Dear Fellow Shareholders,

We are facing challenges at every turn: a pandemic, unprecedented government actions, a strong recovery after a sharp and deep global recession, a highly polarized U.S. election, mounting inflation, a war in Ukraine and dramatic economic sanctions against Russia. While all this turmoil has serious ramifications on our company, its effect on the world — with the extreme suffering of the Ukrainian people and the potential restructuring of the global order — is far more important.

Adding to the disruption, these events are unfolding while America remains divided within its borders, with many arguing that it has lost its essential leadership role outside of its borders and around the world. But during this difficult time, we have a moment to put aside our differences, offer solutions and work with others in the Western world to come together in defense of democracy and essential freedoms, including free enterprise. We have seen America, in partnership with other countries around the globe, come together previously during instances of conflict and crisis. This juncture is also a moment when our country needs to work across the private and public sectors to lead once again by, among other remediations, improving American competitiveness and better fulfilling equal access to opportunity for all. JPMorgan Chase, a company that has historically worked across borders and boundaries, will do its part to ensure the global economy is safe and secure. I discuss these themes later in this letter.

Although I begin this annual letter to shareholders in a challenging landscape, I remain proud of what our company and our hundreds of thousands of employees around the world have achieved, collectively and individually. As you know, we have long championed the essential role of banking in a community — its potential for bringing people together, for enabling companies and individuals to reach for their dreams, and for being a source of strength in difficult times. Throughout these past two challenging years, we never stopped doing all the things we should be doing to serve our clients and our communities.

