Dear Fellow Shareholders,

As we prepare this year's annual letter to shareholders, the world is confronting one of the greatest health threats of a generation, one that profoundly impacts the global economy and all of its citizens. Our thoughts remain with the communities and individuals, including healthcare workers and first responders, most deeply hit by the COVID-19 crisis.

Throughout our history, JPMorgan Chase has built its reputation on being there for clients, customers and communities in the most critical times. This unprecedented environment is no different. Our actions during this global crisis are essential to keeping the global economy going and will be remembered for years to come.

In these annual letters, I usually cover a range of topics, including a review of JPMorgan Chase's principles, priorities and performance, as well as the broader geopolitical issues facing our company and the most critical public policy issues affecting our country. When the time is right and the future is clearer, I will provide a more complete and current view on how this crisis might change our strategies around how we run the company, work with our clients and governments, and develop public policy solutions. However, right now, as we deal with the spiraling effects of this pandemic, I want to focus on what we as a bank can do to remain strong, resilient and well-positioned to support our colleagues, clients, customers and communities across the globe.

Looking back on the last two decades — starting from my time as CEO of Bank One in 2000 — the firm has weathered some unprecedented challenges, as we will with this current pandemic, but they did not stop us from accomplishing some extraordinary things. Once again, you should know how grateful and proud I am of our more than 200,000 employees around the world. I also want to thank Daniel Pinto, Gordon Smith, our Operating Committee, our Board of Directors and our senior leaders for the exceptional leadership they have shown under the most difficult of circumstances.

