehabilitation of affordable housing

- $14 million in New Markets Tax Credit investments to support the Ronald McDonald House Charities in central Ohio

- Over $12 million spent with Black, Hispanic and Latino suppliers

- We’ve committed $45 million in philanthropic support across the state since 2018 such as:

- $5 million to support The 614 for Linden, a CDFI and nonprofit collaborative, in Columbus, which helped catalyze a $20 million fund for affordable housing; create or preserve nearly 750 affordable housing units; provide 57 microloans to local entrepreneurs; support technical assistance for over 100 small businesses; and increase wraparound services for prenatal care, as well as facilitate access to healthy food

Our impact as a proud employer in Ohio:

- Today, as the largest private employer in Columbus, JPMorgan Chase employs over 20,000 Ohioans throughout the state, including more than 2,000 veterans and 500 people with a criminal background who deserve a second chance.

- We also support an additional 3,200 jobs for contractors in our branches and corporate offices across the state.

- In Ohio, our average salary is $96,000, not including benefits. Our lowest starting wage is $41,000 (plus a comprehensive annual benefits package worth nearly $15,000) compared with Ohio’s average salary of $35,0001.

Read footnoted information here

Update on Specific Issues Facing Our Company

CLIMATE COMPLEXITY AND PLANNING

The window for action to avert the costliest impacts of global climate change is closing. At the same time, the ongoing war in Ukraine is roiling trade relations across Europe and Asia and redefining the way countries and companies plan for energy security. The need to provide energy affordably and reliably for today, as well as make the necessary investments to decarbonize for tomorrow, underscores the inextricable links between economic growth, energy security and climate change. We need to do more, and we need to do so immediately.

To expedite progress, governments, businesses and non-governmental organizations need to align across a series of practical policy changes that comprehensively address fundamental issues that are holding us back. Massive global investment in clean energy technologies must be done and must continue to grow year-over-year.

At the same time, permitting reforms are desperately needed to allow investment to be done in any kind of timely way. We may even need to evoke eminent domain — we simply are not getting the adequate investments fast enough for grid, solar, wind and pipeline initiatives. Policies like the Bipartisan Infrastructure Law, the Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Science Act, and the Inflation Reduction Act (IRA) — that hold the potential to unlock over $1 trillion in clean technology development — need to be implemented effectively. The upside is undeniable: Widespread investing across the private sector will aid domestic manufacturing, invigorate research and development in green innovation, help create resilient supply chains, lift up local economies and build the U.S. clean energy workforce by up to 9 million jobs over the next decade. While major advances have been made in the last few years on technology to help this cause, we are hopeful that the great American innovation machine (most advancements will ultimately come from the huge capabilities and capital of America’s largest companies) will find the additional technologies that are desperately needed. There is a downside — massive, inefficient and malinvestment of capital. I talk more about this in the last section on public policy.

Polarization, paralysis and basic lack of analysis cannot keep us from addressing one of the most complex challenges of our time. Diverse stakeholders need to come together, seeking the best answers through engagement around our common interest. Bolstering growth must go hand in hand with both securing an energy future and meeting science-based climate targets for future generations.

AI, DATA AND OUR JOURNEY TO THE CLOUD

Artificial intelligence (AI) is an extraordinary and groundbreaking technology. AI and the raw material that feeds it, data, will be critical to our company’s future success — the importance of implementing new technologies simply cannot be overstated. We already have more than 300 AI use cases in production today for risk, prospecting, marketing, customer experience and fraud prevention, and AI runs throughout our payments processing and money movement systems across the globe. AI has already added significant value to our company. For example, in the last few years, AI has helped us to significantly decrease risk in our retail business (by reducing fraud and illicit activity) and improve trading optimization and portfolio construction (by providing optimal execution strategies, automating forecasting and analytics, and improving client intelligence).

We currently have over 1,000 people involved in data management, more than 900 data scientists (AI and machine learning (ML) experts who create new models) and 600 ML engineers (who write the code to put models in production). This group is focused on AI and ML across natural language processing, time series analysis and reinforcement learning to name a few. We’re imagining new ways to augment and empower employees with AI through human-centered collaborative tools and workflow, leveraging tools like large language models, including ChatGPT.

We also have a 200-person, top-notch AI research group looking at the hardest problems and new frontiers in finance. We were recently ranked #1 on the Evident AI Index, the first public benchmark of major banks on their AI maturity. We take the responsible use of AI very seriously and have an interdisciplinary team of ethicists helping us prevent unintended misuse, anticipate regulation, and promote trust with our clients, customers and communities. AI and data use is complex; it must be done following the laws of the land. But it is an absolute necessity that we do it both for the benefits I just described and, equally, for the protection of the company and the financial system — because you can be certain that the bad guys will be using it, too.

All of our technology groups firmwide work together in a flywheel of innovation and deliver state-of-the-art improvements. We are proud that our AI teams have contributed top-quality novel research and compelling solutions that are transforming more and more business cases every day.

AI is inextricably linked with cloud-based systems, whether public or private, and digital capabilities. Our company needs the cloud for its on-demand compute capacity, flexibility, extensibility and speed. Native cloud-based approaches will ultimately be faster, cheaper and aligned with the newest AI techniques, and they will give us easy access to constantly evolving developer tools.

We have spent over $2 billion building new, cloud-based data centers and are working to modernize a significant portion of our applications (and their related databases) to run in both our public and private cloud environments. To date, we have migrated approximately 38% of our applications to the cloud, meaning over 50% of our application portfolio (this includes third-party, cloud-based applications) is running on modern environments.

This journey to the cloud is hard work but necessary. Unlocking the full potential of the cloud and nearly 550 petabytes of data will require replatforming (putting data in a cloud-eligible format) and refactoring (i.e., rewriting) approximately 4,000 applications. This effort will involve not just the 57,000 employees we have in technology but the dedicated time of firmwide management teams to help in the process.