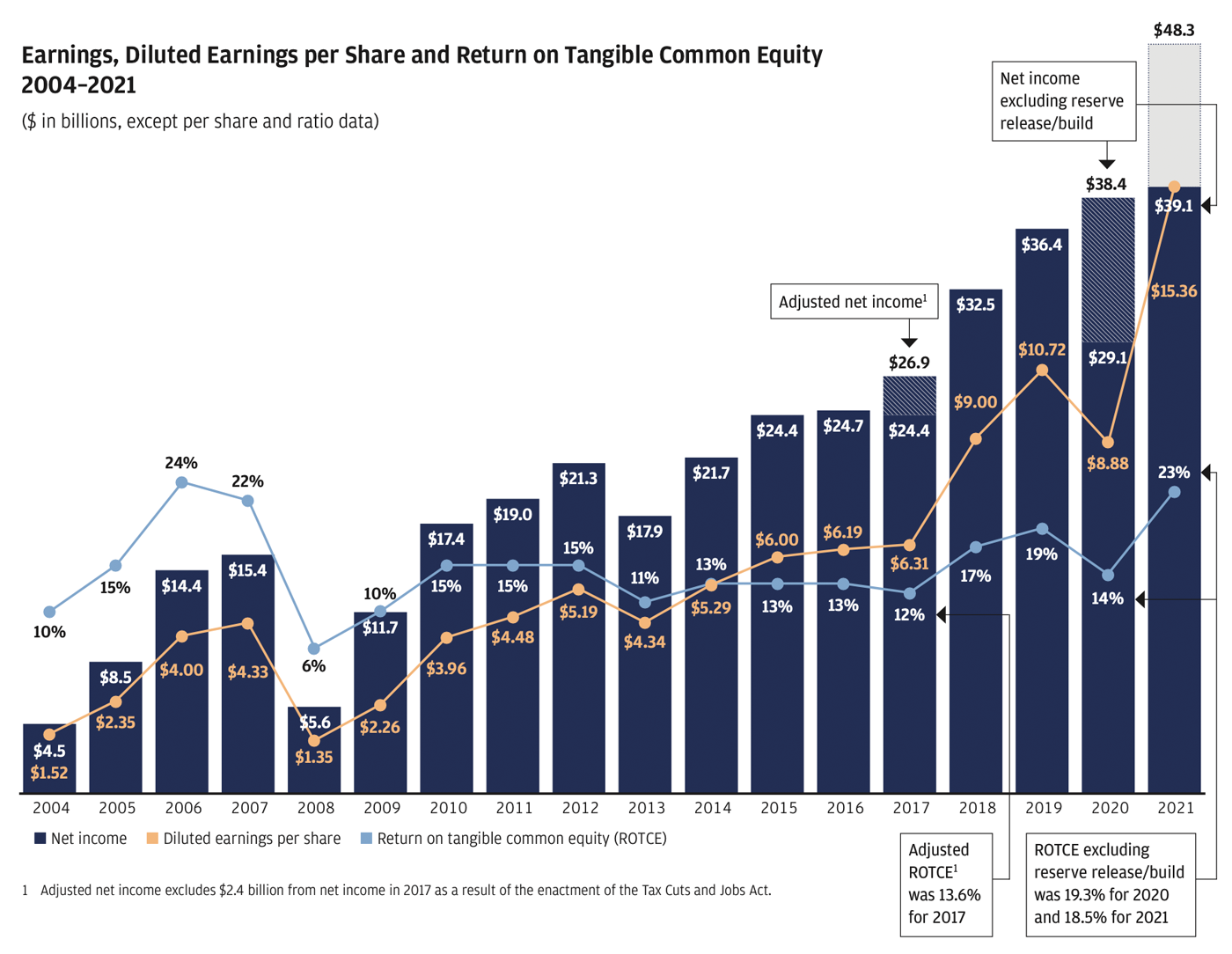

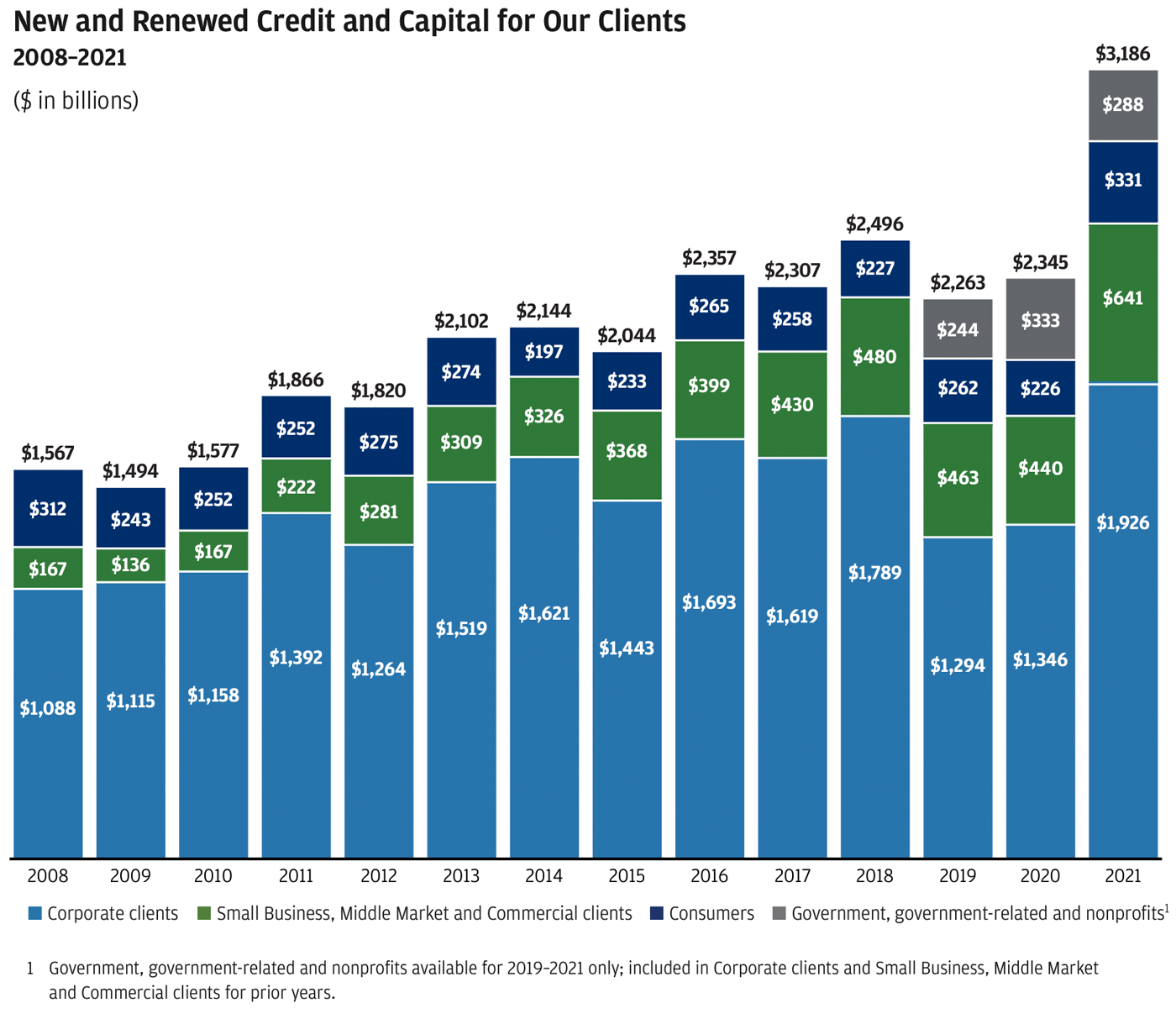

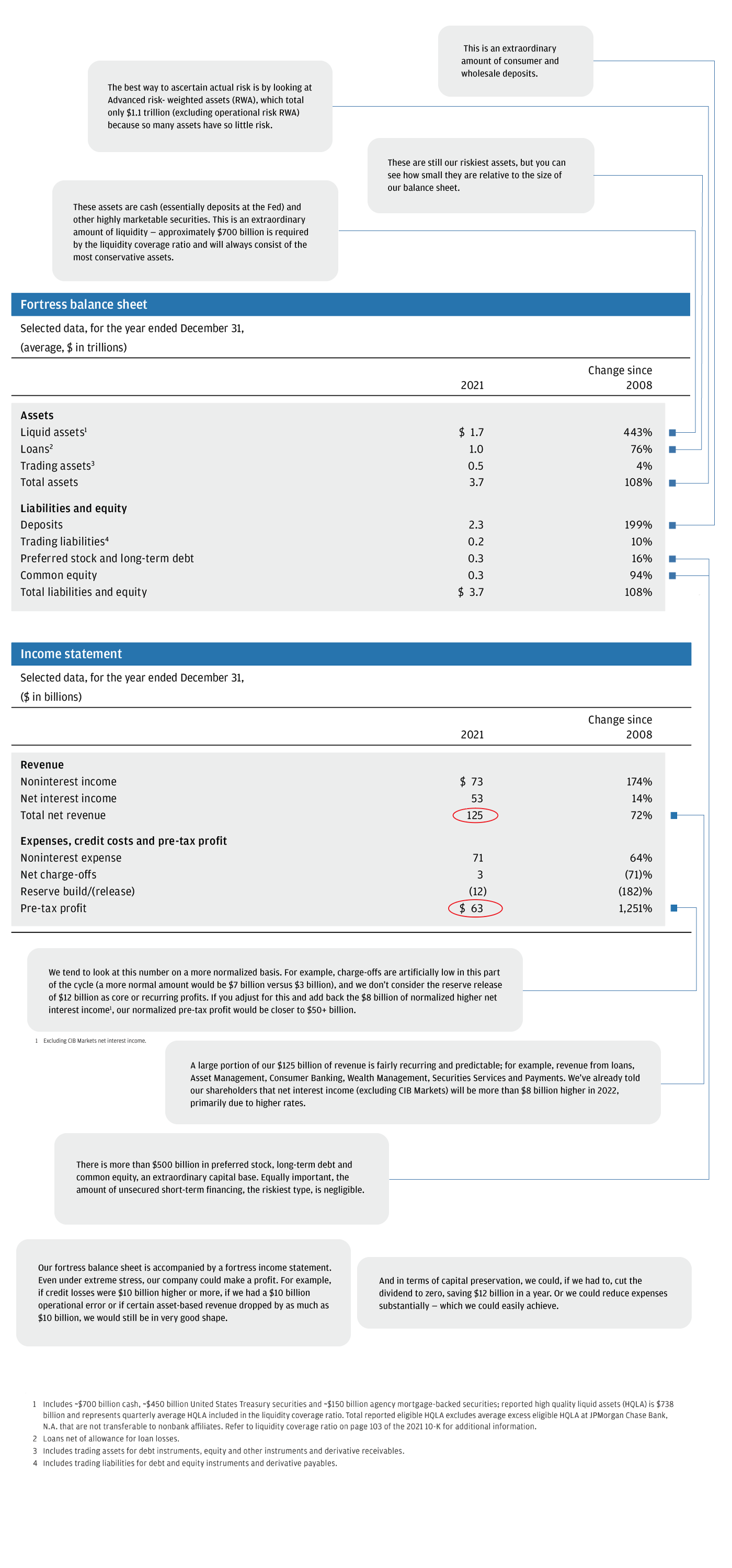

Looking back on the last year and the past two decades — starting from my time as CEO of Bank One in 2000 — it is clear that our financial discipline, constant investment in innovation and ongoing development of our people are what enabled us to persevere in our steadfast dedication to help clients, communities and countries throughout the world. 2021 was another strong year for JPMorgan Chase, with the firm generating record revenue, as well as setting numerous other records in each of our lines of business. We earned $48.3 billion in net income on revenue of $125.3 billion versus $29.1 billion on revenue of $122.9 billion in 2020, reflecting strong underlying performance across our businesses. Included in the $48.3 billion is $9.2 billion after tax in reserve releases due to the volatility introduced by the new current expected credit loss accounting standard. We have pointed out repeatedly that we do not consider these reserve releases core or recurring profits because they are driven by hypothetical, probability-weighted scenarios. Excluding these reserve releases, we still earned 18% on tangible equity — an extremely healthy number. We generally grew market share across our businesses and continued to make significant investments in products, people and technology, all while maintaining credit discipline and a fortress balance sheet. In total, we extended credit and raised capital of $3.2 trillion for large and small businesses, governments and U.S. consumers.

I’d like to note some steadfast principles that are worth repeating. The first is that while JPMorgan Chase stock is owned by large institutions, pension plans, mutual funds and directly by individual investors, in almost all cases, the ultimate beneficiaries are individuals in our communities. More than 100 million people in the United States own stock, and a large percentage of these individuals, in one way or another, own JPMorgan Chase stock. Many of these people are veterans, teachers, police officers, firefighters, healthcare workers, retirees or those saving for a home, education or retirement. Your management team goes to work every day recognizing the enormous responsibility that we have to our shareholders.

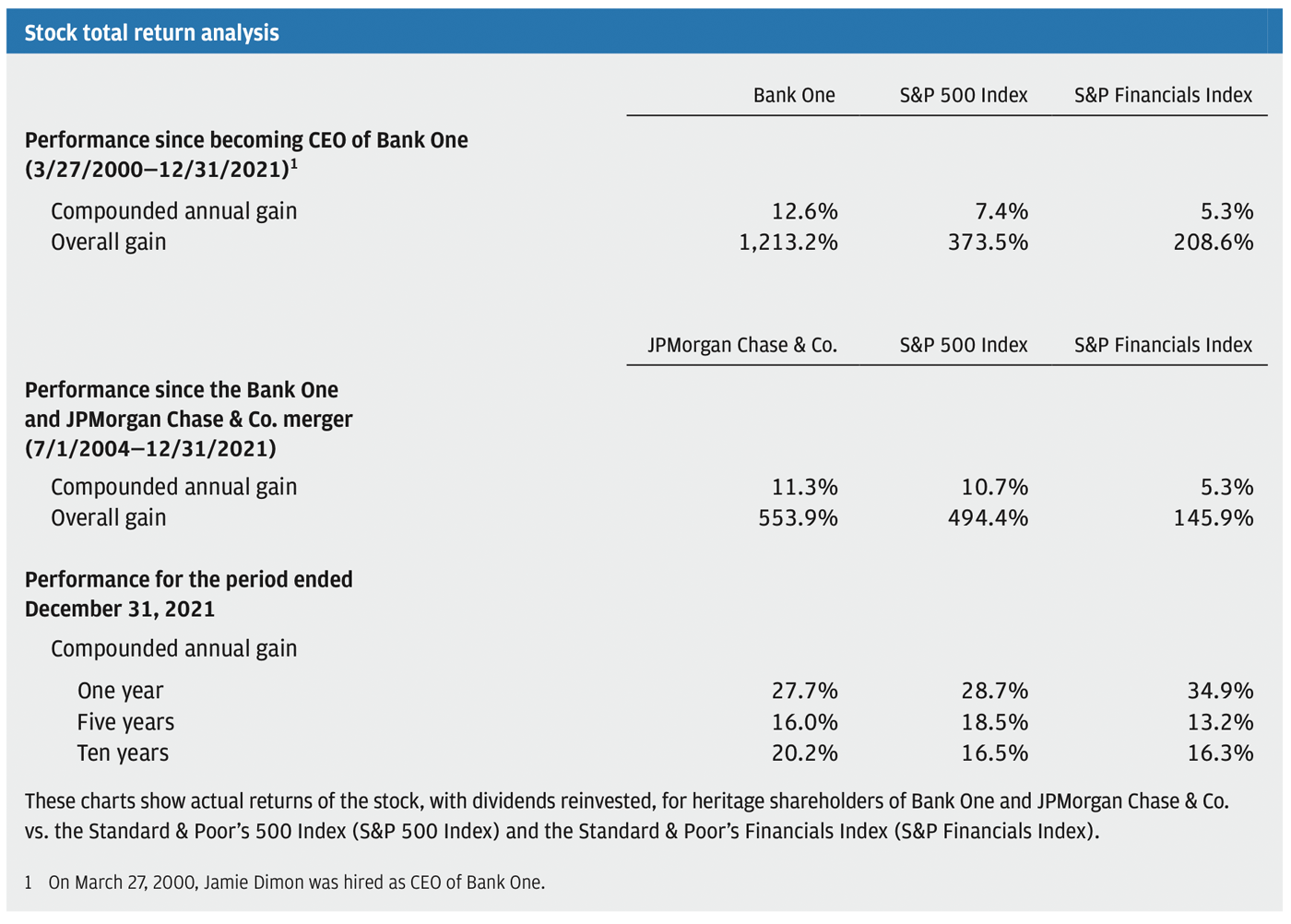

Second, while we don’t run the company worrying about the stock price in the short run, in the long run our stock price is a measure of the progress we have made over the years. This progress is a function of continual investments in our people, systems and products, in good and bad times, to build our capabilities. Whether looking back 10 years or since the JPMorgan Chase/Bank One merger in 2004, these investments have resulted in our stock’s significant outperformance of the Standard & Poor’s 500 Index and the Standard & Poor’s Financials Index. These important investments will also drive our company’s future prospects and position it to grow and prosper for decades.

We have consistently described to you, our shareholders, the basic principles and strategies we use to build this company — from maintaining a fortress balance sheet, constantly investing and nurturing talent to fully satisfying regulators, continually improving risk, governance and controls, and serving customers and clients while lifting up communities worldwide.

If you look deeper, you will find that our success and accomplishments are founded on our commitment to our shareholders. Shareholder value can be built only if you maintain a healthy and vibrant company, which means doing a good job taking care of your customers, employees and communities. Conversely, how can you have a healthy company if you neglect any of these stakeholders? As we have learned in 2021, there are myriad ways an institution can demonstrate its compassion for its employees and its communities while still upholding shareholder value.