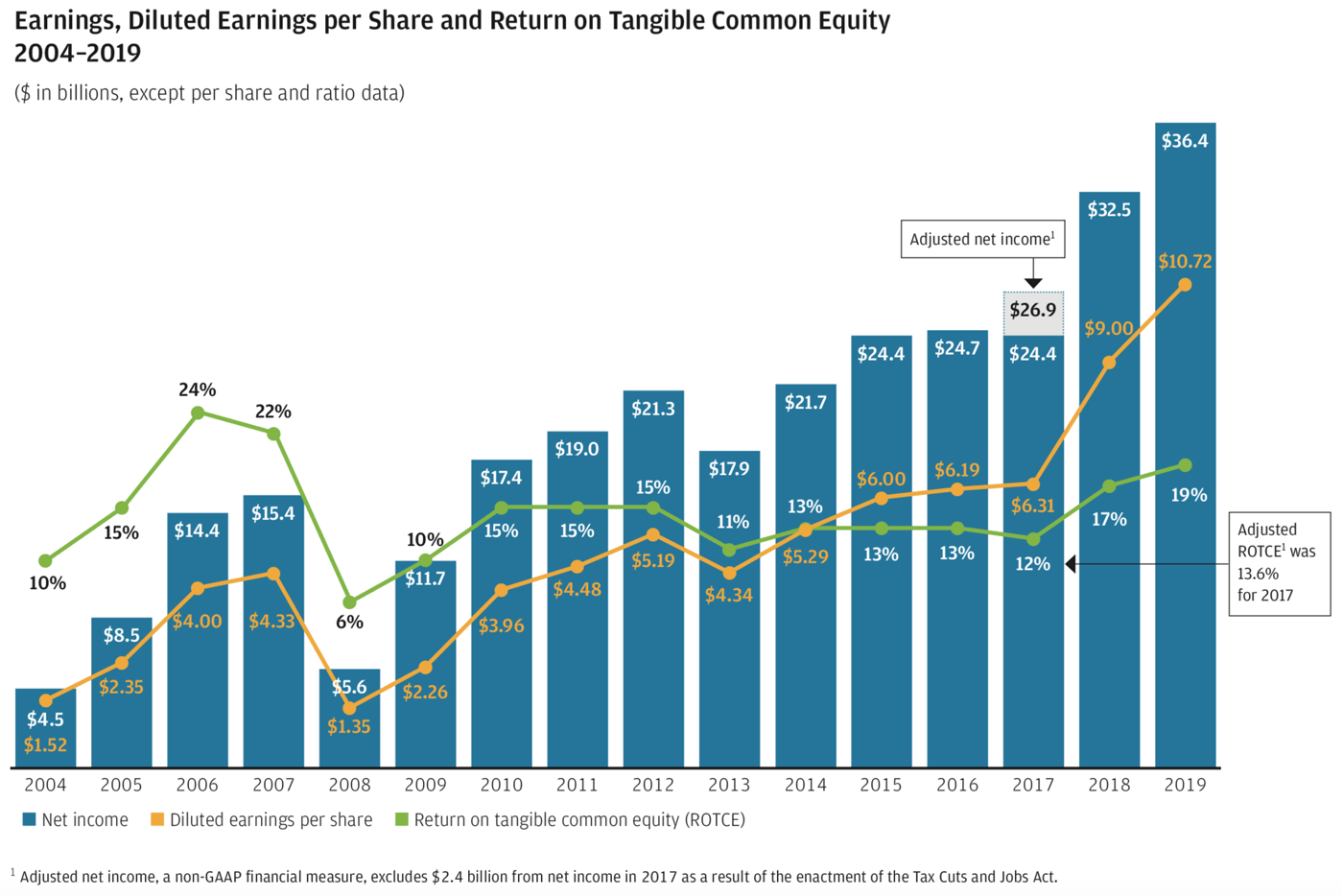

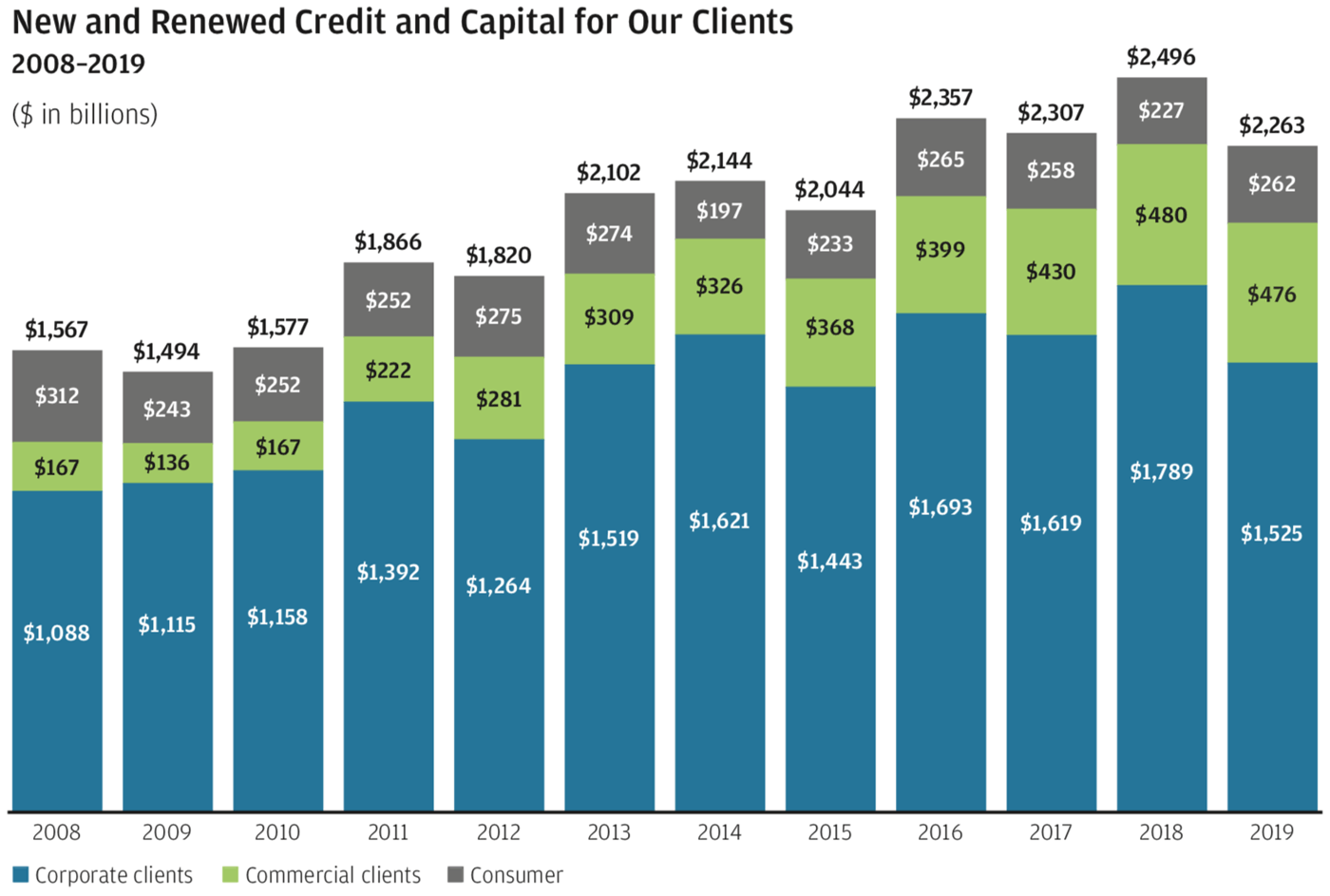

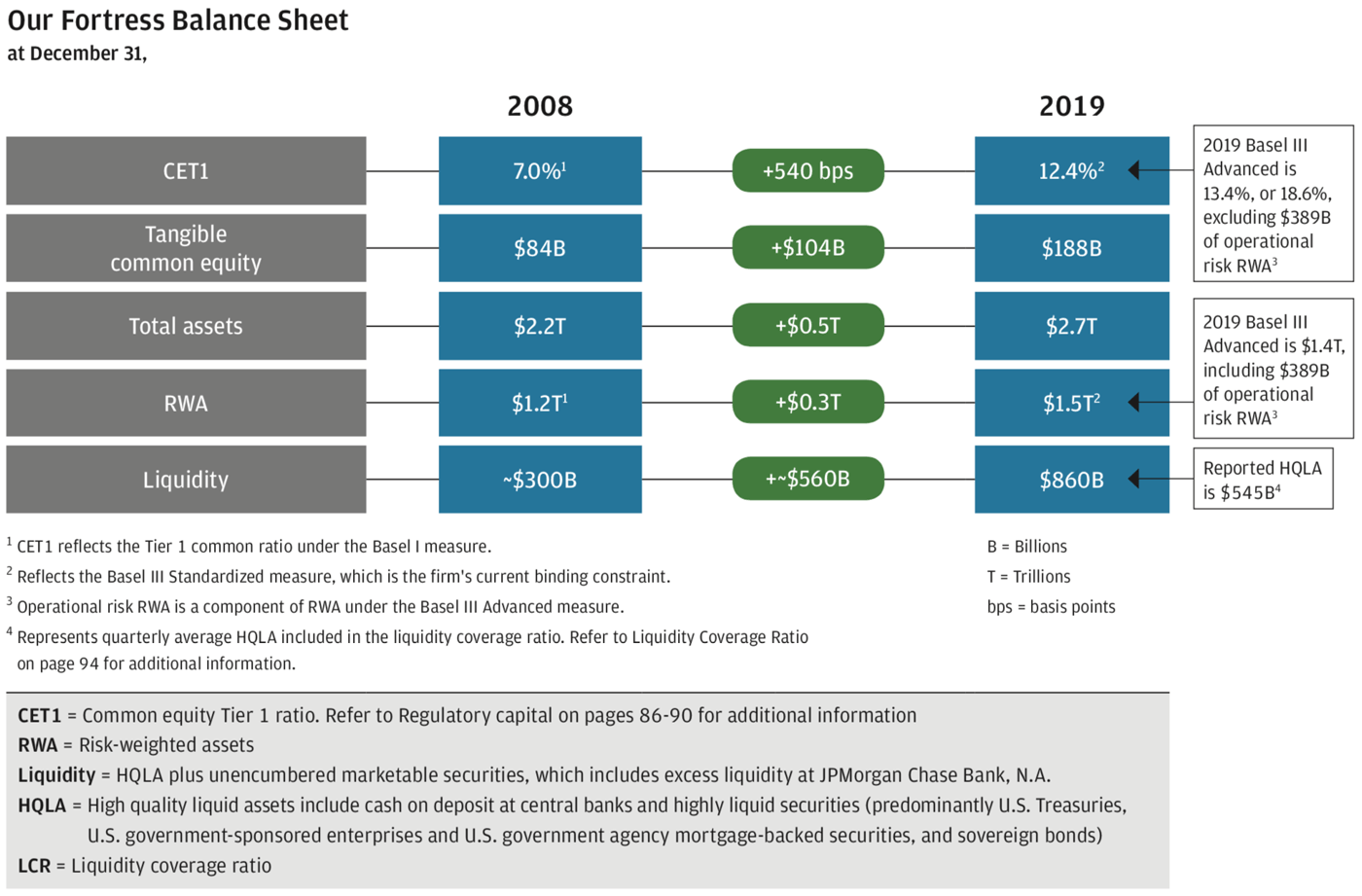

We entered this crisis in a position of strength. 2019 was another strong year for JPMorgan Chase, with the firm generating record revenue and net income, as well as setting numerous other records across our lines of business. We earned $36.4 billion in net income on revenuefootnote1 of $118.7 billion, reflecting strong underlying performance across our businesses. We now have delivered record results in nine of the last 10 yearsfootnote2 and are confident we will continue to do so in the future, though it should be expected that our earnings will be down meaningfully in 2020. Our largest businesses grew revenue and net income for the year, while the firm continued to make significant investments in products, people and technology. We grew core loans by 2%, increased deposits overall by 5% and generally broadened market share across our businesses, all while maintaining credit discipline and a fortress balance sheet. In total, we extended credit and raised capital of $2.3 trillion for businesses, institutional clients and U.S. customers.

JPMorgan Chase stock is owned by large institutions, pension plans, mutual funds and directly by individual investors. However, it is important to remember that in almost all cases, the ultimate beneficiaries are individuals in our communities. Approximately 100 million people in the United States own stock, and a large percentage of these individuals, in one way or another, own JPMorgan Chase stock. Many of these people are veterans, teachers, police officers, firefighters, retirees, or those saving for a home, school or retirement. Your management team goes to work every day recognizing the enormous responsibility that we have to perform for our shareholders.