BANKING TURMOIL AND REGULATORY GOALS

The recent failures of Silicon Valley Bank (SVB) in the United States and Credit Suisse in Europe, and the related stress in the banking system, underscore that simply satisfying regulatory requirements is not sufficient. Risks are abundant, and managing those risks requires constant and vigilant scrutiny as the world evolves. Regarding the current disruption in the U.S. banking system, most of the risks were hiding in plain sight. Interest rate exposure, the fair value of held-to-maturity (HTM) portfolios and the amount of SVB’s uninsured deposits were always known — both to regulators and the marketplace. The unknown risk was that SVB’s over 35,000 corporate clients — and activity within them — were controlled by a small number of venture capital companies and moved their deposits in lockstep. It is unlikely that any recent change in regulatory requirements would have made a difference in what followed. Instead, the recent rapid rise of interest rates placed heightened focus on the potential for rapid deterioration of the fair value of HTM portfolios and, in this case, the lack of stickiness of certain uninsured deposits. Ironically, banks were incented to own very safe government securities because they were considered highly liquid by regulators and carried very low capital requirements. Even worse, the stress testing based on the scenario devised by the Federal Reserve Board (the Fed) never incorporated interest rates at higher levels. This is not to absolve bank management — it’s just to make clear that this wasn’t the finest hour for many players. All of these colliding factors became critically important when the marketplace, rating agencies and depositors focused on them.

As I write this letter, the current crisis is not yet over, and even when it is behind us, there will be repercussions from it for years to come. But importantly, recent events are nothing like what occurred during the 2008 global financial crisis (which barely affected regional banks). In 2008, the trigger was a growing recognition that $1 trillion of consumer mortgages were about to go bad — and they were owned by various types of entities around the world. At that time, there was enormous leverage virtually everywhere in the financial system. Major investment banks, Fannie Mae and Freddie Mac, nearly all savings and loan institutions, off-balance sheet vehicles, AIG and banks around the world — all of them failed. This current banking crisis involves far fewer financial players and fewer issues that need to be resolved.

These failures were not good for banks of any size.

Any crisis that damages Americans’ trust in their banks damages all banks — a fact that was known even before this crisis. While it is true that this bank crisis “benefited” larger banks due to the inflow of deposits they received from smaller institutions, the notion that this meltdown was good for them in any way is absurd.

Let’s be very thoughtful in our reaction to recent events.

While this crisis will pass, lessons will be learned, which will result in some changes to the regulatory system. However, it is extremely important that we avoid knee-jerk, whack-a-mole or politically motivated responses that often result in achieving the opposite of what people intended. Now is the time to deeply think through and coordinate complex regulations to accomplish the goals we want, eliminating costly inefficiencies and contradictory policies. Very often, rules are put in place in one part of the framework without appreciating their consequences in combination with other regulations. America has had, and continues to have, the best and most dynamic financial system in the world — from various types of investors to its banks, rule of law, investor protections, transparency, exchanges and other features. We do not want to throw the baby out with the bath water.

We should have common goals on how we want the banking system to work.

- We want to strengthen regional, midsized and community banks, which are essential to the American economic system. They fill a critical role in small communities, offering local knowledge and local relationships that some large banks simply can’t provide — or can’t provide cost-effectively. Overall, we want to maintain the extraordinary strength this tiered system affords. JPMorgan Chase directly supports this goal as we are one of the largest bankers in America to regional and community banks. We bank approximately 350 of America’s 4,000+ banks across the country. This means we make loans to them or raise capital for them. In addition, we process payments for them, finance some of their mortgage activities, advise them on acquisitions, provide them with interest rate swaps and foreign exchange, and buy and sell securities for them. And we also finance their local communities (think hospitals, schools and larger companies) in ways they cannot.

- We need large, complex banks to continue to play a critical role in the U.S. and global financial system. And we need to recognize that they do so in a way regional banks can’t. Large banks are complex not because they want to be, but because they operate in complex global markets. Regional banks simply cannot manage the scale and complexity of transactions in 50 or 60 countries around the world to help some of America’s best and largest companies accomplish their goals. Think of equity, debt, M&A, research, swaps, foreign exchange, large payments systems, global custody and so on. It takes a global workforce with deep expertise and significant capabilities to provide these services. These large global banks finance not just the world’s largest companies but the world’s development institutions and even countries. Having some of the best large, complex banks in the world is essential to the success of America’s biggest companies, its economic system and its global competitiveness, which says nothing against the importance of having great midsized and community banks as well. And contrary to what some say — to be safe, a global bank needs both huge economies of scale and the strength of diversified earnings streams.

- We should want a system in which a bank failure does not cause undue panic and financial harm. While you don’t want banks to fail all the time, it should be allowed to happen and the resolution should follow a completely prescribed process. In almost all bank failures, uninsured deposits never resulted in lost money — but the very fear of loss can cause a run on any bank having characteristics similar to a bank that has failed. Resolution and recovery regulations did not work particularly well during the recent crisis — we should bring clarity and reassurance to both the unwinding process and measures to reduce the risk of additional bank runs. It should also be noted that banks pay for any bank failure (through fees paid to the Federal Deposit Insurance Corporation) as they pay for the whole financial regulatory system. And yes, while these costs are ultimately passed on to their customers — that is true for all industries — the cost is just the price of implementing proper regulations.

- We want proper transparency and strong regulations. However, it should be noted that regulations, the supervisory regime and the resolution regime currently in place did not stop SVB and Signature Bank from failing — and from causing systemwide issues. We should not aim for a regulatory regime that eliminates all failure but one that reduces the chance of failure and the odds of contagion. We should carefully study why this particular situation happened but not overreact. Strong regulations should not only minimize bank failures but also help to maintain the strength of banks as both the guardians of the financial system and engines that finance the great American economic machine.