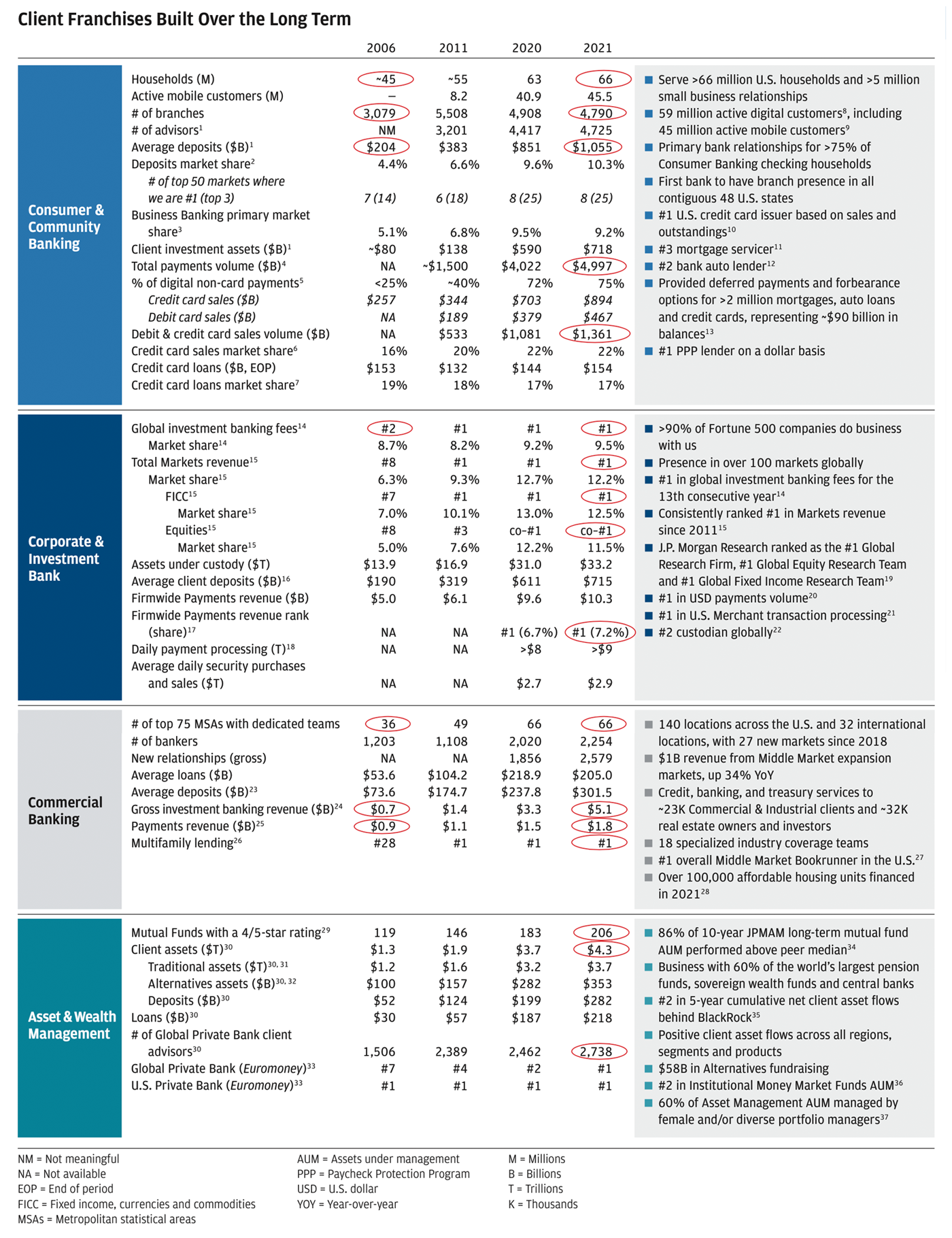

Adhering to our basic principles and strategies allows us to drive good organic growth and properly manage our capital (including dividends and stock buybacks), as we have consistently demonstrated over the past decades. All of this is shown in the charts below, which illustrate how we have grown our franchises, how we compare with our competitors and how we look at our fortress balance sheet. I invite you to peruse them at your leisure. In addition, I urge you to read the CEO letters in this Annual Report, which will give you more specific details about our businesses and our plans for the future.

There are two other critical points I would like to make. We strive to build enduring businesses, and we are not a conglomerate — all our businesses rely on and benefit from each other. Both of these factors help generate our superior returns. But, despite our best efforts, the moats that protect this company are not particularly deep — and we face extraordinary competition. I have written about this reality extensively in the past and cover it in more detail in this letter. However, it is the hand we have been dealt, and we will play it as best we can.

My friend, Warren Buffett, spoke in his letter this year about his silent partner — the U.S. government — noting that all his company’s success is predicated upon the extraordinary conditions our country creates. He is right to say to his shareholders that when they see the flag, they should all say thank you. We should, too. I do just want to note that in our case, the silent partner is not so silent. JPMorgan Chase is a healthy and thriving company, and we always want to give back and pay our fair share. We do — and we want it to be spent well and have the greatest impact. To give you an idea of where our taxes and fees go: In the last 10 years, we paid $42 billion in federal, state and local taxes in the United States and $17 billion in taxes outside of the United States. We also paid the Federal Deposit Insurance Corporation $11 billion so that it has the resources to cover the failure of any major American bank.

Finally, the basis of our success is our people. They are the ones who serve our customers and communities, build the technology, make the strategic decisions, manage the risks, determine our investments and drive innovation. Whatever your view is of the world’s complexity and the risks and opportunities ahead, having a great team of people — with guts, brains, integrity and enormous capabilities to navigate personally challenging circumstances while maintaining high standards of professional excellence — is what ensures our prosperity, now and in the future.

Read footnoted information here

Read footnoted information here

Within this letter, I discuss the following:

Significant Geopolitical and Economic Challenges

- The U.S. economy is strong.

- Persistent inflation will require rising interest rates and a massive but necessary shift from quantitative easing to quantitative tightening.

- The war in Ukraine and the sanctions on Russia, at a minimum, will slow the global economy — and it could easily get worse.

- The confluence of these factors may be unprecedented.

- The war could affect geopolitics for decades.

- How are we managing our global bank in these difficult markets and complex times?

The Extraordinary Need for Strong American Leadership

- While America has flaws, its essential strengths endure.

- To maintain our competitiveness, our country must regain its competence — and our principles, including free enterprise, need to be nurtured.

- Government, with its unique powers, has an essential role in managing the economy — but it needs to be realistic about its limitations on what it can and cannot do.

- We must confront the Russia challenge with bold solutions.

- A strong America need not fear a rising China.

- There are compelling reasons for global trade restructuring

- We can have a path forward for U.S. policy: Agree on what we want, then execute.

- Banks performed magnificently during the COVID-19 crisis.

- The role of banks in the global financial system is diminishing.

- Possibly more important: The role of public companies in the global financial system is also diminishing.

- More regulation is coming — 10 years after the crisis, we are still rolling out Basel IV — and we need more thoughtful calibration of the rules.

- How should we address our G-SIB conundrum?

- Banks need to acknowledge the dramatically changing competitive landscape.

Investments and Acquisitions: Determining the Best Use of Capital and Assessing ROIs

- Some investments generate predictable returns.

- Acquisitions should pay for themselves — and each one has its own logic.

- We want to build upon our global footprint.

- We make extensive investments in technology for a broad range of reasons, from improving operations and security to enhancing our products and services.

Updates on Specific Issues Facing Our Company

- We are vigilant against cyber attacks.

- Our commitment to sustainability is informed by energy realities.

- Progress continues in our diversity, equity and inclusion efforts.

- Morgan Health is helping us lead in healthcare transformation.

- We continue to support data-driven policymaking through the JPMorgan Chase PolicyCenter and Institute.

- We join other companies in evolving our vision of the workplace.

Management Lesson: The Benefit of Purpose and the Tremendous Value of Work

- Perfect your Picasso — have something to strive for and motivate you.

- Recognize the tremendous value of work.

- Nurture the extraordinary value of trust.

- Combat the enemy within.

- Drive high performance, the right way.

- Retaining talent is important and so is life outside of work.

Significant Geopolitical and Economic Challenges

America and the rest of the world are facing the confluence of three important and conflicting forces: 1) a strong U.S. economy, which, we hope, has COVID-19 in its rearview mirror; 2) high inflation, which means rising interest rates and, importantly, the reversal of quantitative easing (QE); and 3) the war in Ukraine and the accompanying humanitarian crisis, with its impact on the global economy in the short term, as well as its significant impact on the geopolitics of the future. These factors will likely have a meaningful effect on the economy over the next few years and on geopolitics for the next several decades.

I should remind the reader that we normally don’t worry about — or even try to predict — normal fluctuations of the economy. In all times, we are prepared for difficult markets and severe recessions, as well as for unpredictable events, not only so we will survive them but also so we can be there for our clients when they need us the most. However, sometimes there are powerful underlying structural trends that we must try to understand since their impact can be so large, with widespread impact on many parts of human existence.

The U.S. economy is strong.

In 2020 and 2021, enormous QE — approximately $4.4 trillion, or 18%, of 2021 gross domestic product (GDP) — and enormous fiscal stimulus (which has been and always will be inflationary) — approximately $5 trillion, or 21%, of 2021 GDP — stabilized markets and allowed companies to raise enormous amounts of capital. In addition, this infusion of capital saved many small businesses and put more than $2.5 trillion in the hands of consumers and almost $1 trillion into state and local coffers. These actions led to a rapid decline in unemployment, dropping from 15% to under 4% in 20 months — the magnitude and speed of which were both unprecedented. Additionally, the economy grew 7% in 2021 despite the arrival of the Delta and Omicron variants and the global supply chain shortages, which were largely fueled by the dramatic upswing in consumer spending and the shift in that spend from services to goods. Fortunately, during these two years, vaccines for COVID-19 were also rapidly developed and distributed.

In today’s economy, the consumer is in excellent financial shape (on average), with leverage among the lowest on record, excellent mortgage underwriting (even though we’ve had home price appreciation), plentiful jobs with wage increases and more than $2 trillion in excess savings, mostly due to government stimulus. Most consumers and companies (and states) are still flush with the money generated in 2020 and 2021, with consumer spending over the last several months 12% above pre-COVID-19 levels. (But we must recognize that the account balances in lower-income households, smaller to begin with, are going down faster and that income for those households is not keeping pace with rising inflation.)

Today’s economic landscape is completely different from the 2008 financial crisis when the consumer was extraordinarily overleveraged, as was the financial system as a whole — from banks and investment banks to shadow banks, hedge funds, private equity, Fannie Mae and many other entities. In addition, home price appreciation, fed by bad underwriting and leverage in the mortgage system, led to excessive speculation, which was missed by virtually everyone — eventually leading to nearly $1 trillion in actual losses.

During 2020 and 2021, many aberrant things also happened: 2 million people retired early; the supply of immigrant workers dropped by 1 million due to immigration policies; available jobs skyrocketed to 11 million (again unprecedented); and job seekers dropped to 5 million. Wage growth accelerated dramatically, particularly in low-income jobs. We should not be unhappy that wages are going up — and that workers have more choices and are making different decisions — in spite of the fact that this causes some difficulties for business. House prices surged during the pandemic (housing became and still is in extremely short supply), and asset prices remained high, some, in my view, in bubble territory. Inflation soared to 7%; while clearly some of this rise is transitory due to supply chain shortages, some is not, because higher wages, higher housing costs, and higher energy and commodity prices will persist (more to come on this later). All these factors will continue in 2022, driving further growth as well as continued inflation. One additional point: Consumer confidence and consumer spending have diverged dramatically, with consumer confidence dropping. Spending, however, is more important, and the drop in consumer confidence may be in reaction to ongoing fatigue from the pandemic shutdown and concerns over high inflation.

Persistent inflation will require rising interest rates and a massive but necessary shift from quantitative easing to quantitative tightening.

It is easy to second-guess complex decisions after the fact. The Federal Reserve (the Fed) and the government did the right thing by taking bold dramatic actions following the misfortune unleashed by the pandemic. In hindsight, it worked. But also in hindsight, the medicine (fiscal spending and QE) was probably too much and lasted too long.