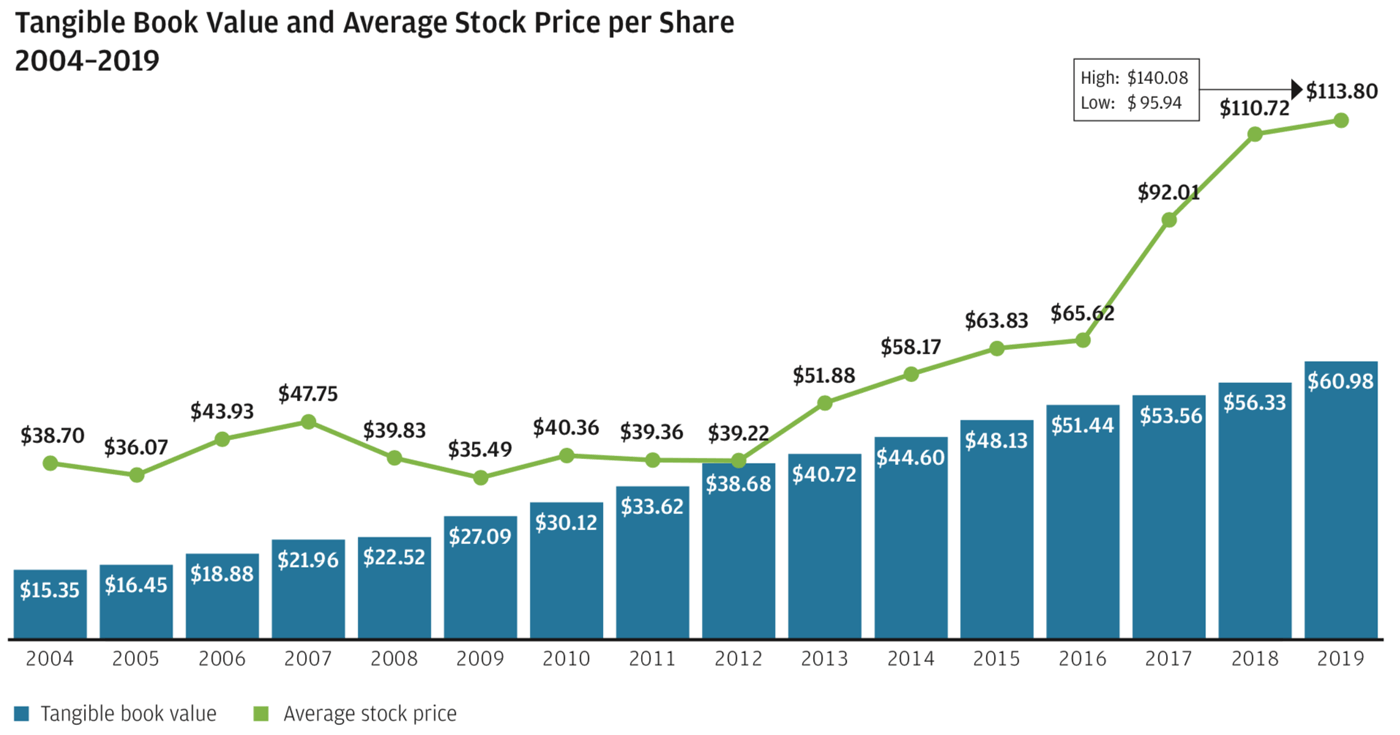

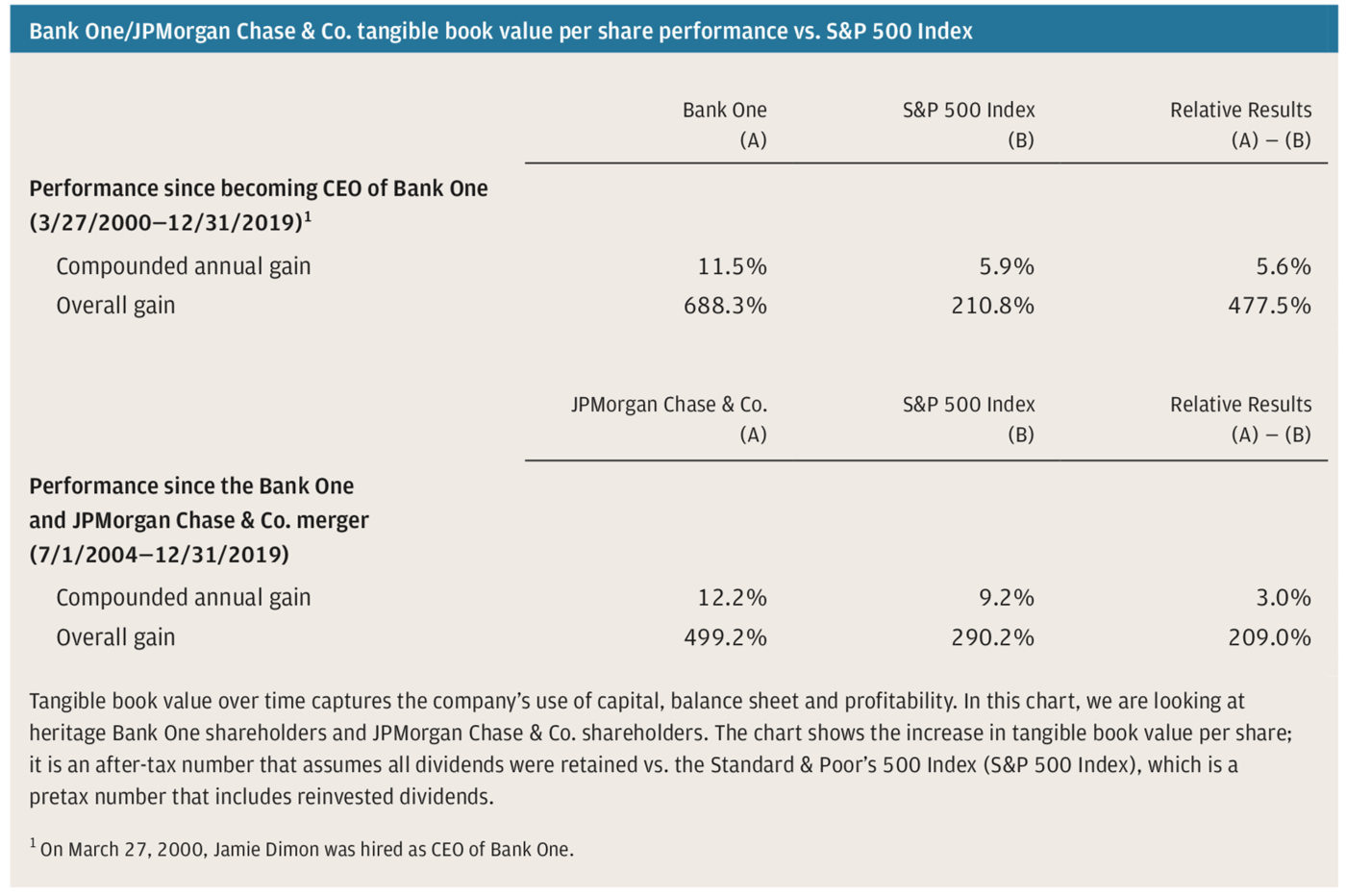

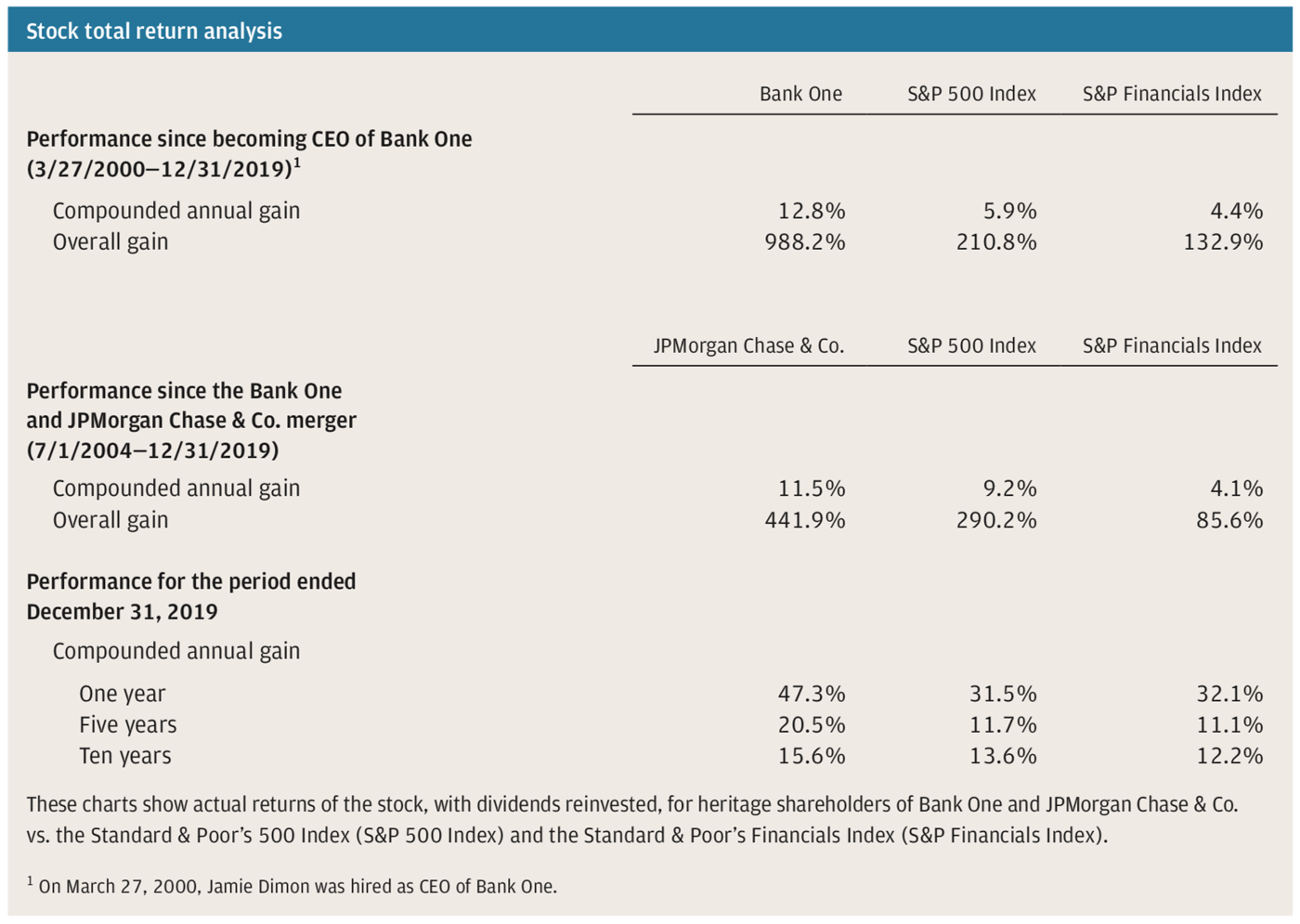

While we don't run the company worrying about the stock price in the short run, in the long run our stock price is a measure of the progress we have made over the years. This progress is a function of continual investments, in good and bad times, to build our capabilities — our people, systems and products. These important investments drive the future prospects of our company and position it to grow and prosper for decades. Whether looking back over five years, 10 years or since the JPMorgan Chase and Bank One merger (15 years ago), our stock has significantly outperformed the Standard & Poor's 500 Index and the Standard & Poor's Financials Index.