- We should want market makers to have the ability to effectively intermediate, particularly in difficult markets, with central banks only stepping in during exceptional situations. In the last few years, we have had many situations in which disruptions in the market were, in my opinion, largely caused by certain regulations that did not improve the safety of the market maker but, instead, damaged the safety of the whole system. In addition, many of the new “shadow bank” market makers are fair-weather friends — they do not step in to help clients in tough times.

- We need banks to be there for their clients in tough times. And they have been. Banks can flex their capital and provide their clients with a lot of loans and liquidity when they really need it. For example, at the beginning of the COVID-19 crisis in March 2020, banks deployed over $500 billion in liquidity for clients and $500 billion in PPP loans — and this does not include banks’ share of the nearly $2 trillion in loans that entered forbearance. Banks also play a unique and fundamental role in the transmission of monetary policy because deposits in banks can be loaned out, effectively “creating” money. Some regulations and some accounting rules have become too procyclical and make it harder to do this.

- Regulation, particularly stress testing, should be more thoughtful and forward looking. It has become an enormous, mind-numbingly complex task about crossing t’s and dotting i’s. For example, the Fed's stress test focuses on only one scenario, which is unlikely to happen. In fact, this may lull risk committee members at any institution into a false sense of security that the risks they are taking are properly vetted and can be easily handled. A less academic, more collaborative reflection of possible risks that a bank faces would better inform institutions and their regulators about the full landscape of potential risks.

- We should decide a priori what should stay in the regulatory system and what shouldn’t. There are reasons for certain choices, and they should not be the accidental outcome of uncoordinated decision making. Regulatory arbitrage is already forcing many activities, from certain types of lending to certain types of trading, outside the banking system. Among many questions that need definitive answers, a few big ones would be: Do you want the mortgage business, credit and market-making, along with other essential financial services, inside the banking system or outside of it? What would be the long-term effect of that choice? Under the new scheme, would nonbank credit-providing institutions be able to provide credit when their clients need them the most? I personally doubt that many of them could.

- We need banks to be attractive investments. It is in the interest of the financial system that banks not become “un-investable” because of uncertainty around regulations that affect capital, profitability and long-term investing. Erratic stress test capital requirements and constant uncertainty around future regulations damage the banking system without making it safer. While it is perfectly reasonable that a bank refrain from stock buybacks, dividends or growth under certain circumstances, it would be far better for the entire banking system if these rules were clearly enumerated (i.e., stipulate that a bank needs to reduce its buybacks and dividend if they breach certain thresholds).

If done properly, banking regulations could be calibrated — adding virtually no additional risk — to make it easier for banks to make loans, intermediate markets, finance the economy, manage a run on their bank and fail if need be. When it comes to political debate about banking regulations, there is little truth to the notion that regulations have been “loosened,” at least in the context of large banks. (To the contrary, our capital requirements have been increasing for years, as our fortress balance sheet chart shows in the introduction.) The debate should not always be about more or less regulation but about what mix of regulations will keep America’s banking system the best in the world, such as capital and leverage ratios, liquidity and what counts as liquidity, resolution rules, deposit insurance, securitization, stress testing, proper usage of the discount window, tailoring and other requirements (including potential requirements on shadow banks). Because of the recent problems, we can add to this mix the review of concentrated customers, uninsured deposits and potential limitations on the use of HTM portfolios. Ideally, new rules and regulations would also make it easier for banks to provide credit in tougher times.

ADJUSTING OUR STRATEGY TO THE NEW REGULATORY REALITY (BASEL III ENDGAME)

The Basel III Endgame (called Basel IV by some) — which, incredibly, has been nearly 10 years in the making — seems likely to increase, yet again, capital requirements for banks in general, through higher operational risk changes, and for trading and capital markets activity in particular, among other things. Whether or not we agree with all these changes (and we’ve discussed these regulations in detail in prior letters), we will simply have to adjust to them immediately. It’s important we describe to our shareholders how we will go about doing that and what it means for banks and, in particular, our bank.

First and foremost, banks must satisfy all of their regulators.

We must satisfy all of our regulators, and, remember, we have regulators all around the world, including more than 10 in the United States alone. Regulations include stress testing, reporting, compliance, legal obligations and trading surveillance, among others. While the business is the first line of defense on all these issues, we also have 3,700 people in compliance, 7,100 in risk and 1,400 lawyers actively working every day to meet the letter and the spirit of these rules along with the final line of defense — audit.

Rules are constantly changing and/or being enhanced and are sometimes, unfortunately, driven by political motivations. Relationships with regulators can often be intense, and, recently, we have lost some terrific people in our firm because of this. Regulators know that when banks disagree, we essentially have no choice — there is no one to appeal to, and even the act of appealing can make them angry. We simply ask respectfully to be heard, but at the end of the day, we will do what they ask us to do.