I do not envy the Fed for what it must do next: The stronger the recovery, the higher the rates that follow (I believe that this could be significantly higher than the markets expect) and the stronger the quantitative tightening (QT). If the Fed gets it just right, we can have years of growth, and inflation will eventually start to recede. In any event, this process will cause lots of consternation and very volatile markets. The Fed should not worry about volatile markets unless they affect the actual economy. A strong economy trumps market volatility.

This is in no way traditional Fed tightening — and there are no models that can even remotely give us the answers. I have always been critical of people’s excessive reliance on models — since they don’t capture major catalysts, such as culture, character and technological advances. And in our current situation, the Fed needs to deal with things it has never dealt with before (and are impossible to model), including supply chain issues, sanctions, war and a reversal of QE in the face of unparalleled inflation. Obviously, the Fed always needs to be data-dependent, and this is true today more than ever before. However, the data will likely continue to be inconsistent and volatile — and hard to read. The Fed should strive for consistency but not when it’s impossible to achieve.

One thing the Fed should do, and seems to have done, is to exempt themselves — give themselves ultimate flexibility — from the pattern of raising rates by only 25 basis points and doing so on a regular schedule. And while they may announce how they intend to reduce the Fed balance sheet, they should be free to change this plan on a moment’s notice in order to deal with actual events in the economy and the markets. A Fed that reacts strongly to data and events in real time will ultimately create more confidence. In any case, rates will need to go up substantially. The Fed has a hard job to do so let’s all wish them the best.

The shift from QE to QT will cause a massive change in the flow of funds in and out of Treasury bonds and, therefore, all securities. Our situation today is completely unlike the monetary policy adjustments following the great financial crisis of 2008. When central banks were buying bonds from 2008 to 2014, there was a tremendous amount of deleveraging in the rest of the financial world. Clearly, this deleveraging slowed growth, which in turn reduced the need for business investment. In addition, banks were required to buy Treasuries to meet their new liquidity requirements. This action reduced both lending and the money supply in the years after the great financial crisis. Low growth also led to less capital needed, and QE added to the savings glut. I am still convinced that these are some of the primary reasons our economy experienced low growth and so-called “secular stagnation.”

In today’s economic environment, countries’ central banks do not need to increase their foreign exchange reserves as they did after the great financial crisis, and banks don’t need to buy Treasuries to improve their liquidity ratios. This time around, business investment will likely be higher, both because of higher growth and because the capital required to combat climate change is estimated to be more than $4 trillion annually. Finally, governments will also need to borrow more money — not less.

This massive change in the flow of funds triggered by Fed tightening is certain to have market and economic effects that will be studied for decades to come. Our bank is prepared for drastically higher rates and more volatile markets.

The war in Ukraine and the sanctions on Russia, at a minimum, will slow the global economy — and it could easily get worse.

The effects of geopolitics on the economy are harder to predict. For as much attention as it gets, geopolitics over the past 50 years have rarely disrupted the global economy in the short run (think Afghanistan; Iraq; Korea; Vietnam; conflicts between Pakistan and India, India and China, China and Vietnam, Russia and China; and at least 10 other upheavals and wars in the Middle East). The 1973 Organization of the Petroleum Exporting Countries, or OPEC, oil embargo was an exception, when the sharp jump in oil prices pushed the world into a global recession. However, it’s important to point out that while past geopolitical events often did not have short-term economic effects, they frequently had large, longer-term consequences — such as America’s experience with the Vietnam War, which drove the great inflation of the 1970s and 1980s and tore the body politic apart.

As I write this letter, the war in Ukraine has been raging for well over a month and is creating a significant refugee crisis. We do not know what its outcome ultimately will be, but the hostilities in Ukraine and the sanctions on Russia are already having a substantial economic impact. They have roiled global oil, commodity and agricultural markets. We expect the fallout from the war and resulting sanctions to reduce Russia’s GDP by 12.5% by midyear (a decline worse than the 10% drop after the 1998 default). Our economists currently think that the euro area, highly dependent on Russia for oil and gas, will see GDP growth of roughly 2% in 2022, instead of the elevated 4.5% pace we had expected just six weeks ago. By contrast, they expect the U.S. economy to advance roughly 2.5% versus a previously estimated 3%. But I caution that these estimates are based upon a fairly static view of the war in Ukraine and the sanctions now in place.

Many more sanctions could be added — which could dramatically, and unpredictably, increase their effect. Along with the unpredictability of war itself and the uncertainty surrounding global commodity supply chains, this makes for a potentially explosive situation. I speak later about the precarious nature of the global energy supply, but for now, simply, that supply is easy to disrupt. (We should also keep in mind that, as a percentage of global GDP, oil is only about 40% of what it was in 1973 – but it is still essential and critical.)

The confluence of these factors may be unprecedented.

Each of these three factors mentioned above is unique in its own right: The dramatic stimulus-fueled recovery from the COVID-19 pandemic, the likely need for rapidly raising rates and the required reversal of QE, and the war in Ukraine and the sanctions on Russia. They present completely different circumstances than what we’ve experienced in the past – and their confluence may dramatically increase the risks ahead.

While it is possible, and hopeful, that all of these events will have peaceful resolutions, we should prepare for the potential negative outcomes. In the next section, I discuss immediate actions we should take to protect us from potential serious problems.

The war could affect geopolitics for decades.

Russian aggression is having another dramatic and important result: It is coalescing the democratic, Western world — across Europe and the North Atlantic Treaty Organization (NATO) countries to Australia, Japan and Korea. The United States and the West realize there is no replacement for strong allies and strong militaries.

The war and prior trade disputes with China also highlight the critical importance of economic relationships and trade, particularly trade that involves anything affecting national security. The outcome of these two issues will transcend Russia and likely will affect geopolitics for decades, potentially leading to both a realignment of alliances and a restructuring of global trade. How the West comports itself, and whether the West can maintain its unity, will likely determine the future global order and shape America’s (and its allies’) important relationship with China, which I talk more about later in this letter.

How are we managing our global bank in these difficult markets and complex times?

Our hearts go out to all of those affected by the war — JPMorgan Chase and its employees have already donated over $5 million to the Ukrainian humanitarian crisis, with more to come.

JPMorgan Chase has also played its part in the implementation of the Western world’s policies and sanctions regarding Russia. Of course, we are following both the letter of the law and the spirit of all the American and allied sanctions, working hand in hand with governments to implement complex policies and directives, and then some. Managing this has been an enormous undertaking. It is completely different from navigating a financial crisis or a severe recession. This entails sanctioning individuals, including their ownership of assets and companies; reducing exposures across multiple products and services; analyzing and stopping billions of dollars of payments as directed by governments; and many other actions.

We are not worried about our direct exposure to Russia, though we could still lose about $1 billion over time. But we are actively monitoring the impact of ongoing sanctions and Russia’s response, concerned as well about their secondary and collateral effects on so many companies and countries. We have been steadfast in our operating principles to be prepared for the unpredictable. Rest assured that our management teams, hundreds of us, globally, have been working around the clock to do the right thing.

The Extraordinary Need for Strong American Leadership

Even before the war in Ukraine jeopardized the world order, we were facing exceptional and enormous global challenges — nuclear proliferation (this is still the biggest risk to mankind, bar none, and made all the more stark by the war in Ukraine), threats to cybersecurity, terrorism, climate change, pressures on free and fair trade, and vast inequities in society. Critical to solving these problems is strong American leadership. American global leadership is the best course for the world and for America — and our leadership needs to articulate to its citizens why this is the case. The war in Ukraine reminds us that in a troubled world, national security always becomes the paramount concern. We should never again forget that this is true even in peaceful times – and we should never again be lulled into a false sense of security. Power abhors a vacuum, and it should be increasingly clear to all that without strong American leadership, chaos likely will prevail.

The world does not want an arrogant America telling everyone what to do but, instead, wants America working with allies, collaborating and compromising. Most of the world would applaud mature, respectful and civil leadership by America. We can organize military and economic frameworks that make the world safe and prosperous for democracy and freedom only if we work with our allies.

If Western allies across Europe and Asia realize there is power in strong partnership, it puts the Western world in a better position to address future challenges, including those posed by China’s growth. This is applicable to areas where we have common interests (e.g., anti-terrorism, nuclear proliferation, climate change), as well as to areas where we may not (e.g., economic and political competition).

It also is clear that trade and supply chains, where they affect matters of national security, need to be restructured. You simply cannot rely on countries with different strategic interests for critical goods and services. Such reorganization does not need to be a disaster or decoupling. With thoughtful analysis and execution, it should be rational and orderly. This is in everyone’s best interest.

While America has flaws, its essential strengths endure.

Many feel despondent about the “decline” of America. Our economy has had anemic growth for decades. COVID-19 and George Floyd’s murder cast a spotlight on what we already knew — that our lower-income citizens, often minorities, suffer more in our society, particularly during recessions and times of turmoil. Continuing income inequality may very well be causing growing partisanship, as some people believe the American dream is fraying and that our system is unfair, leaving many of our citizens behind.

In prior letters, I have detailed our poor management of basic policy in America and what the consequences have been from that dysfunction: ineffective education systems, soaring healthcare costs, excessive regulation and bureaucracy, the inability to plan and build infrastructure efficiently, inequitable taxes, a capricious and wasteful litigation system, frustrating immigration policies and reform, inefficient mortgage markets and housing policy, a partially untrained and unprepared labor force, excessive student debt, and the lack of proper federal government budgeting and spending, which lead to huge inefficiencies. Since I have covered these issues at length in the past, I will not elaborate on them here. I do, however, want to point out (and I find it disheartening) how readily we accept the failure, often with a chuckle, of our bureaucracy and policies.

Our country is not perfect, but our basic principles — i.e., the rule of law, individual liberties, freedom of speech and religion, and the concept of equal opportunity — are still exceptional ideals that most of the world wants yet often is not able to achieve. These principles still make America the partner of choice for many countries and the destination of choice for many individuals. Our American system gave us one of the world’s most prosperous and innovative economies. I do not like it when anyone disparages this wonderful country because of our flaws. Though our sins may be real, they are the sins of all countries. We can celebrate this country for having given so much to so many while acknowledging prior mistakes and fixing them. It is shocking to me how many people denigrate not just America but free enterprise and the essential role of business. If America could open its borders to all, I have little doubt that billions of people, if they could, would want to come here, and few would leave.