The results shown above use our stock price as of December 31, 2019. If you compare that with our stock price as of March 31, 2020, you would see a dramatic change. For example, the overall stock price gain from the date of the JPMorgan Chase and Bank One merger was 442% at the end of last year, but it dropped to 252% three months later. While that's still far better than many companies' performance, it illustrates the volatility of returns.

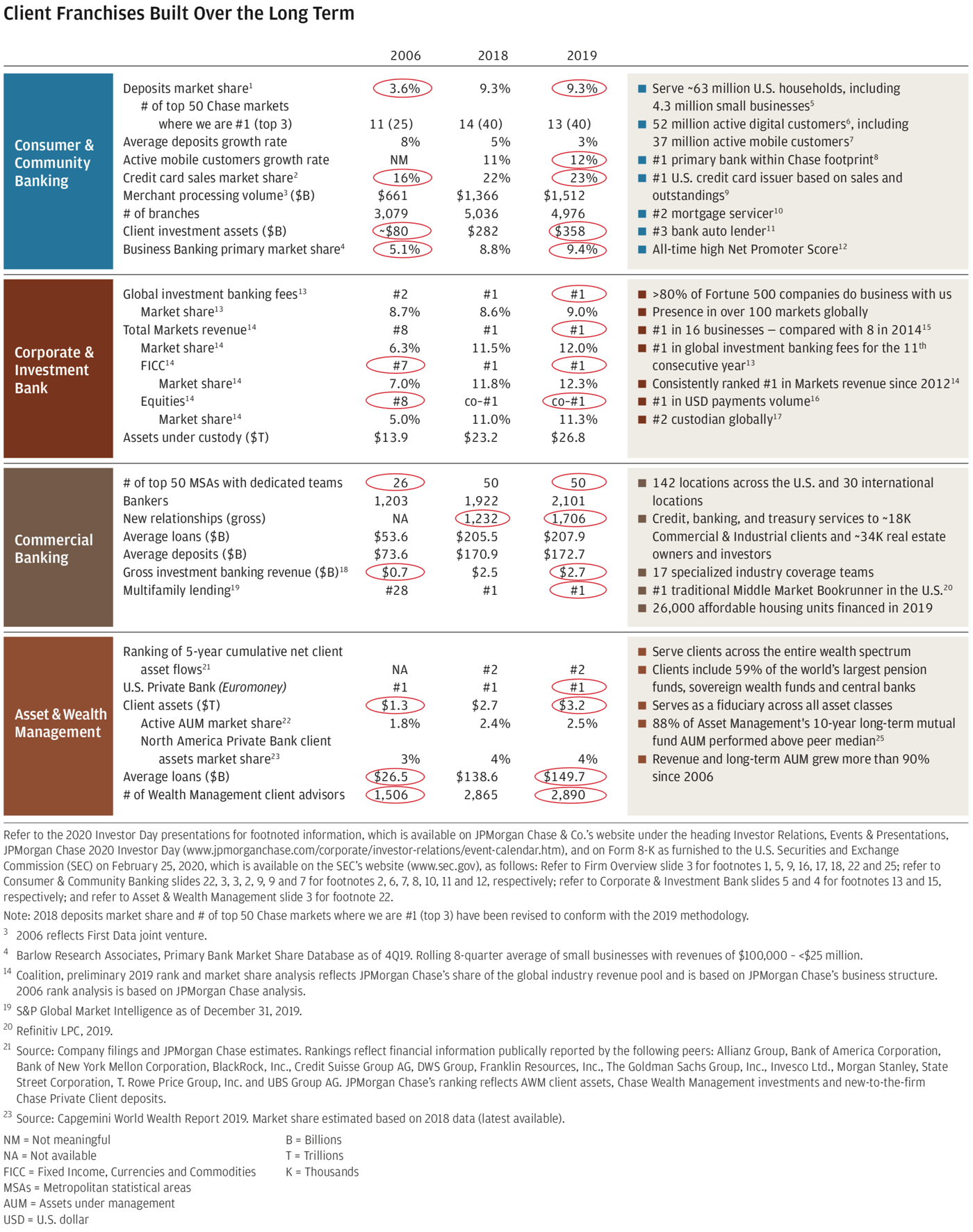

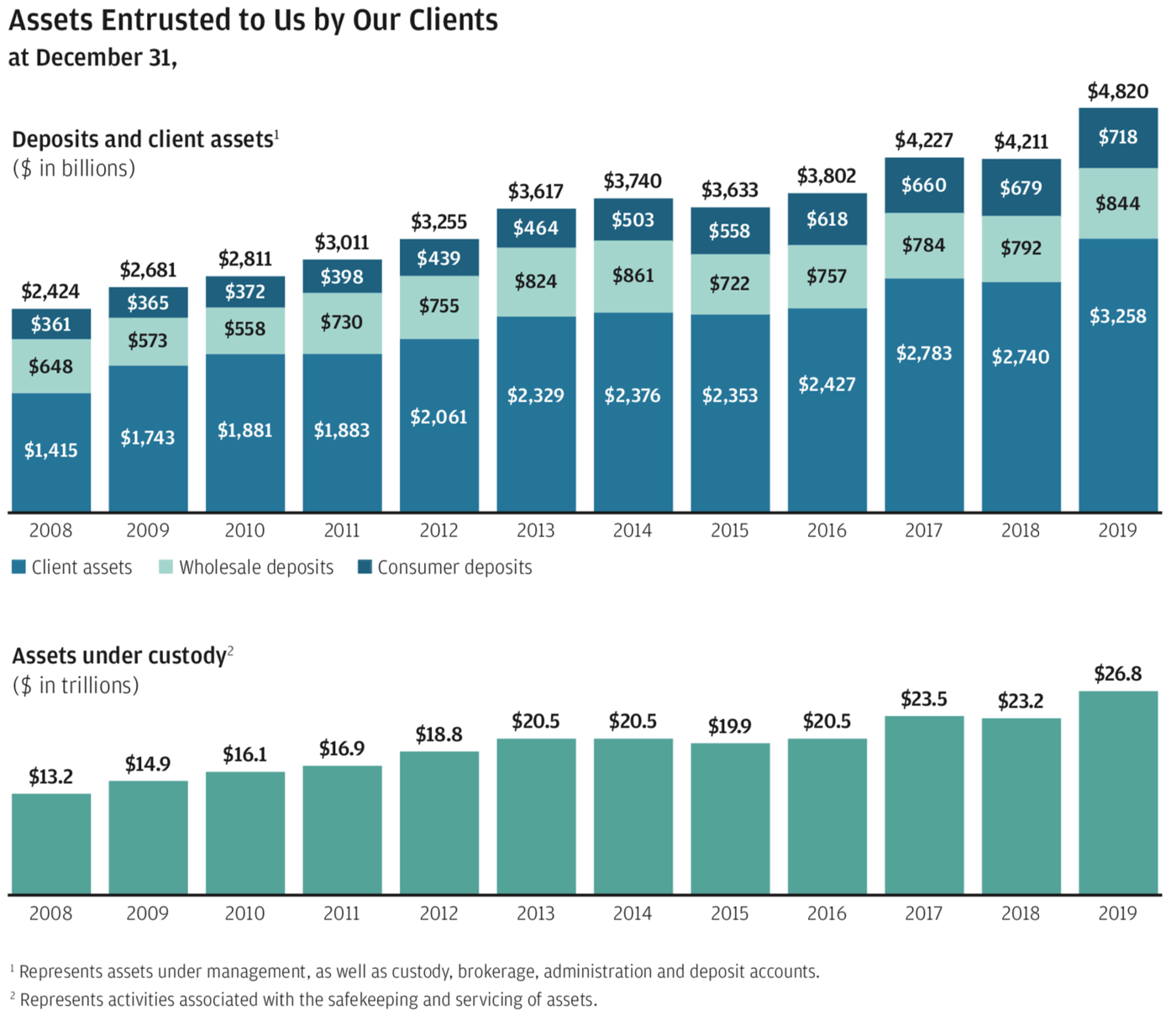

Unlike past letters, the placement of charts about the performance of our lines of business and our fortress balance sheet is different — they can be found in an appendix following this letter to peruse at your leisure. Instead, I am going to focus my comments in the rest of this letter on issues that relate to our current crisis. And while I enjoy sharing my opinion on many other matters, I will avoid doing so this year.