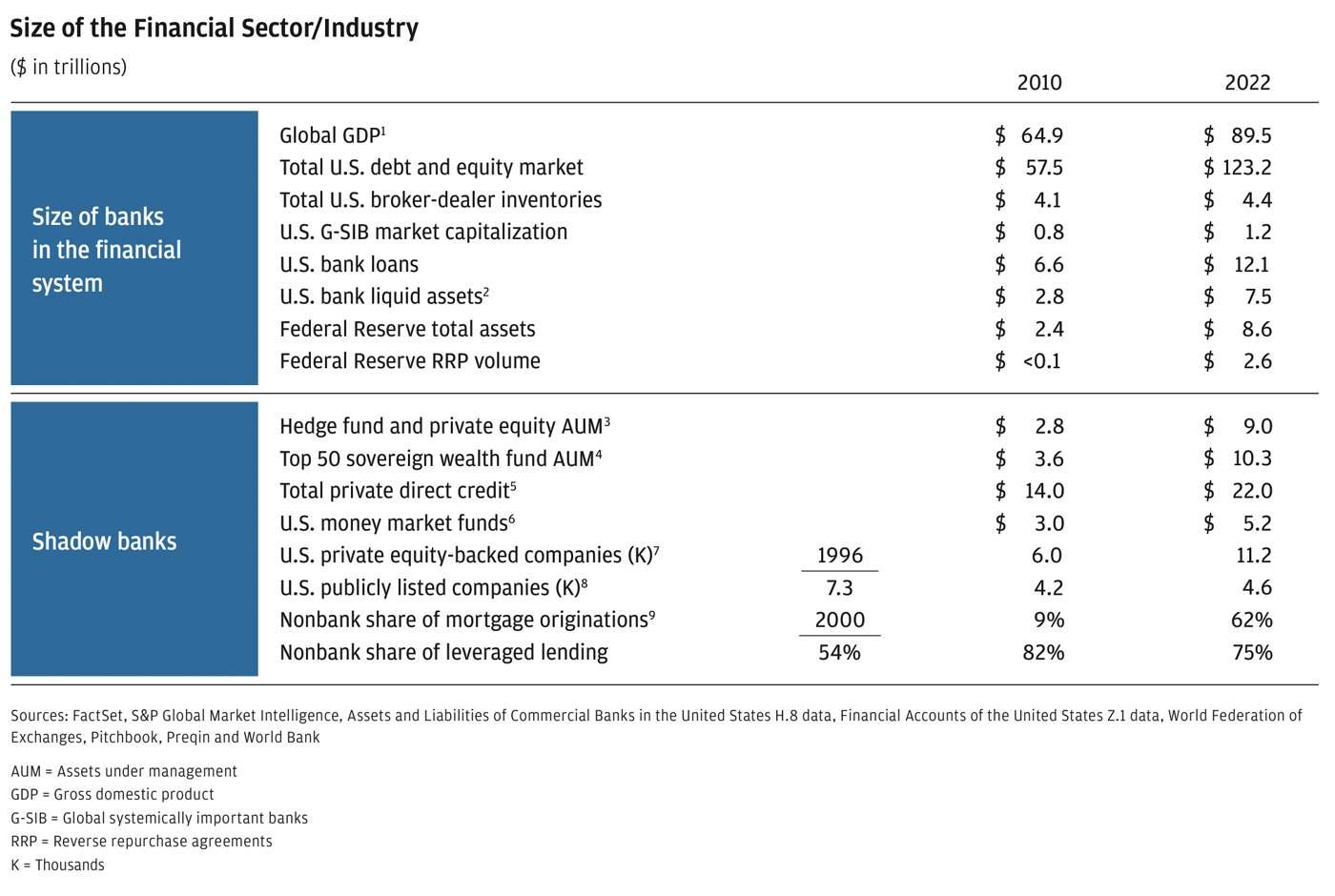

Banks will play a smaller role in the global financial system.

The chart below shows both the decreasing role and size of U.S. banks relative to the global economy alongside the increasing role and size of shadow banks. The data illustrates this dynamic. We expect this trend to continue for all the reasons I’ve discussed.

Read footnoted information here

Banks will continue to be guardians of the financial system.

Properly regulated banks are meant to protect and enhance the financial system. They are transparent with regulators, and they strive mightily to protect the system from terrorism financing and tax evasion as they implement know your customer guidelines and anti-money laundering laws. They protect clients’ assets and clients’ money in movement. Banks also help customers — from protecting their data and minimizing fraud and cyber risk to providing financial education — and must abide by social requirements, such as the Community Reinvestment Act, which requires banks to extend their services into lower-income communities. As mentioned previously, unlike the private market, banks do not always choose when to provide a product or service but need to be there for their clients when they need credit or liquidity the most.

Looking forward, we constantly modify our strategies to adjust to our market realities.

It’s always best to adjust to new reality quickly. We really don’t like crying over spilled milk, although we sometimes do. The new reality is that some things — for example, holding certain types of credit — are more efficiently done by a nonbank.

Here are some actions we are taking to help our business succeed in the current and future environments:

- First and foremost, we must conclude that holding certain types of credit, loans or otherwise has generally become less profitable because of the high levels of capital that need to be held against it — generally more than the market demands. What this means is that some credit is better held in a nonbank. Increasingly, for a credit relationship to make sense, banks need a lot of noncredit-related revenue.

- Because of various capital requirements, we try to reduce clients’ nonoperating cash deposits.

- We are seeking to implement much tighter management and execution of business strategies. This includes repricing certain businesses, running off certain unprofitable products, changing the mix of business for a client, and more rigorously evaluating client selection and resource optimization applied to clients.

- We are exploring new capital optimization strategies, which could include partnerships and perhaps one day more securitizations, among other opportunities.

- Unfortunately, it is becoming increasingly difficult for banks to stay in the mortgage business, which ultimately hurts everyday Americans. The high costs of origination and servicing along with the complexity of regulations create a costly business with significant legal, reputational and operational challenges. In addition, given capital requirements and the lack of a healthy securitization market, it barely makes sense for banks to hold mortgages or mortgage-servicing rights. Many banks have already reduced much of this business. We are hanging on, continuing to hope for meaningful change.

- We have the ability to add low-capital or no-capital revenue streams, like providing valuable data and analytics in trading, travel and other relevant offers in the consumer bank, wealth management and payment services businesses, among others.

If you review our CEO letters, you will see that we have many growth opportunities in front of us and our plans to attack them. We face the future and the new competition, large and small, with confidence, strength and a dash of humility.

KEEPING AN EYE ON ALL OF OUR COMPETITORS

The growing competition to banks from each other, as well as shadow banks, fintechs and large technology companies, is intense and clearly contributing to the diminishing role of banks and public companies in the United States and the global financial system. The pace of change and the size of the competition are extraordinary, and activity is accelerating. Walmart, for example (with over 200 million in-store customers each week), can use new digital technologies to efficiently bring banking-type services to their customers. Apple, already a strong presence in banking-type services with Apple Pay and the Apple Card, is actively moving into other similar services such as payment processing, credit risk assessment, person-to-person payment systems, merchant acquiring and buy-now-pay-later offers. Large tech companies, already 100% digital, have hundreds of millions of customers, as well as enormous resources, in data and proprietary systems — all of which give them an extraordinary competitive advantage.

We remain confident that as long as we stay vigilant, hungry, adaptable, fast and disciplined, we will continue to succeed in building this great company.

Management Lessons

As recent countries and companies have demonstrated, great management and leadership are critical to any large organization’s long-term success. While providing strong management is a disciplined and rigorous process — facts, analysis, detail, rinse and repeat — creating an exceptional management team is an art, not a science.

In the rest of this section, I talk about some management lessons — I always enjoy sharing what I have learned over time by watching others and through my own successes and failures.

BUILDING TRUE FRANCHISE VALUE

Accounting can distort actual economic reality.I have spoken in the past about good and bad revenue and good and bad expenses. Certain expenses, such as opening well-designed and well-located branches, actually are long-term investments of great value. Conversely, poorly underwritten credit creates revenue that you are bound to regret. Further, there are accounting practices that may distort the true value of actions you take. For example, when we create a new credit card account, we recognize origination costs over 12 months, but an average account exists for over eight years. And with the new accounting rules for loan loss reserves — called the current expected credit losses standard — you book the expected life of loan losses on the day you make the loan, while the revenue comes in over multiple years.

Increasingly in the modern world, many valuable things are not reflected on our balance sheet in generally accepted accounting principles — for example, previously expensed intellectual property or extraordinary human capital. At the end of the day, human capital is the most valuable asset. Think of a great athlete, a great lawyer or a great artist. It’s not simply the equipment — it’s the extraordinary training and talent of those involved, as we’ve also seen with the U.S. military. And sometimes it’s not the individual but the highly coordinated activities of the team that deliver the championship.

Finally, if any value is based upon models, one must really test the sensitivity of the outcome against changes in assumptions. Understanding the range of potential outcomes may be far more important than the point estimate created by a model. In some cases, you can have an excellent average outcome, with a chance of death.

The point is: Accounting can distort economic reality and can lead one to make the wrong decisions.

Building true franchise value requires an outcomes-based outlook.In banking, specific examples illustrate how merely following accounting and capital rules — without thinking through the outcomes— can lead one astray. I’m going to describe just two examples, but there are hundreds more.

If you buy or create a loan at par and put it on your balance sheet at par (think of a mortgage) and internally finance it, even match-funded with 10% capital, you might believe you have a 12% return. Many companies subscribe to this interpretation and simply continue to borrow money to invest in such a thing. But I would tell you this product has no franchise value because it is only worth par, and, in fact, a small change in that value (because of interest rates and credit spread) could mean that you have made a huge mistake. If, on the other hand, you create a loan and sell it at more than par at a profit, you have created value — whether or not you keep it on your balance sheet. And far more important, if you create a loan and at the same time forge a client relationship – and you add additional capital light revenue, such as asset management and cash management — you have created something of long-term value that you can nurture and grow. This is franchise value.

Simply taking interest rate risk (which contributed to the downfall of SVB) is not a business. Nor is simply taking credit risk. One person and a computer will suffice — you do not need 290,000 people circling the globe to do that.

Another example relates to any branch-based business. Let’s say I build a system with well-designed and well-located branches, staffed by well-trained personnel who can offer customers great products and services and who strive to do every task a little bit better. Then you build a branch system with outdated sites in poor locations (often to save money) that have undertrained and underpaid staff and lower-quality products and services. Between the two, my branch system will win every time. One system will have high franchise value and be self-perpetuating with high returns. The other enterprise is probably on the road to eventual failure. If you study the history of business, you can see this phenomenon play out in grocery stores, car companies, restaurants, retailers and various other enterprises.

LEARNING FROM INVESTOR DAY

In February 2021, we did not hold our annual Investor Day for the obvious reason — COVID-19. When February 2022 came around, we were somewhat happy to be relieved of that responsibility again. Investor Day is a tremendous amount of work. But from 2020 to 2022, we did a lot of investment spending and made several acquisitions. Some of our analysts questioned whether we were being transparent enough in terms of what we were doing and why we were doing it. While sometimes we get frustrated with investor demands — and not all investors are created equally — all investors should be treated fairly and with respect. So, in 2022, we gave it more thought and reversed course with an extensive Investor Day. Our senior management team explained in detail our acquisitions and our investments, answering every question to the best of their ability. Having to explain your business to investors, comparing yourself with competitors and looking at the business as a whole — across sales, marketing, returns, growth, risks and strategic opportunities — was a terrific exercise for us. We learned our lesson!

This also raises another issue. Of course, it is critically important to analyze your business at the right disaggregated level — right down to the branch — inside the company. But it is also important to have the proper segments reported externally to the company, properly accounted for and generally aligned to their relevant competitors. This actually helps hold managers accountable by forcing them to accurately assess performance — the good, the bad and the ugly — without any attempts to avoid reality through an external obfuscation of results.

BALANCING A CUSTOMER-CENTRIC APPROACH WITH (EXCESSIVE) RISK

Most businesses, including banks like us, say they put their customers first. We often go further than that statement to say that we need to be there for them, in good times and in bad. However, banking is a complex industry, and this customer-centric approach requires a little more explanation.

In our business, we are essentially a financial partner to a client. While we strive to build great client relationships based on trust over the long run, our role has intricacies. For example, we do not need every transaction to make economic sense — just the overall client relationship, year after year. Whatever the transaction, we need to be properly compensated for the risks we bear, which can be extraordinary. Very often, a client will merely look for the lowest price, which we completely understand; we recognize that sometimes banks are perfectly willing to make a certain transaction for a client at a loss. There are also occasions when we need to tell a client that a specific financial transaction would be imprudent — maybe for us and the client.

Say, for example, that a very strong client of ours is simply trying to get the best price for a leveraged loan. If we believe the desired price is unwise and another institution is willing to offer it, we will advise the client to take that option. For us, this is pure counterparty risk and not really part of our core relationship. Conversely, should the same client come to us and request something that extends beyond what we consider reasonable for that transaction, we may nonetheless do it. Perhaps the client is in the middle of an M&A transaction in difficult markets and simply cannot get the financing they need — other than from us. In recent crises, we have often gone the extra mile for a client at great risks to ourselves, not to make a profit but to rescue the client from financial calamity.

Fundamentally, putting the client first means always providing them with the products and services they need (although they may go somewhere else because of price) and having our whole team work hard for them — either in the United States or around the world, reliably and with constancy. One of the most important things we do for a client, above all else, is to be a steady hand, providing financial safety and security at every turn.

Some Commonsense Principles for Corporate Governance

I have written before about the diminishing role of public companies in the American financial system. They peaked in 1996 at 7,300 and now total 4,600. Conversely, the number of private U.S. companies backed by private equity firms has grown from 1,900 to 11,200 over the last two decades. And this does not include the increasing number of companies owned by sovereign wealth funds and family offices. This migration is serious and worthy of critical study, and it may very well increase with more regulation and litigation coming. We really need to consider: Is this the outcome we want?

There are good reasons for such healthy private markets, and some good outcomes have resulted from them as well. The reasons are complex and may include public market factors such as onerous reporting requirements, higher litigation expenses, costly regulations, cookie-cutter board governance, less compensation flexibility, heightened public scrutiny and the relentless pressure of quarterly earnings.

With intensified public reporting, investors’ growing needs for environmental, social and governance information and the universal proxy — which makes it very easy to put disruptive directors on a board — the pressure to become a private company will rise. Corporate governance principles are becoming more and more templated and formulaic, which is a negative trend. For example, sometimes proxy advisors automatically judge board members unfavorably if they have been on the board a long time, without a fair assessment of their actual contributions or experience. And some simple, sensible governance principles are far better than the formulaic ones. The governance of major corporations is evolving into a bureaucratic compliance exercise instead of focusing on its relationship to long-term economic value. Good corporate governance is critical, and a little common sense would go a long way.

PROMOTING OPEN COMMUNICATION AND TRUST WITH THE BOARD

As authorized and coordinated by the board, directors should have unfettered access to management, including those below the CEO’s direct reports. At every board meeting, to ensure open and free discussion, the full board should meet in executive session without the CEO or other members of management. The independent directors should ensure that they have enough time to do this properly.

This one act would allow the board to have a completely open conversation and provide candid feedback to the CEO and management team. Good CEOs, who are trying to do the best job they can, should appreciate this important feedback — and should know how difficult it is to gather in a large group. This type of quality discussion among and with board members leads to collaboration and good succession planning since every meeting should include a real conversation around this important topic. Meetings such as these allow the board to nurture the extraordinary value of collaboration and trust.

CONFRONTING SUCCESSION PLANNING

Our board is responsible for succession planning, and it is on the agenda every time board members meet — both when they are with me and when I am not in the room. We already have a “hit-by-the-truck” plan ready to go (not all companies can say this), and we have multiple successor candidates who are well known to the board and to the investor community. The board believes this is one of its paramount priorities. You can rest assured that our board members are on the case and are very comfortable with where we are.

ACTIVE ENGAGEMENT WITH ASSET MANAGERS

We — companies and investors — need to become more active and involved in proxy issues each year to foster better communication between the investors and the board of the companies they own. Whether it’s issues around climate risk or say on pay, it should be appropriate for the management team or board to actively engage with investors during proxy season to hear and understand each other’s views on key issues and communicate their positions in real time. Investors should also require proxy advisors to share any communications they have with a company in real time before investors make voting decisions. In my view, too many portfolio managers and investors have partially ceded critical decisions on key proxy issues to their internal stewardship groups or external proxy advisors. Stewardship teams are also often under pressure to follow proxy advisors by bureaucratic internal systems at investment firms that discourage disagreement and encourage the safety of the herd. Many portfolio managers have told me that even when they have the authority to override the internal group, it is frequently very difficult to do so.

The new universal proxy is likely to create havoc for companies.

The new universal proxy makes it such that one investor with one share, who owns it for as little as one day, can nominate a director for any reason, at relatively low cost. In my view, it is likely that not just activists but also special interest groups will nominate directors. Not only would this be extremely disruptive to the board, but, almost by their nature, special interest groups would be counter to shareholders’ interests. While we fully respect being transparent — protecting investors and shareholder rights — director election processes are becoming too far removed from shareholder interests.

While there are legitimate complaints against entrenched boards, good boards often tend to interview prospective candidates for their brains, integrity, work ethic, management and collaboration skills, and experience. With this new universal proxy, it’s easy to envision a time when a proxy season will be like a political campaign, with interest groups on both sides of an issue trying to elect a board member. Disruptive boards, which can be caused by just a single troublesome member, are an anathema to shareholders’ interests. This is unlikely to end well.

Evaluating and Managing the Economic and Geopolitical Risks Ahead

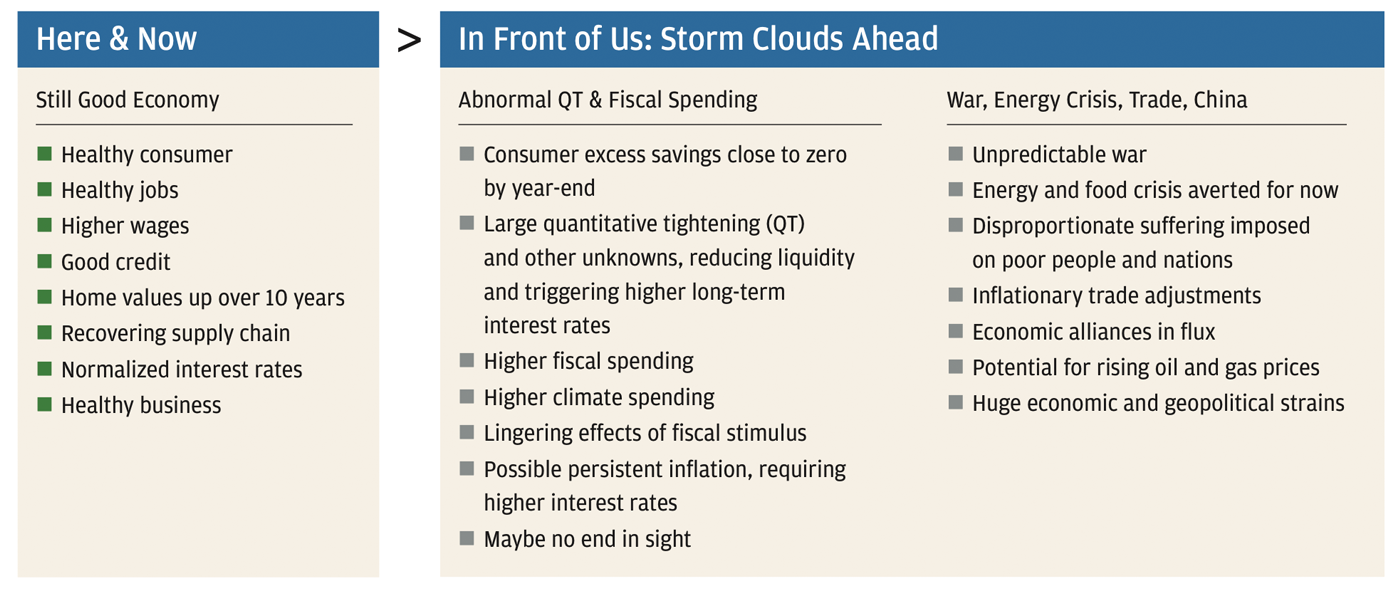

We usually don’t worry about typical economic fluctuations and often compare economic forecasting with weather forecasting: It is extremely complicated, easy to do in the short term and far more difficult to do in the long run. It is particularly hard to forecast true longer-term inflection points in the economy. Although we don’t want to waste time on “normal” fluctuations, we do want to be prepared for economic extremes — we look at multiple possibilities and probabilities and manage our company so that we can handle all of them, whether or not we think they actually will happen. After we spoke last year about storm clouds, some of those storms did, indeed, hit, and, unfortunately, some of those threatening clouds are still here.

2022 was not normal, economically speaking, and, in fact, 2022 witnessed several dramatic events — the Ukraine war began; inflation hit a 40-year high of 9%; the federal funds rate experienced one of its most rapid increases, up 425 basis points, albeit from a low level; stock markets were down 20%; unemployment fell to a 50-year low at 3.5%; and the U.S. economy was bolstered by frequent fiscal stimulus and by high and rising government debt while supply chain issues eased. In addition, work from home began to raise commercial real estate challenges and, finally, long- and short-term interest rates presented a sharply inverted yield curve, which is “eight for eight” in terms of predicting a recession (more on this later). But, surprisingly, the global economy marched ahead.

THE CURRENT ECONOMY: PRETTY GOOD BUT STORM CLOUDS AHEAD

Until the collapse of Silicon Valley Bank, the current economy was performing adequately, both here in the United States and remarkably better than anyone expected in Europe. The “market” was generally forecasting either a soft landing or a mild recession, with interest rates peaking at 5% and then slowly coming down.

There has been a lot of market volatility over the past year, partially, in my opinion, as people over-extrapolate monthly data, which is highly distorted by inflation, supply chain adjustments, consumer substitution, basically poor assumptions about housing costs and other factors. But underlying all this, consumers have been spending 7% to 9% more than in the prior year and 23% more than pre-COVID-19. Similarly, their balance sheets are in great shape as they still have, according to our own analysis, $1.2 trillion more “excess cash” in their checking accounts than before the pandemic (credit card debt is simply normalizing). In addition, unemployment is extremely low, and wages are going up, particularly at the low end. We’ve had 10 years of home and stock price appreciation, and even if we go into a recession, consumers would enter it in far better shape than during the great financial crisis. Finally, supply chains are recovering, businesses are pretty healthy and credit losses are extremely low.

The failures of SVB and Credit Suisse have significantly changed the market’s expectations, bond prices have recovered dramatically, the stock market is down and the market’s odds of a recession have increased. And while this is nothing like 2008, it is not clear when this current crisis will end. It has provoked lots of jitters in the market and will clearly cause some tightening of financial conditions as banks and other lenders become more conservative. However, it is unclear whether this disruption is likely to slow consumer spending (as of April 1, 2023, spending has been consistently running higher versus the prior year). Although higher rates, particularly in mortgages, have reduced both home sales and prices, do remember that consumer spending drives more than 65% of the U.S. economy.

While the current crisis has exposed some weaknesses in the system, it should not be considered, as I pointed out, anything like what we experienced in 2008. Nonetheless, we do have other unique and complicated issues in front of us, which are outlined in the chart below.

POTENTIAL TROUBLE BREWING FROM UNPRECEDENTED FISCAL SPENDING, QUANTITATIVE TIGHTENING AND GEOPOLITICAL TENSIONS

Having already confessed to how difficult it is to predict the future, for planning purposes it still makes sense to try to assess the environment ahead by laying out those factors that may be significantly different from the past.

Fiscal stimulus is still surging through the system.In the last three years, partially but not entirely due to the pandemic, the federal government had a deficit of $3.1 trillion (2020), $2.8 trillion (2021) and $1.4 trillion (2022). These are extraordinary numbers, which ended up in consumers’ pockets, in states and local municipalities, and even in companies. We pointed out last year that you simply cannot have this level of spending and say that it’s not inflationary. It’s also important to point out that there is a multiplier effect of this stimulus; that is, one person’s spending is another person’s income and so on. The deficit for the next three years is now estimated to be $1.4 trillion to $1.8 trillion per year, which is also an extraordinary number, with no end in sight. In Europe, fiscal deficits are high — even before the enormous subsidies given to consumers to counterbalance higher energy prices. It’s also important to note that borrowing to invest is fundamentally different from borrowing to consume — borrowing to consume can only be inflationary.

This is before any additional costs related to future recessions, the war or any other unforeseeable events. Offsetting this, by sometime late this year or early next year, we expect consumers will have spent the bulk of their remaining excess savings. It remains to be seen whether this will cause a little bit of a cliff effect or whether consumer spending will simply slow down. Either way, this will add to whatever recessionary pressures there are sometime in the future.

Today’s quantitative tightening is following more than a decade of quantitative easing.

In the two years after COVID-19, the Fed bought $4.5 trillion of U.S. Treasuries and mortgage-backed securities, bringing its total balance sheet to $9 trillion. We have experienced almost 12 years of quantitative easing (QE), which drove interest rates down — so much so that U.S. short-term rates were virtually zero, and the 10-year bond hit a low of 0.5%. Amazingly, tens of trillions of dollars of debt, mostly in Europe, sold at negative interest rates (we will look back upon this with total astonishment). This period of QE also led to extraordinary liquidity (and a surging money supply) that undoubtedly drove increased prices across many investment classes — from stocks and bonds to crypto, meme stocks and real estate, among others. Importantly, this also increased bank deposits from $13 trillion to $18 trillion (and the now-famous uninsured deposits from $6 trillion to $8 trillion).

QE is now being reversed into quantitative tightening (QT) as the Fed grapples with inflation. So far, the Fed has reduced its securities holdings by approximately $550 billion and is committed to reducing its holdings by almost $100 billion in securities each month or over $1 trillion each year.

How all this will unfold is still unknown as the direction and speed of money have changed significantly from prior years. To varying degrees, banks will compete for money, not only among one another but also with money market funds, other investments and the Fed itself. Money market fund total assets under management have increased by $650 billion since April 2022, with a significant portion migrating into the Fed’s reverse repo facility, thereby draining deposits from the banking system. So while the Fed’s balance sheet has come down by approximately $550 billion, deposits at the banks have come down by $1 trillion, largely uninsured deposits. Unfortunately, some banks invested much of these excess deposits in “safe” Treasuries, which, of course, went down in value as rates rose faster than most people expected.

It should be noted that an inordinate amount of attention is focused on short-term interest rates, which the Fed affects directly. But the Fed does not completely control long-term rates and liquidity, which are influenced by both supply and demand (QT) and global investor preferences and sentiment — importantly, including views on risk and safety. It is also important to remember that while the central banks of the world are now selling instead of buying securities, the governments of the world have larger debts to finance. The United States alone needs to sell $2 trillion in securities, which must be absorbed in the market. This turn of events is generally true globally.

There has been huge intervention by central banks around the world over the last decade. While it was completely necessary in 2008 and 2009 to stop the worst of the global financial crisis, and again in 2020 to stop the effects of the global pandemic, the depth and breadth of these interventions will be studied for years as will the extent to which we need QT (whose full effect may not be known immediately). It is unclear how the Fed incorporated the enormous fiscal spending into both its forecasts for growth and inflation, as well as its need to continue QE as it did. And importantly, the Fed’s ability to reverse course on this strategy (QT) is somewhat constrained by higher inflation (though, of course, it can temporarily adjust its actions to deal with the current bank failure crisis).

War complicates geopolitics and materially adds risks.We have not had a major land war in Europe since 1945. The war in Ukraine, already into its second year, has been particularly devastating in terms of casualties and damage and has been haunted by the threat of nuclear weapons. It may very well last for many more years. Wars are unpredictable, and at the start, most predictions about how they will end have been completely wrong.

This war is also affecting global energy and food supplies, with a disproportionate and negative effect falling on poor people and poorer nations, including millions of Ukrainian refugees. There is still a risk that energy and food supply lines, which are not secure, will lead to higher prices and the large migration of people, triggering another level of geopolitical dislocation.

The tensions of this war are also leading to the rethinking of many economic alliances, as well as trade and national security. All these factors create more risk and potentially higher inflation, and their confluence (along with inflation and QT) creates a somewhat unpredictable and dangerous outcome.

This may be a once-in-a-generation sea change, with material effect.Of course, there is always uncertainty. I am often frustrated when people talk about today’s uncertainty as if it were any different from yesterday’s uncertainty. However, in this case, I believe it actually is.

Less-predictable geopolitics, in general, and a complex adjustment to relationships with China are probably leading to higher military spending and a realignment of global economic and military alliances.

Higher fiscal spending, higher debt to gross domestic product (GDP), higher investment spend in general (including climate spending), higher energy costs and the inflationary effect of trade adjustments all lead me to believe that we may have gone from a savings glut to scarce capital and may be headed to higher inflation and higher interest rates than in the immediate past.

Essentially, we may be moving, as I read somewhere, from a virtuous cycle to a vicious cycle.