America has faced tough times before — the Civil War, World War I, the U.S. stock market crash of 1929 and the Great Depression that followed, World War II and 9/11, among others. As recently as the late 1960s and 1970s, we struggled with the loss of the Vietnam War, political and racial injustice, recessions and inflation. (Do you remember America’s obsession and fear about the emergence of Japan as an economic power in the 1980s?) In each case, however, America’s resiliency persevered and ultimately strengthened our position in the world. We hope this time is no different, but we should not be complacent as we do not have a divine right to success.

To maintain our competitiveness, our country must regain its competence — and our principles, including free enterprise, need to be nurtured.

America’s moral, economic and military might all derive from our principles and are also predicated on the strength and competence of the American system. We must acknowledge that nurturing and maintaining our enormously prosperous economy provides the foundation of that system. Ultimately, that economy is what pays for the best military the world has ever seen.

Over the past 20 years, our economy has grown, on average, at only 2%. American ingenuity, work ethic, technology and business capability were able to overcome some — but not all — of our mismanagement. We should not accept mediocrity; we no longer imagine what should be: Over the past decade, we should have grown at 3.5%.

Freedom and its brother, free enterprise, properly regulated are the answer — not unconstrained capitalism nor crony capitalism, where business uses government and regulations to maintain its position or strengthen its hand. All interest groups, business groups included, should applaud good public policy and not resist it for self-serving reasons.

Free enterprise celebrates, and is inseparable from, human freedom and creativity, which ultimately are the sources of all human progress. The secret sauce of free enterprise is not only the free movement of capital but also, more importantly, the value of knowledge and free people exercising their rights.

Nonetheless, many countries — inadvertently through decades of following bad policy or deliberately by restricting freedoms — damage the full benefit of free enterprise and often discourage savings, innovation, and the free movement of people and labor. We all believe in great social safety nets that reduce poverty, provide opportunity for good jobs and serve as an engine for economic growth. But freedom slowly disappears when a country’s government controls too much of its economy, and people in nearly every country, free or not, do not like constantly being told what to do. It is disingenuous when political leaders say that government “built the roads” and then use that statement as an argument to suppress free enterprise. The roads were built by the people and for the people so that all could travel and prosper.

What we really need are free enterprise, more civic-minded companies and citizens, and extraordinarily competent government and policies.

Government, with its unique powers, has an essential role in managing the economy — but it needs to be realistic about its limitations on what it can and cannot do.

We have fallen into the rut of false narratives, which distracts us from facing reality. We don’t define our problems properly. If you have the wrong diagnosis of a problem, you will certainly have the wrong solution. Even if you have the right diagnosis, you still may arrive at the wrong solution — but your odds are certainly much better. Our policies are often incomprehensible and uncoordinated, and our policy decisions frequently have no forethought and no identification of desired outcomes.

We sometimes blame inflation on corporate profits — for example, the cost of meat in the United States is high not because of the profits earned by the meat packing industry but because of high cattle and feed costs and disruptions in logistics. Similarly, energy costs are high not because of price gouging but because of the dramatic decline in investments in energy, which results in reduced supply when demand goes up. Regulation has dramatically impeded our ability to build good infrastructure in a timely manner — the cost of building a highway has more than tripled in 20 years purely because of expenses due to regulations.

Our politics are dysfunctional, which has prevented some of our best, brightest and most competent to want to work in government. While we have plenty of economists, academics and lifetime politicians in government, who I know are committed to doing their best, we need additional brainpower, capabilities and experience from leaders across all sectors of our society, including business. It is going to take extraordinary, broad-based leadership to solve our problems.

There are some things only the federal government can do — among them, protect national security, operate federal courts, act as a central bank, perform certain research and development (R&D), and execute some national infrastructure.

While government cannot create jobs outside of government itself, it can optimize the conditions under which jobs can be created. If it simply exhibits consistency and competence in the performance of its tasks, government will maximize investments and jobs. Conversely, government can destroy jobs and capital investment through bureaucracy, red tape and constant policy changes. Government cannot and will not be able to hold back technology, but it can foster an environment that promotes quick retraining of those who are replaced by technological advancements.

Our problems are neither Democratic nor Republican — nor are the solutions. Unfortunately, however, partisan politics are preventing collaborative policy from being designed and implemented, particularly at the federal level. We would do better if we listened to one another.

Democrats should acknowledge Republicans’ legitimate concerns that money sent to Washington often ends up in large wasteful programs, ultimately offering little value to local communities. Democrats could acknowledge that while we need good government, it is not the answer to everything. Democrats could also acknowledge that a healthy fear of a large central government is not irrational (like a leviathan).

Republicans need to acknowledge that America can and should afford to provide a proper safety net for our elderly, our sick and our poor, as well as help create an environment that generates more opportunities and more income for more Americans. Republicans could acknowledge that if the government can demonstrate that it is spending money wisely, we should spend more — think infrastructure and education funding. And that may very well mean higher taxes for the wealthy. Should that happen, the wealthy should keep in mind that if tax monies improve our society and our economy, then those same individuals will be, in effect, among the main beneficiaries.

Democrats and Republicans often seem to be ships passing in the night — with both parties talking at cross purposes even when they may share the same goals. Compromise is not incompatible with democracy — in fact, compromise is a core principle of democracy. Enacting major policies on a purely partisan basis (think healthcare and tax reform) virtually guarantees decades of fighting. It’s not unreasonable to assert that major policies should be bipartisan or not at all.

We must remember that the concepts of free enterprise, rugged individualism and entrepreneurship are not incompatible with meaningful safety nets and the desire to lift up our disadvantaged citizens. We can acknowledge the exceptional history of America and also acknowledge our flaws, which need redress.

We must confront the Russia challenge with bold solutions.

America must be ready for the possibility of an extended war in Ukraine with unpredictable outcomes. We should prepare for the worst and hope for the best. We must look at this as a wake-up call. We need to pursue short-term and long-term strategies with the goal of not only solving the current crisis but also maintaining the long-term unity of the newly strengthened democratic alliances. We need to make this a permanent, long-lasting stand for democratic ideals and against all forms of evil.

Our nation’s solutions need to be bold, brave and dynamic — and they have to be bipartisan — because we know only bipartisan solutions stand on firm ground. Bipartisanship could start with the appointment of Republicans to the cabinet. We need to think broadly because whatever we do will not only help determine the fate of the war in Ukraine but likely will determine the ability of the Western democratic world to address critical future challenges. We also need to ensure that the Western coalition remains economically competitive on the world stage. The better America performs as a country in dealing with Russia now, the easier it will be for us to engage with the rest of the world, including China, going forward.

In addition to being big, clear-eyed and realistic, our solutions should acknowledge that we are essentially, and unfortunately, reverting to some Cold War strategies. Here are some actions we should take immediately:

- Demonstrate leadership and commitment to a long-term military strategy by meaningfully increasing our military budget and troop deployment on NATO’s borders, as appropriate. To both sides, these steps make our resolve clear and reflect our recognition of the grave new geopolitical realities.

- Direct billions of dollars in aid to Ukraine, announced now, to support the country currently and to help rebuild in the future. We should also help the Europeans with the enormous migration issues they are facing. The United States could take the lead in humanitarian efforts and ask all nations, including China, to join us in this response.

- Turn up sanctions — there are many more that could be imposed — in whatever way national security experts recommend to maximize the right outcomes.

- We need a “Marshall Plan” to ensure energy security for us and our European allies. Our European allies, who are highly dependent on Russian energy, require our help. For such a plan to succeed, we need to secure proper energy supplies immediately for the next few years, which can be done while reducing CO2 emissions.

As we are seeing — and know from past experience — oil and gas supply can be easily disrupted, either physically or by additional sanctions, significantly impacting energy prices. National security demands energy security for ourselves and for our allies overseas. Fortunately, we do not need to change our long-term objectives on climate change and greenhouse gases, and we should remind ourselves that using gas to diminish coal consumption is an actionable way to reduce CO2 emissions expeditiously. While the United States is fairly energy independent, we need to increase our energy production and get more gas (in the form of liquefied natural gas) to Europe immediately. Our work with all of our allies should include urging them to both increase their production and deliver some of it to Europe. To do this, we also need immediate approval for additional oil leases and gas pipelines, as well as permits for green energy projects; i.e., solar and wind. We cannot accomplish our goals with misguided and counterproductive policies.

Strong, bold and comprehensive short-term and long-term policies, persistently and properly executed, will maximize the strength and the durable unity of the democratic world. Not only will this be very good for the Western world in general, but it will help frame our approach with China.

A strong America need not fear a rising China.

The most important relationship over the next 100 years will be the one between America (and its allies) and China. The stronger the allied nations, the better it is for America. But for America to get this essential relationship right, we need to have a clear-eyed view of our strategic economic and national security interests.

America is not operating from a position of weakness; indeed, our strengths are extraordinary. Conversely, over the next 40 years, China will have to grapple with some serious issues: For all of its strengths, China still needs more food, water and energy to support its population; pollution is rampant; corruption continues to be a problem; state-owned enterprises are often inefficient; corporate and government debt levels are growing rapidly; financial markets lack depth, transparency and adequate rule of law; income inequality remains highly prevalent; and its working age population has been declining since 2015. China will continue to face pressure from the United States and other Western governments over human rights, democracy and freedom in Hong Kong, and activity in the South China Sea and Taiwan.

Asia is a very tangled continent, geopolitically speaking. Many of China’s neighbors (Afghanistan, India, Indonesia, Japan, Korea, Pakistan, the Philippines, Russia and Vietnam) are large, complicated and not always friendly to China — in fact, China has had border skirmishes and wars with India, the Soviet Union and Vietnam since World War II. These neighbors do not all look at the rise of China as being completely beneficial. By comparison, America is at peace with its North American neighbors and is protected by the Atlantic and Pacific oceans.

America and China have large differences: ideological, democracy versus single-party rule, and market capitalism versus state-controlled capitalism. We also have common interests: halting nuclear proliferation, reducing terrorism, stopping climate change and promoting peaceful relationships. All countries, including China, want to lift up their people. Done right, we can establish and maintain a relationship with China that will allow both countries and the world to thrive.

Because we are dealing with a combination of circumstances that we have never confronted before — the rise of a country equal in size to us, unfair trade and bilateral investment rights, and state-sponsored subsidies and competition — we will need to respond in equally unprecedented ways.

We should stop complaining about unfair practices and just take appropriate action. Both countries can take unilateral actions as they see fit in the economic domain – and they already do – and that is okay.

To counter unfair competition on China’s part (i.e., subsidies and state-sponsored monopolies), we will need to develop thoughtful policies and strategies that work. We also need to develop “industrial policies” that help industries important to national security (for example, semiconductors, 5G, rare earths and others) succeed. I believe this could be done intelligently and not as “handouts” or subsidies that create excessive profits. This will also require increased government R&D focused on activities that business simply cannot do alone — advanced science, military technologies, among others.