Within this letter, I discuss the following:

DEALING WITH AN EXTRAORDINARY CRISIS

- We go to extraordinary lengths to help our customers — consumers, small businesses, midsize companies, large corporations, and state and local governments.

- We take excellent care of our employees.

- We make extraordinary efforts to lift up our communities, especially in challenging times.

- We are transparent with our shareholders: What they should expect regarding our financial and operating performance in 2020.

- We are working closely with all levels of government during this crisis — and while we will participate in government programs to address the severe economic challenges, we will not request any regulatory relief for ourselves.

- We need a plan to get safely back to work.

- We need to come together: My fervent hope for America.

DEALING WITH AN EXTRAORDINARY CRISIS

A corporation – essentially any institution – is a living, breathing organism made up of people, technology, institutional knowledge and relationships and is generally organized around mission and purpose. Entering into a crisis is not the time to figure out what you want to be. You must already be a well-functioning organization prepared to rapidly mobilize your resources, take your losses and survive another day for the good of all your stakeholders.

No matter the challenge, we manage our company consistently with principles that have stood the test of time. I have written about these inviolable principles often – the need for extremely talented and motivated employees; a fortress balance sheet that allows us to invest in good times and in bad times; clear, comprehensive and accurate financial, risk and operating reporting to let us make quick and accurate decisions; a devotion to our customers and communities; and continuous investing in technology to better serve both our employees and our customers. (These principles also underlie an organization's preparedness for tough competition – I was going to write this year that the competition is back in all of its facets. There'll be more to come on that next year.)

We are there for our customers, employees and communities in good and bad times – we are a port in the storm. It is in the toughest of times that we need to use our capital and liquidity to help clients – large and small. COVID-19 is one of those extraordinary times. Below are some of the things we are doing to help our company and our customers during this global crisis.

1. We go to extraordinary lengths to help our customers — consumers, small businesses, midsize companies, large corporations, and state and local governments.

First and foremost, we have to be prepared to operate under extremely adverse circumstances.

The significant economic fallout from this crisis reinforces the critical need to keep the global financial system fully functioning – and we recognize that our firm is an important part of the global economy.

Therefore, we incorporate plans for resilience in everything we do – resilience for hurricanes, data center failures, cyber attacks and other issues. And while we had not envisioned the effects of a pandemic like this one, all of this preparation has paid off – and we have been able to accomplish far more and far more quickly than we originally thought possible. It is absolutely essential that we be up and functioning for all of our customers each and every day. How else would we process $6 trillion in payments or buy and sell approximately $2 trillion in securities and foreign exchange transactions for our clients on a daily basis? And how else would we raise more than $2 trillion of credit and capital for our clients each year? Our branches, collectively, have 1 million customer visits each day, and our combined credit card and debit card transaction volume totals $1.1 trillion a year.

During this crisis, we have been utilizing our disaster recovery sites and implementing alternative work arrangements globally. We now have more than 180,000 employees working from home (and quite effectively), including traders, bankers, portfolio managers, and operations and call center teams across the globe. We are ensuring they continue to operate at the highest standards with the proper technological tools and access so they can serve their clients safely and seamlessly. Over the past few weeks, we have had nearly 150,000 concurrent virtual sessions – nearly five times our pre-pandemic average – and we have capacity in reserve to support significantly more demand if necessary.

We're taking significant steps to help our consumer customers.

After Superstorm Sandy, Hurricane Harvey and other devastating natural disasters around the globe, after wildfires ravaged California towns and after a number of other tragic events, we stepped up for our customers. Today, we are doing the same across the country as we work individually with customers facing COVID-19-related hardships.

We have been helping our customers, who tell us about their financial struggles as a result of the crisis, and are offering relief measures such as:

- Providing a 90-day grace period for mortgage and auto loan/lease payments and waiving any associated late fees.

- Removing minimum payment requirements on credit cards and waiving associated late fees.

- Not reporting payment deferrals such as late payments to credit bureaus for up-to-date clients.

- Continuing to responsibly lend to qualified consumers.

- Waiving or refunding some fees, including early withdrawal fees on certificates of deposit.

You can learn more about our customer response at: www.chase.com/stayconnected: opens overlay

Of our approximately 5,000 Chase branches, we have managed to keep three-quarters of them open – and safe – for our customers who need our services. In every one of our markets, almost all of our 2,300 branches with drive-up windows have remained open for business, allowing people to maintain a safe distance. Our 17,000 bankers have continued to take appointments and proactively reach out to customers – helping them manage their finances and use our digital tools – often letting customers stay home. In addition, the vast majority of our 16,850 ATMs are well-stocked and still functioning to provide needed cash to our customers. Our call centers have not fared as well; many of them have been effectively shut down by local restrictions. As the volume of calls has increased from customers seeking assistance, hold times have also increased. We have mobilized quickly to address this issue, reminding customers that our digital self-service capabilities are always available for them to check balances, deposit checks or make payments. Additionally, we have built new tools – digital and electronic – to allow customers to request relief without waiting for a specialist. And we are making it possible for our displaced phone specialists to work from home.

We are also taking significant action to support businesses – small, midsize and large – and state and local governments.

Clearly, some clients may be much more vulnerable than others – for example, transportation companies, hospitality enterprises, hospitals, utilities and, in particular, small businesses that do not have enough capital to withstand sudden and sustained downturns in income. JPMorgan Chase Institute research reveals that 50% of small businesses have less than 15 cash buffer days, reinforcing why small businesses are being heavily disrupted by the current crisis and will feel the effects for a significant period of time – even as more capital from the recent federal stimulus program reaches them.

To support businesses during this current crisis, we are doing the following:

- Prudently extending credit to businesses of all sizes for working capital and general corporate purposes. For example, in the past 60 days alone, we have extended $950 million in new loans to small businesses.

- Waiving and refunding fees for those businesses in need and finding ways to help more small businesses through resources available at the Small Business Administration.

- Servicing clients with additional credit through revolving facilities, when appropriate, and stepping in to try to help with credit when others can't or won't.

- Continuing in the ordinary course of business to sustain consumers, businesses and communities with about $500 billion of credit and capital raised every quarter.

- Continuing to maintain undrawn revolving commitments in our wholesale businesses, which totaled approximately $295 billion as of the close of business on March 31, 2020. Companies have already drawn down more than $50 billion of their revolvers to prepare themselves for the crisis (this already dramatically exceeds what happened in the global financial crisis). Many others have requested additional credit, which we have been offering judiciously – more than $25 billion of new credit extensions were approved in the month of March alone.

- Continuing the issuance of bonds for highly rated companies ($85 billion) – it may surprise you that the first quarter of 2020 will be our largest quarter for investment grade issuance, led by J.P. Morgan.

- Continuing to support vital institutions to keep our communities strong: Increased funding in March included, for example, $1.9 billion for hospitals and healthcare companies, $270 million for educational institutions, $360 million for nonprofits, and $240 million for state and local governments.

- Continuing to fund construction projects essential to our communities (affordable housing, food banks and grocery stores) through our $5 billion commitment.

Recognizing the extraordinary extension of new credit, mentioned above, and knowing there will be a major recession mean that we are exposing ourselves to billions of dollars of additional credit losses as we help both consumer and business customers through these difficult times. (We will provide more detail on these actions later in this letter.) Of course, we are in continual contact with our regulators about our actions and efforts.

We stand ready to assist the government in implementing stimulus package benefits to support the economy.

We applaud the speed with which the federal government and the Federal Reserve (the Fed), as well as other central banks around the world, put together a stimulus package and other funding benefits to help individuals, businesses, and state and local entities across the United States and beyond. Much remains to be done to assure these resources can be quickly and effectively rolled out. We hope to be at the forefront of using this assistance to help our customers get through what is certain to be a difficult next few months. We will not use this relief funding for ourselves.

2. We take excellent care of our employees.

Times like these reinforce that our employees are our most important asset – they are fundamental to the vibrancy and success of our company. Excellence in everything we do – from operations and technology to service and reputation – depends upon the abilities and character of our employees. Our vast and diverse team of people serves our customers and communities, builds the technology, makes the strategic decisions, manages the risks, determines our investments and drives innovation. Setting aside differing views of our complex world and the risks and opportunities ahead, it is inarguable that having such an extraordinary team — people with guts, brains and enormous capabilities who can navigate whatever circumstances bring – is what ensures our future prosperity.

In last year's letter, I wrote about the many ways we take excellent care of our employees: competitive wages and compensation, 401(k) retirement benefits, health benefits and wellness programs, extensive training programs, volunteer and employee engagement opportunities, generous parental leave policies and much more.