Although there will be global trade restructuring, lots of global trade (and trade with China) will remain even after trade partnerships have been altered. Keep in mind, China’s trade with the West and the United States in 2021 totaled $3.6 trillion (exports and imports). By contrast, China’s total trade with Russia in 2021 totaled almost $150 billion. Clearly, these economic relationships are critical to China and the West – China also has a huge interest in making this work.

All of these policies must be done in conjunction with our allies or they will not be effective – because without a united front, unfair economic and trade practices will still be allowed to flourish. If it were up to me, I would rejoin the Trans-Pacific Partnership (TPP). We need to look at trade as only one part of strategic economic partnerships — and that’s exactly what TPP did. There is a lot at stake, but there is no reason why serious, comprehensive, honest negotiations can’t lead to good outcomes.

There are compelling reasons for global trade restructuring.

There is no question that supply chains need to be restructured for three different reasons:

- For any products or materials that are essential for national security (think rare earths, 5G and semiconductors), the U.S. supply chain must either be domestic or open only to completely friendly allies. We cannot and should not ever be reliant on processes that can and will be used against us, especially when we are most vulnerable.

- For similar national security reasons, activities (including investment activities) that help create a national security risk — i.e., sharing critical technology with potential adversaries — should be restricted.

- Companies will diversify their supply chains simply to be more resilient.

This restructuring will likely take place over time and does not need to be extraordinarily disruptive. There will be winners and losers — some of the main beneficiaries will be Brazil, Canada, Mexico and friendly Southeast Asian nations.

Along with reconfiguring our supply chains, we must create new trading systems with our allies. As mentioned above, my preference would be to rejoin the TPP — it is the best geostrategic and trade arrangement possible with allied nations.

We can have a path forward for U.S. policy: Agree on what we want, then execute.

We need more real leaders — people who know how to get things done, who are capable and who can educate and explain to all citizens what we need and why. We need a renaissance of the American dream and American “can-do” exceptionalism.

Our leaders need to agree on what we want and then execute to get it done. At a minimum, we should all agree that we want:

- The world’s most prosperous economy, which would also mean having the world’s reserve currency. The strength and the importance of the U.S. dollar are predicated on the strength and openness of the U.S. economy, the rule of law and the free movement of capital.

- Regulations and policies that foster growth and accomplish stated goals but don’t cripple business innovation and investment. Policies need to be consistent, reliable and constantly reviewed to reduce red tape and increase efficiency.

- A new strategic economic and competitive framework, devised in partnership with our allies (particularly as it relates to China), which includes trade and industrial policy, as previously discussed. This does need rebranding. Trade is only part of an economic relationship (there are investment rights, property rights, education, immigration rights and so on). We should always negotiate strategic economic agreements remembering that whether you emerge with a formal agreement or not, you likely have created a policy.

- A “Marshall Plan,” as previously mentioned, to ensure energy security for us and our European allies, requiring us to secure proper energy supplies immediately for the next few years (which can be done while reducing CO2 emissions and combatting climate change).

- The strongest military in the world — continually maintained, though used judiciously and in conjunction with our allies. The strength of the military needs to be matched by the strength of our diplomatic, development and intelligence agencies.

- A more equitable labor market that maximizes employment and values all jobs, effective and continuous job training for workers of all ages, and practices that better promote sharing the wealth — i.e., higher minimum wages, an increased Earned Income Tax Credit (EITC), broader healthcare coverage and other related policies.

- A strong America that respects all its citizens, helps the poor and disadvantaged, honors again the dignity of work, and demonstrates character and civility. And we all want well-functioning, healthy social safety nets.

The war in Ukraine and the growing competitiveness of China — including its growing military and strategic alliances across the globe — dictate that we move forward on our comprehensive needs. If we do not resolve our problems and restore effective long-term leadership, it is easy to envision darker days ahead in both the economic and geopolitical realms. But with great leadership, America, our allies and the rest of the world will enjoy a brighter future.

Learning from other countries’ successes — and failures

It is always instructive to look around the world at policies and countries that work — and policies and countries that don’t work. For example, you can find countries that have done a great job providing safety nets — without damaging labor — and building infrastructure efficiently without crippling regulations. A number of countries have succeeded in developing themselves, surprisingly often with minimal natural resources: Ireland, Israel, Singapore, South Korea and Sweden. Singapore has developed effective healthcare programs. Germany and Switzerland have created impressive work apprenticeship models, and Hong Kong has excelled at infrastructure. Another inspiring example is Ireland. After decades of sectarian strife and terrorism, Ireland is now a melting pot with a thriving economy due to good government policies.

Then there are the counterexamples, countries sometimes flush with natural resources — Argentina, Cuba and Venezuela. Rarely is the successful nation the socialist or autocratic one. And all of the negative cases are either socialist governments or governments hypothetically run in the name of the people. The successful nations, on the other hand, all are market-based economies of slightly different types with policies that grow their economy and share the nation’s wealth. Sweden is a good example of a country that many consider socialist, but it is far from it. By most measures, Sweden is actually more of a market-based economy than the United States, and it has enormous wealth and extremely strong social safety nets.

Competitive Threat Redux

The growing competition to banks from each other, shadow banks, fintechs and large technology companies is intensifying and clearly contributing to the diminishing role of banks and public companies in the United States and the global financial system. Before we give an update on the structural shifts taking place, it would be good to address the question: How did banks perform during the recent COVID-19 crisis?

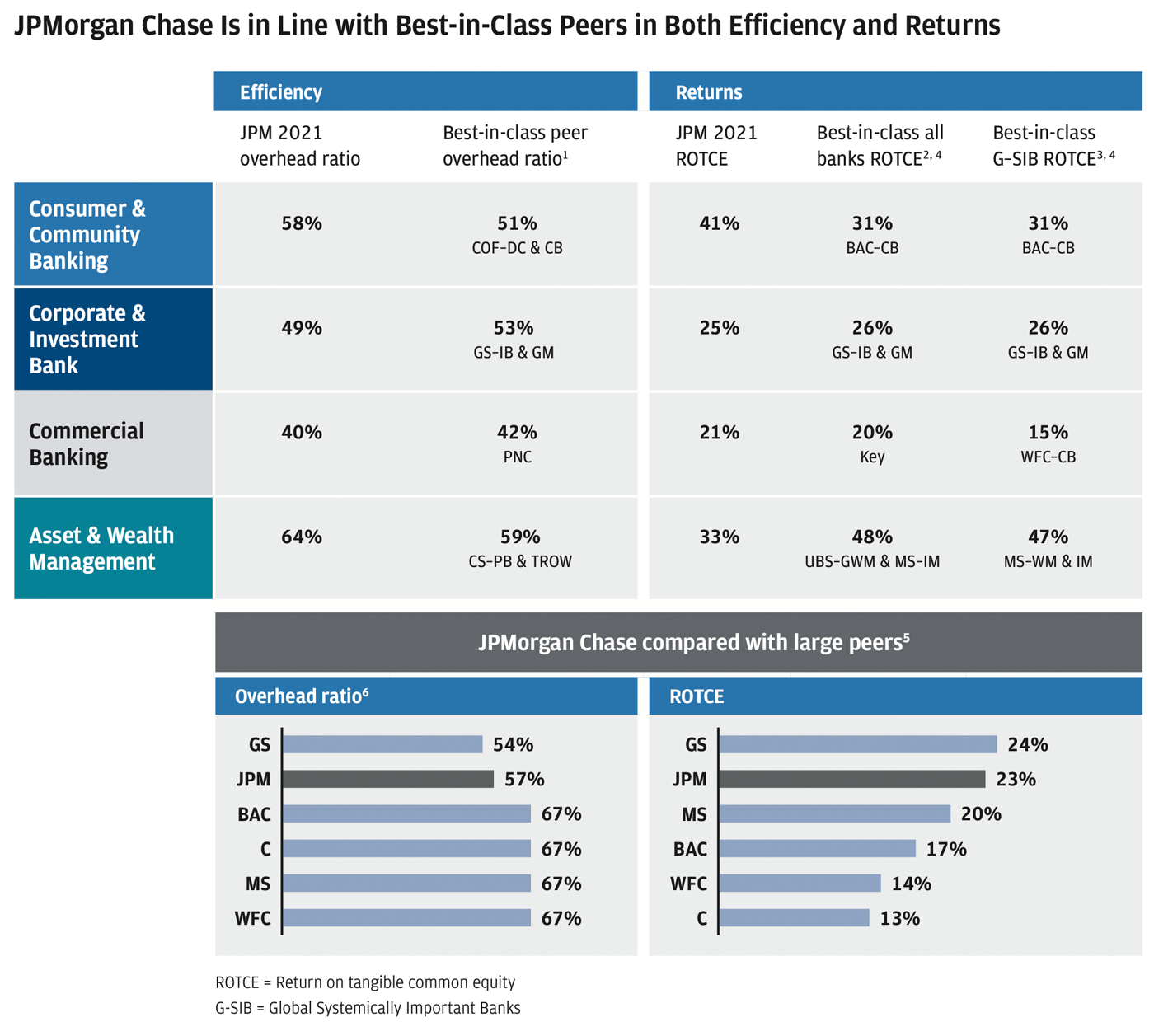

Banks performed magnificently during the COVID-19 crisis.

Within days of realizing COVID-19 was a pandemic that would virtually close large parts of the world’s economies, the U.S. government moved with unprecedented speed. Fortunately, most banks were part of the solution — unlike during the Great Recession when many banks were not. And fortunately, unlike during the Great Recession, the U.S. economy was actually in good shape going into the COVID-19 recession.

Yes, of course, it is true that large government actions dramatically helped individuals, companies (including banks) and the economy overall. But it is also true that banks performed magnificently during the COVID-19 crisis. They extended a huge amount of credit, waived fees and postponed debt repayment, and were at the forefront of delivering Paycheck Protection Program (PPP) loans to small businesses. And they did it the right way, protecting government money by trying to make legitimate loans to borrowers in need. By contrast, nonbanks were involved in instances of illegitimate PPP loans and Economic Injury Disaster Loan assistance, as well as stimulus money fraud, often at rates almost five times those of traditional banks. As for us:

- JPMorgan Chase was the #1 PPP lender — over the life of the program, we funded more than 400,000 loans totaling over $40 billion.

- Since March 13, 2020, we delayed payments due and refunded fees for more than 3.5 million customer accounts — refunding more than $250 million for nearly 2 million consumer deposit and lending accounts and offering delayed payments and forbearance on more than 2 million mortgage, auto and credit card accounts, representing approximately $90 billion in loans.

- In 2020, we raised capital and provided credit totaling $2.3 trillion for customers and businesses of all sizes, helping them meet payroll, avoid layoffs and fund operations during that first year of the pandemic crisis.

- In 2020, we committed $250 million in global business and philanthropic initiatives, with particular focus on the people and communities most vulnerable and hardest hit by the pandemic.

- In addition, JPMorgan Chase launched several ambitious flagship programs, including our $30 billion commitment to help close the racial wealth gap and drive economic inclusion, which is described in more detail within this letter.

While the U.S. government’s actions were a benefit to the whole economy, including the banking industry, banks were more than able to weather the terrible financial storm while setting aside extensive reserves for potential future loan losses. Importantly, during this time, the Fed conducted two additional, severely adverse Comprehensive Capital Analysis and Review stress tests, which projected bank results under extreme unemployment, GDP loss, market disruption and a smaller government stimulus. The results showed that banks could withstand these extreme conditions while continuing to finance the economy.

I also have very little doubt that if the severely adverse scenario played out, JPMorgan Chase would perform far better than the stress test projections. One supporting data point: From March 5, 2020 to March 20, 2020, when the stock market fell 24% and the bond index spread gapped from 191 to 446 prior to major Fed intervention, our actual trading revenue was higher than normal as we actively made markets for our clients. By contrast, the hypothetical stress test had us losing a huge amount of money in market-making, based on the way it is calculated.

While I understand why regulators stress test this way — they are essentially trying to ensure that banks survive the worst-case scenario — the methodology clearly does not result in an accurate forecast of how our company would perform under adverse circumstances.

Read footnoted information here

The role of banks in the global financial system is diminishing.

Banks have advantages and disadvantages. Some of the advantages, including economies of scale, profitability and brand, may only diminish slowly. Unfortunately, it also seems likely that some of the disadvantages, such as uneven or costly regulation, may not diminish at all. Other disadvantages, like legacy systems, will diminish over time.

Regulations have consequences, both intended and unintended — but many regulations are crafted with little regard for their interplay with other policies and their cumulative effect. As a result, regulations often are disconnected from their likely outcomes. This is particularly true when trying to determine what products and services will remain inside the regulatory system as opposed to those likely to move outside of it.

Keep in mind that markets, not regulators, set capital requirements. If regulators set capital standards that are too high for banks to hold loans, then the markets will drive those loans outside of the banking system. There are also non-capital regulatory standards that can force activities out of the regulatory system, such as excessive reporting and social requirements, among others.

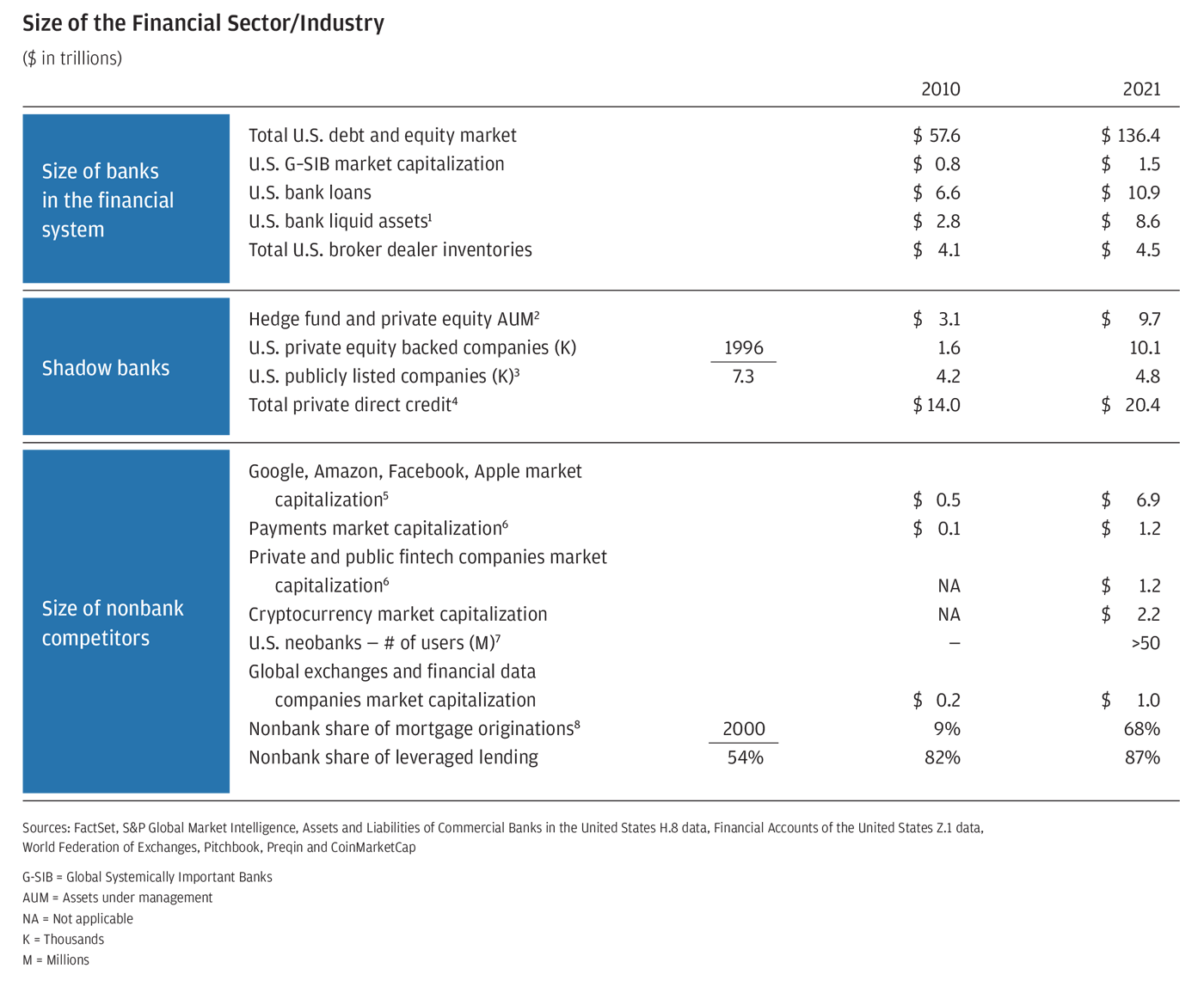

Banks around the world are already engaged in tough competition with each other. A quick review of the chart above shows the phenomenal size of nonbanks — from payments companies and fintechs to exchanges and Big Tech — that compete with traditional banks, but outside of the banking regulatory system, in providing certain financial services. And those don’t include many others, such as Schwab, Fidelity or Vanguard – which also provide banking-type services. The data also doesn’t show that last year alone, $130 billion was invested in fintech, allowing them to speed things up — and at scale.

The pace of change and the size of the competition are extraordinary, and activity is accelerating. Walmart, for good reason (over 200 million customers visit their stores each week) can use new digital technologies to efficiently bring banking-type services to their customers. Apple, already a strong presence in banking-type services with Apple Pay and the Apple Card, is actively extending services into other banking-type products, such as payment processing, credit risk assessment, person-to-person payment systems, merchant acquiring and buy-now-pay-later offers. The large tech companies, already 100% digital, have hundreds of millions of customers, enormous resources in data and proprietary systems — all of which give them an extraordinary competitive advantage.

Properly regulated banks are meant to protect and enhance the financial system. They are transparent with regulators, and they strive mightily to protect the system from terrorism financing and tax evasion as they implement know your customer (KYC) and anti-money laundering laws. They protect clients’ assets and clients’ money in movement. They also help customers — from protecting their data and minimizing fraud and cyber risk to providing financial education — and must abide by social requirements, such as the Community Reinvestment Act, which requires banks to extend their services into lower-income communities. Regulators need to figure out what they really want to achieve.

The chart above shows banks’ decreasing role in the global economy, but a few examples will put it in stark contrast.

- Banks’ size and market cap (U.S. global systemically important bank [G-SIB] market cap is $1.5 trillion) have dramatically diminished relative to their nonbank competitors.

- U.S. banks’ broker-dealer inventories have barely kept pace with the large increase in total markets. Banks’ dramatic decline in market-making ability relative to the size of the public markets is a factor in the periodic disruptions that occur in the public markets.

- U.S. banks’ loans in an 11-year period have only grown 65% and now represent only 8% of total U.S. debt and equity markets, down from 11% in 2010.

- Conversely, U.S. banks’ liquid assets are up more than 300% to $8.6 trillion, most of which is needed to meet liquidity requirements.

- Banks’ share of mortgage originations has gone from 91% to 32%.

- Banks’ share of the leveraged loan market has decreased over the last 20 years from 46% to 13%.

- Neobanks, now with over 50 million accounts, bypass the Durbin Amendment and so earn higher revenue per debit swipe — and they don’t have to abide by certain other regulatory or social requirements.

- Other companies providing banking-type services have hundreds of millions of accounts that hold consumer money, process payments, access bank accounts and extensively use customer data.

- A sizable and growing portion of equity trading has moved off transparent exchanges to nontraditional trading firms, causing a loss of access to on-exchange liquidity for many market participants.

I can go on and on, but suffice it to say, we must be prepared for this trend to continue.

It seems unlikely to me that all the banks, shadow banks and fintech companies will thrive as they strive to take share from each other over the next decade. I would expect to see many mergers among America’s 4,000+ banks — they need to do this, in some cases, to create more economies of scale to be able to compete. Other companies will try different strategies, including bank-fintech mergers or mergers just between fintechs. You should expect to see some winners and lots of casualties — it’s just not possible for everyone to perform well.

Possibly more important: The role of public companies in the global financial system is also diminishing.

In addition to banks’ shrinking global role, you can see that the number of public companies, which should have grown substantially over the past decade, is remarkably reduced. Instead, U.S. public companies peaked in 1996 at 7,300 and now total 4,800. Conversely, the number of private U.S. companies backed by private equity companies has grown from 1,600 to 10,100 — a remarkable increase.

This migration is worthy of serious study. The reasons are complex and may include public market factors, such as onerous reporting requirements, higher litigation expenses, costly regulations, cookie-cutter board governance, less compensation flexibility, heightened public scrutiny and the relentless pressure of quarterly earnings.