During this pandemic, we have also taken extensive steps to protect and support our employees and their families. For example:

- We continue to pay employees who are at home because they have had potential exposure to the virus or whose health is higher risk. Additionally, we provide paid medical leave to employees who are unwell.

- We have clinical staff internally to support our employees through this difficult time, whether it is fielding general inquiries related to COVID-19 or locating testing or other medical facilities.

- All employees are receiving five additional paid days off to help manage personal needs, which may include dependent care, child care or other issues.

- A special payment of up to $1,000 has been granted to full- and part-time employees whose job requires them to continue working on-site and generally whose annual cash compensation is less than $60,000.

- All branch employees are being paid for their regularly scheduled hours even if those hours are reduced or their branch is temporarily closed.

- For those who must go to work on-site, we are reinforcing both basic and enhanced personal and office hygiene measures to keep them, their colleagues and their clients safe. We have modified business operations, staggered shifts, changed seating arrangements, closed buildings to nonessential visitors and provided additional equipment where possible. We have also intensified nightly and daily cleaning of all offices and branches worldwide that remain open.

It's amazing how quickly we have mobilized and implemented work-from-home and other resiliency measures – in weeks instead of months or years. There are great lessons to be learned from this experience.

While conditions may sometimes be unusual and difficult, we are functioning smoothly. In fact, over the last month in certain parts of our company, we've had the highest volume and transaction totals we have ever seen.

Needless to say, this success would be impossible without our exceptional employees, and we recognize our responsibility to support both their professional and personal lives now more than ever.

A DIVERSE AND INCLUSIVE COMPANY IS A STRONGER COMPANY

While the health crisis we are facing supersedes all other topics in this year’s letter, the subject of diversity and inclusion is such an important one that I feel compelled to include it. As a firm, we have an unwavering commitment to integrity, fairness and responsibility. That’s why any instances of racist behavior and discrimination are so deeply unsettling.

Recently, Daniel Pinto and Gordon Smith, our Co-Presidents and Chief Operating Officers, sent a note to employees about steps we're taking to ensure our values reach all corners of our company.

Dear colleagues,

We are managing through uncertain times right now and recognize many of you are focusing much of your day on responding to the ongoing spread of the COVID-19 coronavirus. While this is a top priority for all of us, we want to make sure you know we haven't lost sight of our commitment to keeping you informed about our ongoing efforts to strengthen our culture. Now, more than ever, we need the best of everyone because only together will we get through these unprecedented times.

As you know, after the media reported on alleged discrimination in our firm last year, Jamie asked Gordon to lead an internal team to take a hard look at how we do business so that we could gain a deeper understanding of what more we can do to root out racism and discrimination anywhere it exists.

Challenging our people to be clear-eyed and open to change, we tasked many of our senior leaders from across the firm, from multiple lines of business and control functions, to evaluate our policies, procedures and programs firmwide, to ensure they are fair for all employees and customers. To be clear, we are looking across the whole firm and at everything we do.

As a result, we've identified a number of areas that, with enhanced, scaled or new programming or processes, would serve to improve our culture in important ways. For example, we focused on employee and customer complaints — examining common themes, where they originated and where opportunity exists to improve.

We also looked at how employee discretion may affect product accessibility across lines of business. We found opportunities to increase awareness about the firm's Diversity & Inclusion strategy, and we identified a need to expand our diversity recruitment efforts to help us hire more diverse talent, and to implement mandatory firmwide training.

While this work is ongoing, here are five initial areas where work is now underway, including:

Enhancing our employee feedback process

We are looking hard at how we treat an employee complaint when it comes in. We are already working to simplify escalation channels so employees are clear on where to submit complaints, in addition to further building out our capabilities across complaints to better understand the full scope of the individual's experience. Feedback suggests that employees are not always clear on where to submit complaints, so we are working to identify where improvements are needed.

Employees are encouraged to use existing channels to report inappropriate conduct or discrimination. We will continue to strengthen these “listening posts” and reporting channels in an effort to make sure every one of us feels safe and confident identifying and reporting inappropriate behavior.

Making it easier for customers to access products and services

We regularly review the products and services we offer to customers, and we are looking for ways to boost customer connectivity across our full spectrum of consumer products. To start, we are focusing on:

- Enhancing ease of navigating and guiding customers through our full range of products and services available across our entire branch network; and

- Re-evaluating the qualification requirements for new product features and benefits.

We will improve product parameters and strengthen monitoring tools to ensure the exercise of discretion works as intended.

Bolstering our hiring systems to build a more robust pipeline of diverse talent

Attracting the best talent can only be achieved through a dedicated focus on inclusive recruiting, so we are recommitting ourselves to this effort. We have made progress in this area, with programs such as Advancing Black Leaders, a program focused specifically on increased hiring, retention and development of talent from within the black community. Over the past four years, we have increased the number of black professionals in our most senior ranks, with the number of black managing directors and executive directors up by more than 50 percent.

In addition, we are expanding our specialized team dedicated to conducting more targeted outreach to recruit diverse talent. We will expand on our program to hold hiring managers and recruiters at the highest levels of the company accountable for hiring a diverse group of professionals.

Instituting required firmwide Diversity & Inclusion Training

In order to drive more diverse and inclusive behaviors amongst our leaders, managers, employees and customers, we are requiring diversity and inclusion training for all employees at various points throughout an employee lifecycle, including at the time of hire, and periodically thereafter. We expect all employees to fulfill these requirements.

Because the role of the manager is arguably the most critical role in promoting our culture deep into the organization, we will make additional manager training mandatory at the time of promotion to a people-manager role, and at the time of promotion to a senior leader role, in addition to other developmental moments for managers. We already have training in many parts of the organization, including programs like “Journey to Inclusive Teams” and the required unconscious bias training for branch managers. We will continue to enhance and embed this required training throughout the manager's career.

We know that it is essential for managers to be inclusive leaders and we will focus on helping them recognize ways they can be intentional about inclusion as they recruit, hire, retain and develop diverse talent.

Increasing the diversity of the businesses we partner with firmwide

We are fully committed to a fair, equitable and inclusive company for our customers, our employees, our partners and our suppliers. This is part of every manager's job, and they will be held accountable.

The diversity of the businesses we partner with across the firm is just as important as our employee diversity — from the small businesses to which we provide access to capital, to our asset managers, to our suppliers and to the companies we assist in bringing public.

We intend to increase diverse representation through structural process improvements in how we select partners and build our pipeline.

The firm will also continue to use data and research to further inform the development of products, services, employee programs and community investments that help address racial disparities in wealth building.

This all goes to say our work described above is representative of our deep commitment and is ongoing. It is not a “one and done” event. We will remain steadfast, continue to work now and in the future, and remain ever-vigilant in our effort to maintain a culture where racism cannot live or thrive. Over the next 30 days, each business will review their current strategies and contribute a plan to bring this to life and each business will be held accountable.

Let us say again, we are all the keepers of our culture and we are committed to ensuring that ours is one where all employees and customers are treated equally and fairly, and where all of us receive the opportunity and mutual respect we deserve.

I can assure you, it did not take one particular story to make us realize that a diverse and inclusive culture is important.

We know that too many people are being left behind – particularly in the black community. The Civil War ended more than 150 years ago, and we still have not come even close to parity. We need to do more as a nation, and we have more to do as a firm.

3. We make extraordinary efforts to lift up our communities, especially in challenging times.

I believe that our shareholders know we make extraordinary efforts to lift up our communities, both at a local level – supporting schools and work skills training, for example – and at the national level, helping to formulate policies that are good for countries. These policies affect healthcare, infrastructure, education and employment, including initiatives such as those that help people with a criminal background get a second chance.

We know that crises like COVID-19 create further inequities in society so it is even more important that we be present for those communities hit hard by the pandemic. JPMorgan Chase made a $50 million commitment to help address the immediate humanitarian crisis, as well as the long-term economic challenges people face. Funding will be deployed over time with particular focus on the most vulnerable people and communities, including:

- Immediate healthcare, food and other humanitarian relief globally;

- Help for existing nonprofit partners around the world that are responding to the crisis in their communities;

- Assistance to small businesses vulnerable to significant economic hardships in the United States, China and Europe.

There is a tremendous amount we do day to day – in addition to traditional banking – to help the communities in which we operate, including the following, some of which you might be surprised to know:

- We finance more than $5.5 billion in affordable housing each year (including residential and commercial lending and mortgages in low- and moderate-income communities).

- We provide small business loans in low- and moderate-income neighborhoods.

- We design products and services to promote the financial health of lower-income individuals.

- We support a number of employee- and community-based initiatives and philanthropic activities, including:

- Office of Military and Veterans Affairs, which sponsors mentorship, development and recognition programs to support the military and veterans working at the firm;

- Women on the Move, our global firmwide effort that empowers female employees, clients and consumers;

- The Service Corps, which mobilizes employee volunteers to help nonprofit organizations around the world;

- Advancing Black Pathways, a comprehensive program focused on providing more opportunities for black people and black-owned businesses because we know that opportunity is not always created equally;

- Entrepreneurs of Color Fund, which is expanding and provides minority entrepreneurs with access to capital, education and other resources.

- We expect to finance more than $100 billion in transactions aimed at supporting development in emerging market countries – in infrastructure, education, healthcare, agribusiness and industry, among other investments – to promote the United Nations' Sustainable Development Goals.

- We are huge supporters of regional and community banks, which are critical to many cities and small towns around the country. We bank approximately 500 of America's 5,000 regional and community banks. In 2019, we lent or raised a total of $2.6 billion in capital for them. In addition, we provide payment-processing services for them, we finance some of their mortgage activities, we advise on acquisitions, and we buy and sell securities for these banks. We also supply interest rate swaps and foreign exchange both for themselves – to help them hedge some of their exposures – and for their clients. For example, while many community banks were seeking more liquidity to serve their local communities amidst COVID-19 fears, we were able to help approximately 100 community banks secure $775 million in increased cash availability over a three-week period in March, delivering $1.9 billion of cash to support their branches and ATMs. This is not only a win for our clients but also for the communities in which they operate.

4. We are transparent with our shareholders: What they should expect regarding our financial and operating performance in 2020.

Of course, we do not know how this crisis will ultimately end, including how long it will last, how much economic damage it will do, or how fast or slow the recovery will be. We have always been serious about stress testing and run an enormous number of tests per week so that we are prepared for most crises. But as is often the case, this “actual new crisis” – while it shares attributes with what is being stress tested – is dramatically different from the expected.

We stopped buying back our stock: We have always held the position that the highest and best use of our equity is to reinvest it in our own business and, of course, to be able to withstand tough times. Halting buybacks was simply a very prudent action – we don't know exactly what the future will hold – but at a minimum, we assume that it will include a bad recession combined with some kind of financial stress similar to the global financial crisis of 2008. Our bank cannot be immune to the effects of this kind of stress.

We will share in detail our latest thinking on the impact this crisis will have on our financials in our first quarter earnings release in mid-April; however, to put it in context, here is how our shareholders can think broadly about a reasonable range of outcomes.

Our 2019 pretax earnings were $48 billionfootnote3 – a huge and powerful earnings stream that enables us to absorb the loss of revenues and the higher credit costs that inevitably follow a crisis. For comparison, the Comprehensive Capital Analysis and Review (CCAR) results for 2020 that we submitted to the Federal Reserve in 2019 (which assumed outcomes like U.S. unemployment peaking at 10% and the stock market falling 50%) showed a decline in revenue of almost 20% and credit costs of approximately $20 billion more than what we experienced in 2019. We believe we would perform better than this if the Fed's scenario were to actually occur. But even in the Fed's scenario, we would be profitable in every quarter.footnote4 These stress test results also show that following such a meaningful reduction in our revenue (and assuming we continue to pay dividends), our common equity Tier 1 (CET1) ratio would likely hold at a very strong 10%, and we would have in excess of $500 billion of liquid assets.

Additionally, we have run an extremely adverse scenario that assumes an even deeper contraction of gross domestic product, down as much as 35% in the second quarter and lasting through the end of the year, and with U.S. unemployment continuing to increase, peaking at 14% in the fourth quarter. Even under this scenario, the company would still end the year with strong liquidity and a CET1 ratio of approximately 9.5% (common equity Tier 1 capital would still total $170 billion). This scenario is quite severe and, we hope, unlikely. If it were to play out, the Board would likely consider suspending the dividend even though it is a rather small claim on our equity capital base. If the Board suspended the dividend, it would be out of extreme prudence and based upon continued uncertainty over what the next few years will bring.

It is also important to be aware that in both our central case scenario for 2020 results and in our extremely adverse scenario, we are lending – currently or plan to do so – an additional $150 billion for our clients' needs. Despite this, our capital resources and liquidity are very strong in both models. We have over $500 billion in total liquid assets and an incremental $300+ billion borrowing capacity at the Federal Reserve and Federal Home Loan Banks, if needed, to support these loans, as well as meet our liquidity requirements (these numbers do not include the potential use of some of the Fed's newly created facilities). We could, of course, make our capital and liquidity buffer better by restricting our activities, but we do not intend to do that – our clients need us.

I would like to point out that, as we get closer to the extremely adverse scenario, current regulatory constraints will limit additional actions we can take to help clients – in spite of the extraordinary amount of capital and liquidity we could deploy.

5. We are working closely with all levels of government during this crisis — and while we will participate in government programs to address the severe economic challenges, we will not request any regulatory relief for ourselves.

We are just beginning to analyze and work with the government on all of their various programs. For the most part, these initiatives will need the deep involvement of the private sector to be properly executed. We intend to do everything we can – and as soon as possible – to ensure that government support is reaching the people who need it most.

We applaud and support the recent actions the U.S. Department of the Treasury and the Federal Reserve have taken to try to mitigate the economic impact of the COVID-19 turmoil. The Fed's overwhelming actions have already dramatically reduced the financial stress in the system, and there is still more they could do if they need to. For example, balance sheet expansion, additional lending facilities, and changes to capital and liquidity requirements are steps designed to ensure that more capital will flow through the system, which will ultimately allow us to help more families and small businesses. These actions would bolster the U.S. economy with no impact on safety, soundness or regulatory oversight. We are working with the government to make sure such crisis-relief measures are structured to work effectively – there are a significant number of details that need to be resolved, which I will not go into here.

While we will aggressively help our customers take advantage of these new programs (though we must take action to protect ourselves from ongoing – and, more important, future – litigation risk), we want our shareholders to know that we have not requested any regulatory relief for ourselves. Saying that we will not ask for regulatory relief does not mean the government shouldn't change some rules and regulations, however. For example, some rules can improperly prevent healthy, well-capitalized banks from lending freely in times of stress. This can hurt customers as the crisis deepens. Leaving high-quality, available liquidity undeployed in times of need is an opportunity forever lost.

I have written in detail in past letters that the regulatory system is in need of both reform and recalibration – not because we want it to happen but because it would be good for a deepening and widening of the financial system – something that would benefit all Americans. While a lot of the rules were constructive and made the financial system stronger, we are now seeing the impact of poorly coordinated, poorly calibrated and poorly organized rulemaking. After the crisis subsides (and it will), our country should thoroughly review all aspects of our preparedness and response. And we should use the opportunity to closely review the economic response and determine whether any additional regulatory changes are warranted to improve our financial and economic system. There will be a time and place for that – but not now.

6. We need a plan to get safely back to work.

It is hoped that the number of new COVID-19 cases will decrease soon and – coupled with greatly enhanced medical capabilities (more beds, proper equipment where it is needed, adequate testing) – the healthcare system is equipped to take care of all Americans, both minimizing their suffering and maximizing their chance of living. Once this occurs, people can carefully start going back to work, of course with proper social distancing, vigilant hygiene, proper testing and other precautions. There are many jobs that can be safely done; however, employees in certain companies should return to business as usual only if the Centers for Disease Control and Prevention (CDC) and other government entities deem it safe to do so.

In addition, this “return to work” process could be accelerated if federal, state and local governments make tests widely available that allow people to certify that they have contracted and recovered from the disease, have the necessary antibodies to prevent them from getting sick again and are not infectious to anyone. Initially, we need a buffer period of days or weeks for people to be tested, and then for those who test negative for the virus, we need to discover whether virus antibodies appear through serology testing. Both the CDC and private companies are scrambling to produce such tests: The U.K. has ordered 3.5 million of them, Germany will use them to issue immunity certificates to COVID-19 survivors, and China and Singapore already are using tests to determine how extensively the virus spread in large populations in order to measure the true infection rate. In the United States, the Food and Drug Administration is allowing doctors to use these serology tests to identify recovered patients whose antibodies could treat emergency cases of the disease.

The country was not adequately prepared for this pandemic – however, we can and should be more prepared for what comes next. Done right, a disciplined transition would maximize the health of Americans and minimize the time, extent and suffering caused by the economic downturn.

7. We need to come together: My fervent hope for America.

Sometimes extraordinary events in history can cause a change in the body politic. As a nation, we were clearly not equipped for this global pandemic, and the consequences have been devastating. But it is forcing us to work together, and it is improving civility and reminding us that we all live on one planet. E Pluribus Unum.

I am hoping that civility, humanity, empathy and the goal of improving America will break through.

We have the resources to emerge from this crisis as a stronger country. America is still the most prosperous nation the world has ever seen. We are blessed with the natural gifts of land; all the food, water and energy we need; the Atlantic and Pacific oceans as natural borders; and wonderful neighbors in Canada and Mexico. And we are blessed with the extraordinary gifts from our Founding Fathers, which are still unequaled: freedom of speech, freedom of religion, freedom of enterprise, and the promise of equality and opportunity. These gifts have led to the most dynamic economy the world has ever seen – one that nurtures vibrant businesses large and small, exceptional universities, and a welcoming environment for innovation, science and technology. America was an idea borne on principles, not based upon historical relationships and tribal politics. It has and will continue to be a beacon of hope for the world and a magnet for the world's best and brightest.

Of course, America has always had its flaws. The current pandemic is only one example of the bad planning and management that have hurt our country: Our inner city schools don't graduate half of their students and don't give our children an education that leads to a livelihood; our healthcare system is increasingly costly with many of our citizens lacking any access; and nutrition and personal health aren't even being taught at many schools. Obesity has become a national scourge. We have a litigation and regulatory system that cripples small businesses with red tape and bureaucracy; ineffective infrastructure planning and investment; and huge waste and inefficiency at both the state and federal levels. We have failed to put proper immigration policies in place; our social safety nets are poorly designed; and the share of wages for the bottom 30% of Americans has effectively been going down. We need to acknowledge these problems and the damage they have done if we are ever going to fix them.

There should have been a pandemic playbook. Likewise, every problem I noted above should have detailed and nonpartisan solutions. As we have seen in past crises of this magnitude, there will come a time when we will look back and it will be clear how we – at all levels of society, government, business, healthcare systems, and civic and humanitarian organizations – could have been and will be better prepared to face emergencies of this scale. While the inclination of some will be to finger-point and look for blame, I hope we can avoid that. I also hope we can avoid people using times of crisis to argue for what they already believe. We need to demand more of ourselves and our leaders if we want to prevent or mitigate these disasters. This can be a moment when we all come together and recognize our shared responsibility, acting in a way that reflects the best of all of us. As President Kennedy historically said, “Ask not what your country can do for you – ask what you can do for your country.”

My fervent hope is that America rolls up its sleeves and starts to attack these problems. Fixing them would better prepare us for future catastrophes, create better economic outcomes for everyone (with policies that aim to maximize economic growth, driving the best potential outcomes), improve income inequality, protect the most vulnerable and foster economic growth that is more resilient, which would also strengthen America's role in the world. We must never forget that America's economic prosperity is a necessary foundation for our military capability, which keeps us free and strong and is essential to world peace. These issues could all be tackled while preserving the freedoms ascribed by our Founding Fathers: life, liberty and the pursuit of happiness, freedom of speech, freedom of religion and freedom of enterprise, which means the free movement of capital and labor (meaning you can work where you want and for whom you want). At the end of the day, the pursuit of happiness, our freedoms and free enterprise are inseparable.

If we acknowledge our problems and work together, we can lift up those who need help and society as a whole. Business and government collaborating together can conquer our biggest challenges.

IN CLOSING

While I have a deep and abiding faith in the United States of America and its extraordinary resiliency and capabilities, we do not have a divine right to success. Our challenges are significant, and we should not assume they will take care of themselves. Let us all do what we can to strengthen our exceptional union.

I would like to express my deep gratitude and appreciation for the employees of JPMorgan Chase, and I’d also like to thank all of you who shared your good wishes with me while I was recuperating from my recent heart surgery. From this letter, I hope shareholders and all readers gain an appreciation for the tremendous character and capabilities of our people and how they have helped communities around the world. They have faced these times of adversity with grace and fortitude. I hope you are as proud of them as I am. Finally, the countries and citizens of the global community will get through this unprecedented situation, undoubtedly stronger for it. Together, we will rise to the challenge.

Jamie Dimon

Chairman and Chief Executive Officer

April 6, 2020

APPENDIX

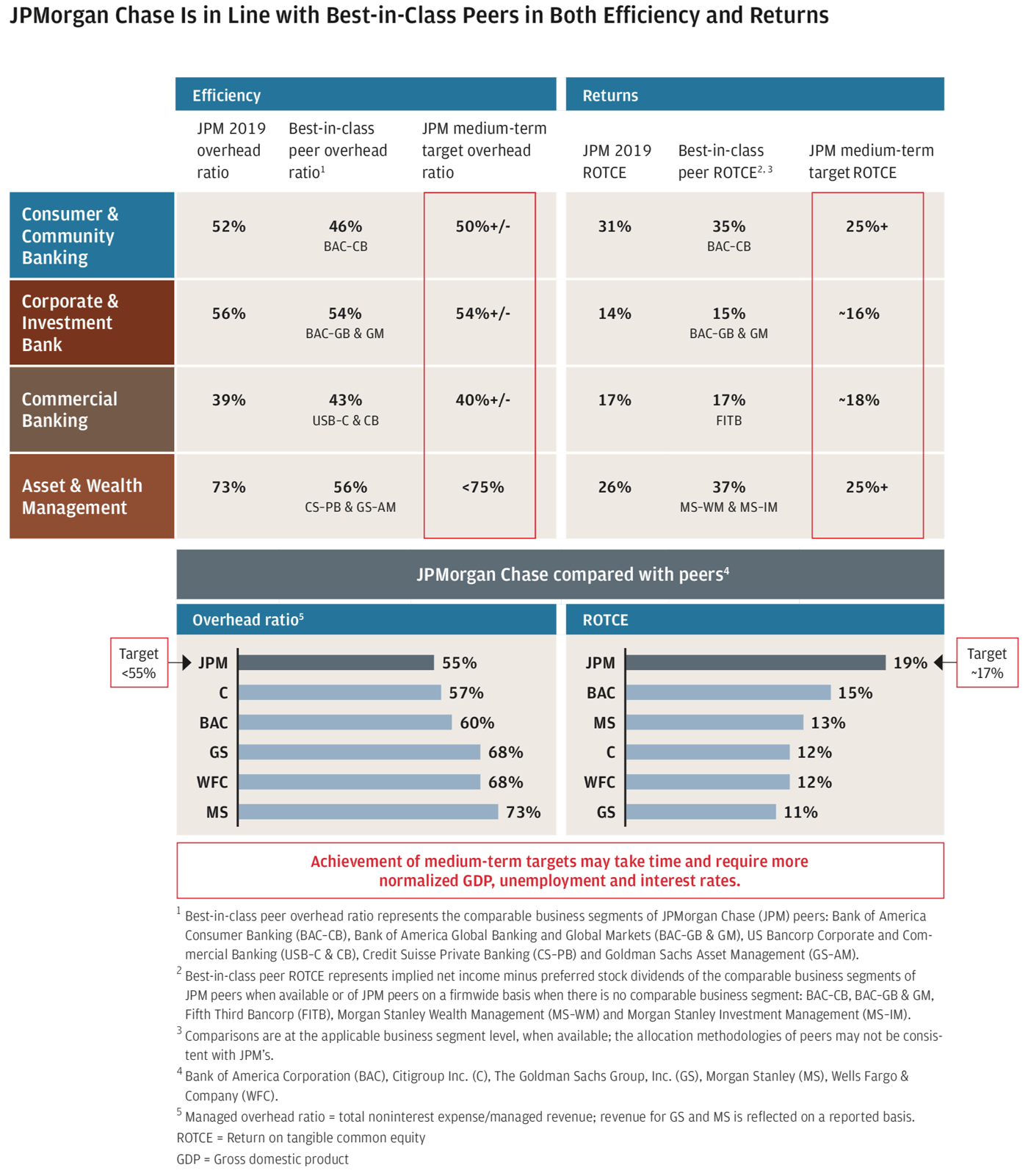

While we never expect to be best in class every year in every business, we normally compare well with our best-in-class peers. The chart below shows our performance generally, by business, versus our competitors in terms of efficiency and returns.

- 1

- Represents managed revenue

- 2

- Adjusted net income, a non-GAAP financial measure, excludes $2.4 billion from net income in 2017 as a result of the enactment of the Tax Cuts and Jobs Act.

- 3

- Represents managed pretax income.

- 4

- We are adjusting these CCAR results for the global market shock trading losses and operational losses – and there have been none in this crisis.