It’s incumbent upon us to figure out why so many companies and so much capital are being moved out of transparent public markets to less transparent private markets — and whether this is in the country’s long-term interest. We do need to ask some questions: Do we want public companies? Are we okay with more and more of our capital markets being private and, therefore, less regulated? If I were a shareholder of a company, I would ask myself, do I really think that all the rules we impose on public companies actually make them better? Finally, we need to consider, is it a good thing that many investors won’t have the opportunity to invest in these companies if and when they are private?

There are good and bad reasons why capital is going private. For example, private companies can raise money more easily now than in the past. Private companies’ boards and management teams can focus primarily on the business, and private investors can be more patient with capital — they are not necessarily worried about short-term results.

We need to study this public market diminishment thoughtfully and deeply — particularly since more regulation is coming that will affect this trend. This is a good time to think through and create the outcomes we want — and not just let multiple, often well-meaning but uncoordinated legal, regulatory and policy decisions take us where we do not want to go.

More regulation is coming — 10 years after the crisis, we are still rolling out Basel IV — and we need more thoughtful calibration of the rules.

Basel IV seems likely to increase capital requirements for banks on credit, loans, trading books and operational risk, some of which is unnecessary. These risks are real, but they need to be properly and rationally calculated. For example, operational risk is real; it exists in all enterprises and is usually handled in the ordinary course of business. If all large companies had to hold capital for operational risk, following the standard set for banks, trillions of dollars of additional capital would be permanently held in idle funds. The question for all capital requirements is: How much is enough?

If done properly, bank regulations could be recalibrated, adding virtually no additional risk, to make it easier for banks to make loans, intermediate markets and finance the economy. When it comes to political debate about banking regulations, there is little truth to the notion that regulations have been “loosened” – at least in the context of large banks.

We should keep in mind the enormous unintended consequences that could result from any policy (e.g., regulations) not being properly thought through. Policy with no forethought — designed without a comprehensive plan or instigated out of anger or false morality — can have bad outcomes. A few examples will suffice:

- The U.S. government management of student lending has been a disaster. In the 11 years since they’ve taken over student lending, they have extended an additional $1 trillion in loans. Prior to the pandemic, $300 billion of these loans were either severely delinquent or not being paid. We are not against student lending, but the disciplined use of capital should be applied here, too. I generally agree with the position that for loans that should not have been made and where the borrower reaped no benefit, there should be some forgiveness. However, many loans were properly made and brought the benefit that was expected. Government should reform its policies to stop making loans that should never be made.

- Fannie Mae and Freddie Mac contributed to the crisis in the mortgage market. In the mad rush to improve home ownership levels, these government-guaranteed institutions played a major part (along with many others engaged in the mortgage markets), over decades, in loosening mortgage underwriting standards. Ultimately, this proved catastrophic, leading to nearly $1 trillion in mortgage losses. Conversely, since then, mortgage regulations’ excessive tightening is not only pushing the mortgage market into the unregulated financial system but also making mortgages less available to mostly lower-income Americans.

How should we address our G-SIB conundrum?

The U.S. implementation of G-SIB requirements does not enable a level playing field — plain and simple. Not only have American rules made the G-SIB designation worse for American banks (if JPMorgan Chase could operate on the same basis as large European banks, our Tier 1 capital requirements would be reduced by $30 billion), but the rules have not been adjusted as the framework allows. G-SIB capital requirements were supposed to be modified to account for the increasing size of the global economy and the smaller size of banks in relation to that global economy — this simply has not happened. So JPMorgan Chase will be required to hold 2% more common equity Tier 1 capital as a consequence.

We have always said that the G-SIB calculation is nonsensical as it is not risk-based at all. It drives absurd behavior, such as favoring various acquisitions that may be imprudent but don’t require G-SIB capital or encouraging very risky loans that require no more G-SIB capital than risk-free loans. Being a large, diversified company, with strong revenue and profit streams, is normally a source of strength in troubled times, but this is a negative in regard to G-SIB capital. Even though American banks are performing well today, these extra capital requirements we are required to meet will have long-term negative consequences.

This extra capital is a drag on our return on equity (ROE), effectively reducing whatever our ROE would be by approximately 15% (hypothetically, our 17% target should be 20%). As a result, the dilemma is this: Do we restrict our growth and our ability to serve our clients in order to reduce our capital requirements over time and seek a higher ROE or do we invest our capital to grow with our clients (and in many cases remain competitive) and accept a permanently lower ROE?

Banks need to acknowledge the dramatically changing competitive landscape.

If banks want to compete in this new and increasingly competitive world, they need to acknowledge the truth of this new landscape and respond appropriately — sometimes it truly is change or die.

As they adopt new technologies like cloud, artificial intelligence (AI) and digital platforms, banks may have an advantage in being able to leverage their large customer base to offer increasingly comprehensive products and services, often at no additional cost. While many fintech companies specialize in one area, you already see many fintechs moving in this direction — trying to deepen and broaden their client relationships.

The chart below shows the extensive number of services we already offer to our customers — many of which, depending on the product and customer relationship, are at no additional cost.

We have always invested for the future, and that is even more true today than it has been in the past. But the principle is the same — constantly invest and innovate to ensure our future prosperity.

Investments and Acquisitions: Determining the Best Use of Capital and Assessing ROIs

We have always said that a steady and increasing dividend along with reinvestment in one’s own business — organically and inorganically, offensively and defensively – are the highest and best use of capital. Reinvestment would ordinarily come before stock buybacks unless the stock is extraordinarily cheap. And we generally only buy back stock when we don’t see a clear need for the capital over the next few years.

In fact, stock buybacks at our company will be lower in the next year or so because we may need to retain more capital due to required capital increases (which, by any real measure, we definitely do not need) and because we have made some good acquisitions that we believe will enhance the future of our company.

We try to be rigorous in how we invest for the future. Above all, we try to free up our capital and capabilities with the following in mind: 1) we reduce complexity in our company and simplify as much as possible; 2) we periodically assess and eliminate hobbies (which have a danger all their own); and 3) we assess investments and activities that seemed good when we started them but are not working out as planned. However, some things simply are complex (like airplanes, pharmaceuticals, technology and banking) but worthwhile — and in fact necessary to compete. We don’t let fear of that complexity stop us from investing.

Before we talk about different types of investments, we should recognize that our most important asset — far more important than capital — is the quality of our people.

We announced earlier in the year that our total expenses would increase by approximately $6 billion. Of that amount, $2.5 billion is mostly related to people, reflecting both inflationary and competitive labor market dynamics. (We have been quite adamant that we will do what is necessary to retain talent – we cannot be one of the best companies without having some of the best talent.) Included in this $2.5 billion are certain expenses (think travel and entertainment) as economies have reopened.

In this section of the letter, I am going to focus on investments — describing how and why we do them and offering a few examples. We have always believed that investing continuously and rigorously for the future is critical for our ongoing success. This year, we announced that the expenses related to investments would increase from $11.5 billion to $15 billion. I am going to try to describe the “incremental investments” of $3.5 billion, though I can’t review them all (and for competitive reasons I wouldn’t). But we hope a few examples will give you comfort in our decision-making process.

Some investments generate predictable returns.

Some investments have a fairly predictable time to cash flow positive and a good and predictable return on investment (ROI) however you measure it. These investments include branches and bankers, around the world, across all our businesses. They also include certain marketing expenses, which have a known and quantifiable return. This category combined will add $1 billion to our expenses in 2022.

Our shareholders should also know that when we make investments like these, we incorporate through-the-cycle thinking — we don’t only look at current margins and charge-offs but also evaluate what we expect them to be over the next several years.

Acquisitions should pay for themselves — and each one has its own logic.

Acquisitions generally extend products, add services or bring in technology that we would have had to otherwise build ourselves. These acquisitions are described in more detail in the letters from the other CEOs included in this report. Over the last 18 months, we spent nearly $5 billion on acquisitions, which will increase “incremental investment” expenses by approximately $700 million in 2022.

We expect most of these acquisitions to produce positive returns and strong earnings within a few years, fully justifying their cost. In a few cases, these acquisitions earn money — plus, we believe, help stave off erosion in other parts of our business. Importantly, on an ongoing basis, many of our acquisitions will be relatively capital-lite, meaning they can grow over time but require little additional regulatory capital.

We want to build upon our global footprint.

While we don’t disclose our investment here, our international consumer expansion is an investment of a different nature. We believe the digital world gives us an opportunity to build a consumer bank outside the United States that, over time, can become very competitive — an option that does not exist in the physical world. We start with several advantages that we believe will get stronger over time: a global brand, with long-term capital and staying power; a global Payments business; an international Private Bank; global Asset Management products; and best-in-class trading platforms. We have the talent and know-how to deliver these through cutting-edge technology, allowing us to harness the full range of these capabilities from all our businesses. We can apply what we have learned in our leading U.S. franchise and vice versa. We may be wrong on this one, but I like our hand.

We make extensive investments in technology for a broad range of reasons, from improving operations and security to enhancing our products and services.

Investments in technology and operations, as well as related products and services, are the most complicated category. Some of these investments simply must be done to sustain the company’s health. Investments in this bucket help keep the ship in tip-top shape and touch a broad range of workplace needs: regulatory requirements and necessary improvements for cybersecurity, as well as operational resiliency and security. Some things we have done with no direct revenue benefit, rather simply to maintain our competitive position. I call these table stakes — think of digital account opening for consumer and small business accounts. Other investments are specific improvements to products and services, often with identifiable benefits. Finally, there are specific investments in this category that are more like forward-looking R&D, as described in the examples that follow.

Combined, this category will add a little bit less than $2 billion to our “incremental investment” expenses in 2022 (the actual expense lines could be for people, hardware or software, or purchased services). Almost all of the $2 billion in expenses are analyzed and studied for their ROI or other significant benefits.

Sometimes people refer to some of these expenses as modernizing or adopting new technologies. I prefer not to talk about it that way because, effectively, we have been modernizing my entire life. Also, the term implies that once you get to a modern platform, these expenses should dramatically decrease — which is rarely the case. In fact, when we analyze these expenses, we incorporate not only the cost to build the product or service but also the cost to maintain it going forward. Furthermore, once you have built the new platforms, they generally create a whole new set of investment opportunities to be analyzed. Technology always drives change, but now the waves of technological innovation come in faster and faster. The science behind them is also increasingly complex as technology (including AI) is “embedded” in more products. In today’s world, I cannot overemphasize the importance of implementing new technology.

We hope a few examples will explain how these expenses are managed. To do so, we are going to talk about two different types of investments that are clearly related: infrastructure and software.

First, on the path to new and modern infrastructure, cloud-based systems, whether private or public, will ultimately be faster, cheaper, more flexible and also AI-enabled — all extremely valuable features. A few other additional details: