Dear Fellow Shareholders,

2020 was an extraordinary year by any measure. It was a year of a global pandemic, a global recession, unprecedented government actions, turbulent elections, and deeply felt social and racial injustice. It was a year in which each of us faced difficult personal challenges, and a staggering number of us lost loved ones. It was also a year when those among us with less were disproportionately hurt by joblessness and poverty. And it was a time when companies discovered what they really were and, sometimes, what they might become.

Watching events unfold throughout the year, we were keenly focused on what we, as a company, could do to serve. As I begin this annual letter to shareholders, I am proud of what our company and our tens of thousands of employees around the world achieved, collectively and individually. As you know, we have long championed the essential role of banking in a community — its potential for bringing people together, for enabling companies and individuals to reach for their dreams, and for being a source of strength in difficult times. Those opportunities were powerfully presented to us this year, and I am proud of how we stepped up. I discuss these themes later in this letter.

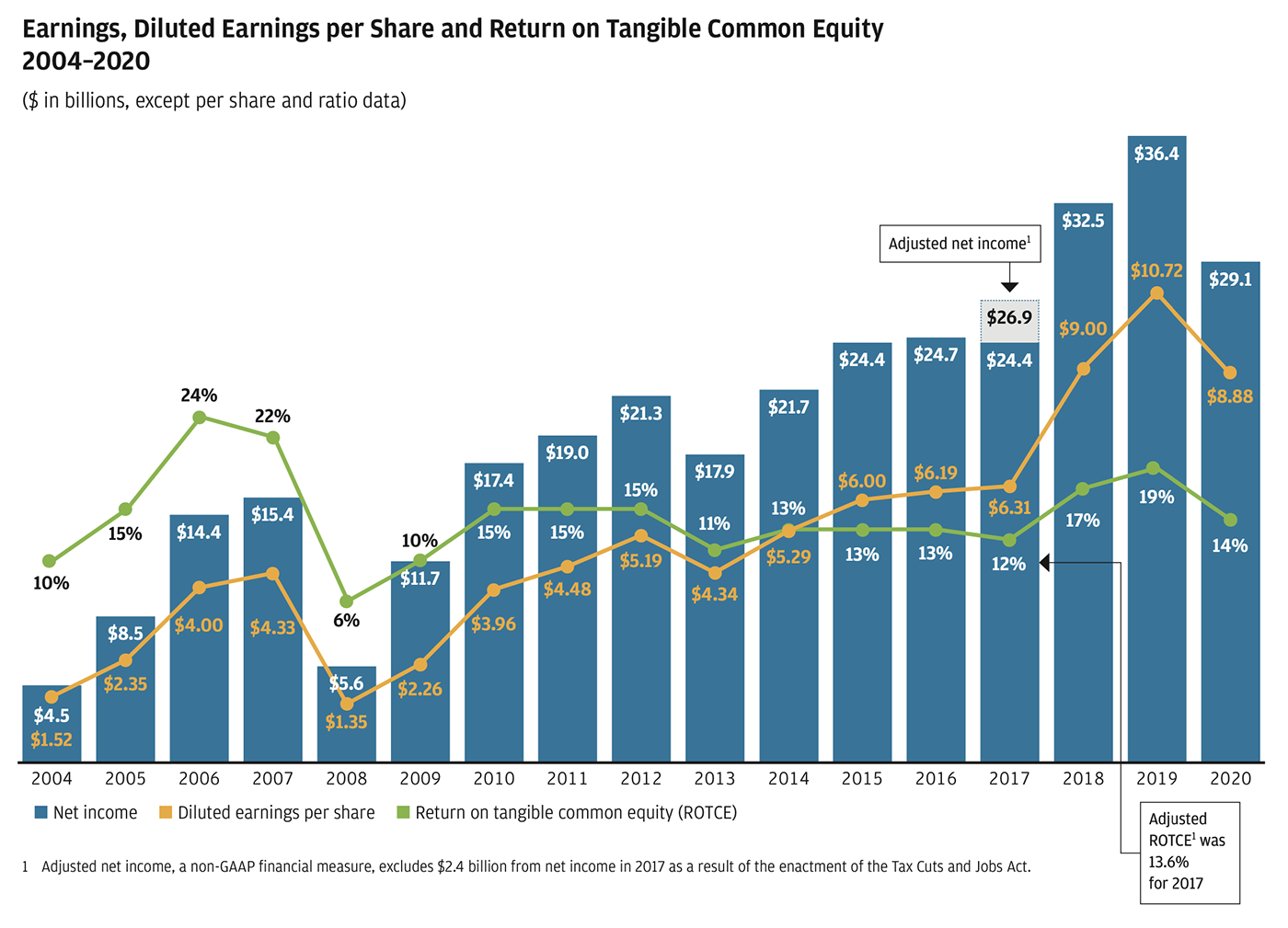

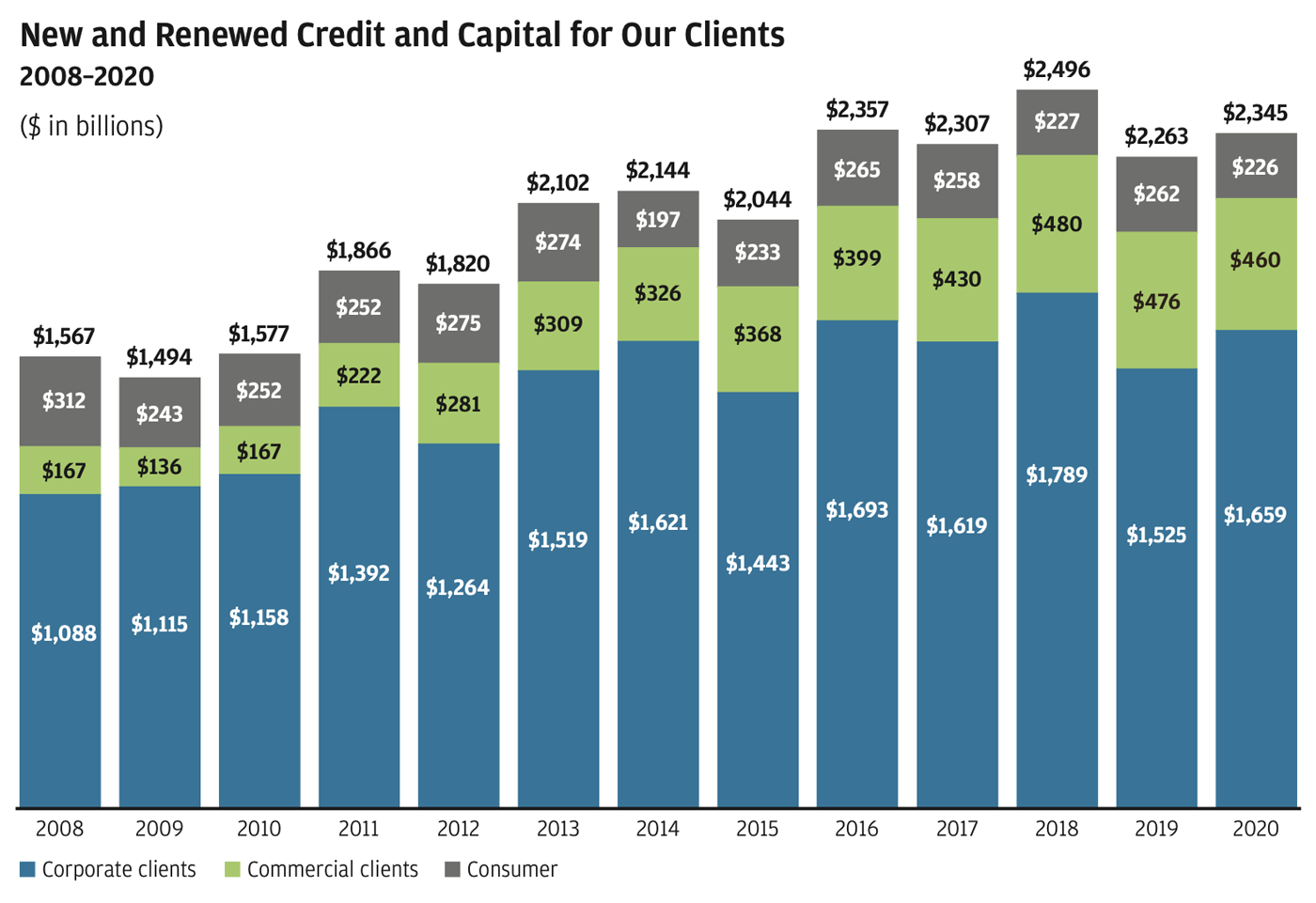

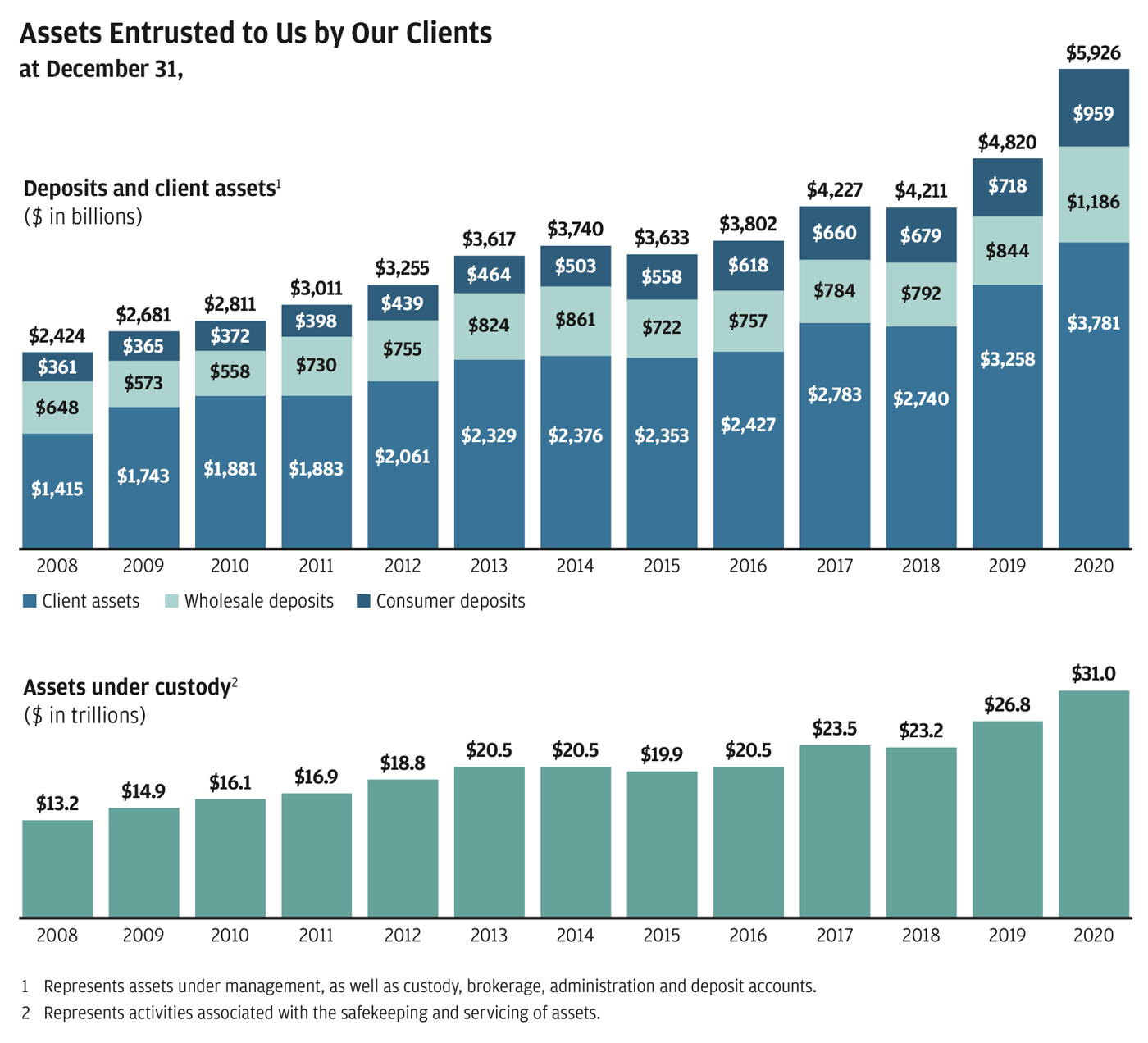

As I look back on the last year and the last two decades — starting from my time as CEO of Bank One in 2000 — it is remarkable how much we persevered and have accomplished, not only in terms of financial performance but also in our steadfast dedication to help clients, communities and countries throughout the world. 2020 was another strong year for JPMorgan Chase, with the firm generating record revenue, as well as numerous other records in each of our lines of business. We earned $29.1 billion in net income on revenue of $122.9 billion versus $36.4 billion on revenue of $118.5 billion in 2019, reflecting strong underlying performance across our businesses offset by additional reserves under new accounting rules. We generally grew market share across our businesses and continued to make significant investments in products, people and technology, all while maintaining credit discipline and a fortress balance sheet. In total, we extended credit and raised $2.3 trillion in capital for businesses, institutional clients and U.S. customers.

JPMorgan Chase stock is owned by large institutions, pension plans, mutual funds and directly by individual investors. However, it is important to remember that in almost all cases, the ultimate beneficiaries are the individuals in our communities. More than 100 million people in the United States own stock, and a large percentage of these individuals, in one way or another, own JPMorgan Chase stock. Many of these people are veterans, teachers, police officers, firefighters, healthcare workers, retirees or those saving for a home, school or retirement. Your management team goes to work every day recognizing the enormous responsibility that we have to perform for our shareholders.

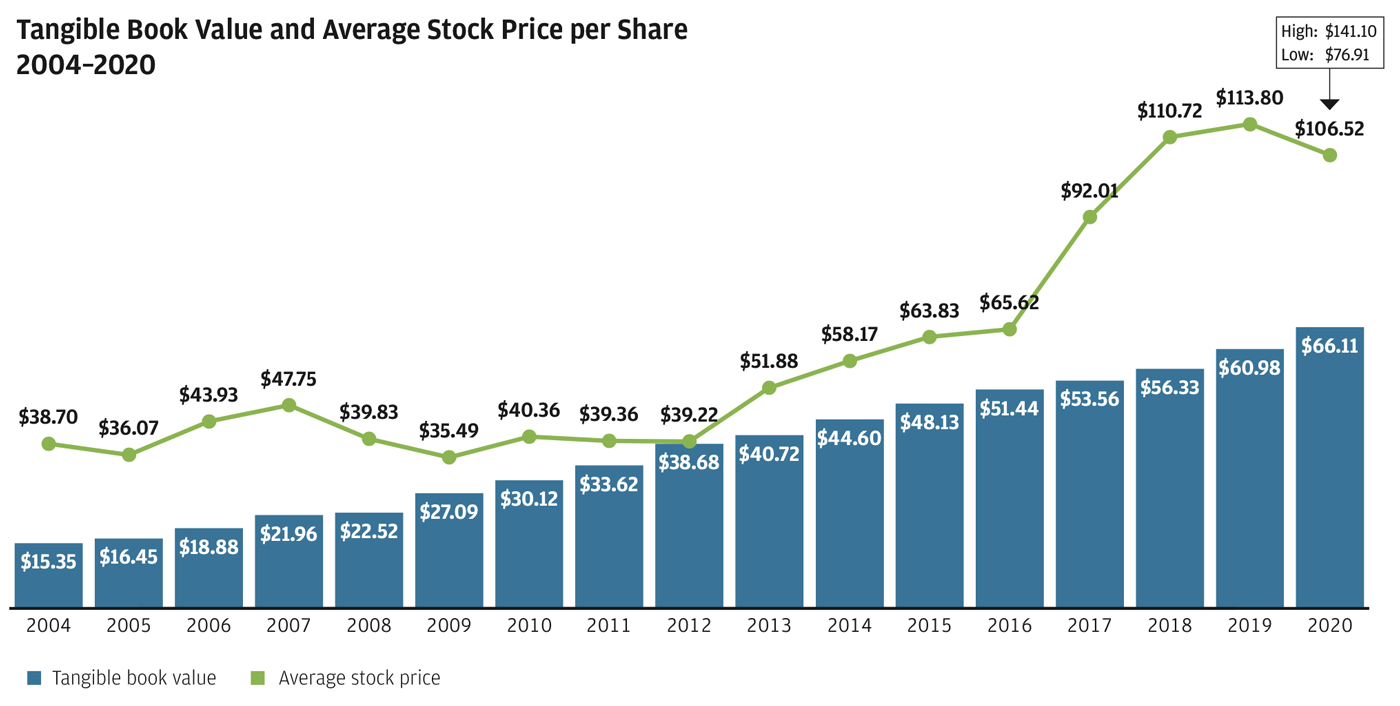

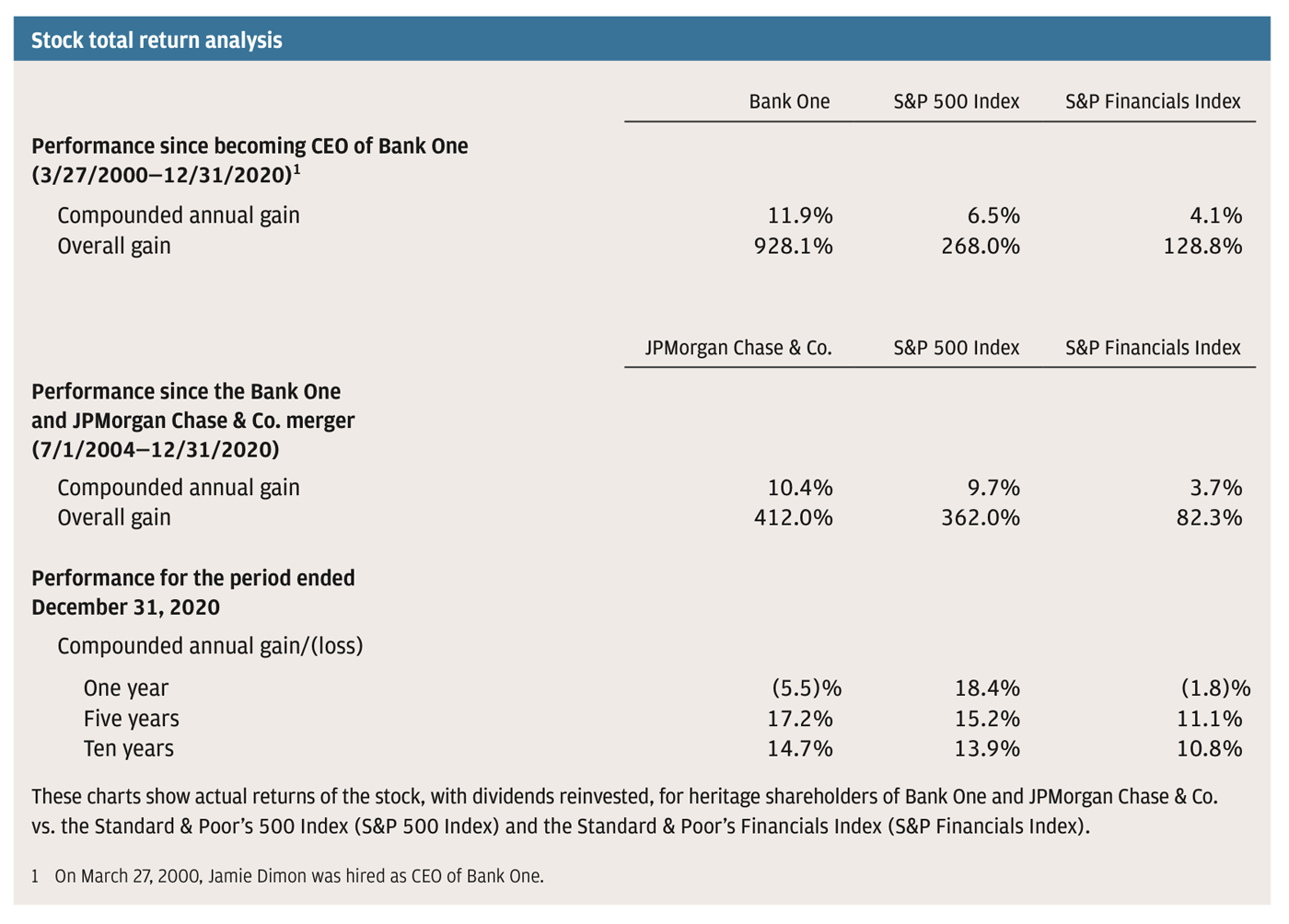

While we don’t run the company worrying about the stock price in the short run, in the long run our stock price is a measure of the progress we have made over the years. This progress is a function of continual investments in our people, systems and products, in good and bad times, to build our capabilities. Whether looking back over five years, 10 years or since the JPMorgan Chase/Bank One merger (approximately 15 years ago), these investments mean our stock has significantly outperformed the Standard & Poor’s 500 Index and the Standard & Poor’s Financials Index. These important investments will also drive our company’s future prospects and position it to grow and prosper for decades.

We have consistently described to you, our shareholders, the basic principles and strategies we use to build this company — from maintaining a fortress balance sheet, constantly investing, nurturing talent, fully satisfying regulators, and continually improving risk, governance and controls to serving customers and clients while lifting up communities worldwide.

Adhering to these principles allows us to drive good organic growth and properly manage our capital (including dividends and stock buybacks), which we have consistently demonstrated over the past decades. All of this is shown in the charts in this introduction. In addition, we urge you to read the CEO letters in this Annual Report, which will give you a lot more specific detail about our businesses and what our plans are for the future.

If you look deeper, you will find that our success and accomplishments are founded on our commitment to our shareholders. Shareholder value can be built only if you maintain a healthy and vibrant company, which means doing a good job taking care of your customers, employees and communities. Conversely, how can you have a healthy company if you neglect any of these stakeholders? As we have learned in 2020, there are myriad ways an institution can demonstrate its compassion for its employees and its communities while still upholding shareholder value.

Ultimately, the basis of our success is our people. They are the ones who serve our customers and communities, build the technology, make the strategic decisions, manage the risks, determine our investments and drive innovation. Whatever your view is of the world’s complexity and the risks and opportunities ahead, having a great team of people — with guts and brains and enormous capabilities who can navigate personally challenging circumstances while dedicating themselves to professional excellence — is what ensures our prosperity, now and in the future.

Read footnoted information here

Read footnoted information here

Within this letter, I discuss the following:

- The Corporate Citizen: The Purpose of a Corporation

- Businesses must earn the trust of their customers and communities by acting ethically and morally.

- Being a responsible community citizen locally is critical, and it is easy to understand why.

- Being a responsible community citizen nationally, or globally, is more critical and more complex.

- Lessons from Leadership

- Enforce a good decision-making process.

- Examine raw data and focus on real numbers.

- Understand when analysis is necessary and when it impedes change.

- Before conducting an important analysis, assess all factors involved.

- Always deal with reality.

- Remain open to learning how to become a better leader.

- Banks’ Enormous Competitive Threats — from Virtually Every Angle.

- Banks are playing an increasingly smaller role in the financial system.

- The growth in shadow and fintech banking calls for level playing field regulation.

- AI, the cloud and digital are transforming how we do business.

- Fintech and Big Tech are here … big time!

- JPMorgan Chase is aggressively adapting to new challenges.

- Specific Issues Facing Our Company

- Cyber risk remains a significant threat.

- Brexit was finally accomplished — but uncertainties linger.

- New accounting requirements affect reserve reporting but not how we run our business.

- While we disbanded Haven, we will continue to build on what we learned.

- COVID-19 and the Economy

- Bold action by the Fed and the U.S. government effectively reversed financial panic.

- Banks entered this recent crisis in great shape and were part of the solution coming out.

- The confusing interplay of monetary, fiscal and regulatory policy continues through recessions.

- The regulatory system needs to keep up with the changing world — and finish Dodd-Frank to get it right.

- The pandemic accelerated remote working capabilities, which will likely carry forward.

- Public Policy. American Exceptionalism, Competitiveness and Leadership: Challenged by China, COVID-19 and Our Own Competence

- Laying out the problems is painful.

- Why did — and didn’t — these failures happen?

- We need a comprehensive, multi-year national Marshall Plan, and we must strive for healthy growth.

- We need to take specific action steps.

- America’s global role and engagement are indispensable to the health and well-being of America.

I. The Corporate Citizen: The Purpose of a Corporation

We need to build and maintain a healthy and vibrant company, over the long run, to be able to deal with the uncertainties of life, to invest, to innovate and to grow. To be healthy and vibrant, a company must do many things well: It must do a great job for customers; attract, develop and retain talented employees; and serve its communities.

It is vital that we do all of these things, as the failure to perform any one of them with excellence could lead to the failure of all. Over the years, we have extensively described the efforts we make to take care of our customers and our employees. The purpose of this section is to describe our corporate responsibility efforts in more detail and explain their importance.

To be healthy and vibrant – and to create long-term shareholder value – a company must be financially successful over the long run.

The problem with the American public’s impression of “shareholder value” is that too many people interpret it to mean short-term, rapacious profit taking – which, ironically, is the last thing that leads to building real, long-term shareholder value. And when they hear the word “fiduciary,” they think we are standing behind our lawyers.

Obviously, companies have fiduciary responsibilities. However, legal and fiduciary language does not represent how most CEOs and boards actually run their companies. We should not be buttonholed by the debate about whether there are “fiduciary” reasons to think of “shareholder value” narrowly and to the exclusion of those who work at the company, our clients and communities. When most CEOs and board members wake up each morning, they worry about all of the things that they need to do right to build a successful company. A company is like a team. We must do many things well to succeed, and, ultimately, that leads to creating shareholder value.

Business Roundtable’s Statement on the Purpose of a Corporation

In August 2019, Business Roundtable released the below Statement on the Purpose of a Corporation, signed by 181 CEOs, including Jamie Dimon, then chair of the association. This statement repositioned the definition of corporate success as serving shareholders principally to endorsing a modern standard of corporate responsibility: to serve all stakeholders — customers, employees, suppliers, communities and shareholders.

Americans deserve an economy that allows each person to succeed through hard work and creativity and to lead a life of meaning and dignity. We believe the free-market system is the best means of generating good jobs, a strong and sustainable economy, innovation, a healthy environment and economic opportunity for all.

Businesses play a vital role in the economy by creating jobs, fostering innovation and providing essential goods and services. Businesses make and sell consumer products; manufacture equipment and vehicles; support the national defense; grow and produce food; provide health care; generate and deliver energy; and offer financial, communications and other services that underpin economic growth.

While each of our individual companies serves its own corporate purpose, we share a fundamental commitment to all of our stakeholders. We commit to:

- Delivering value to our customers. We will further the tradition of American companies leading the way in meeting or exceeding customer expectations.

- Investing in our employees. This starts with compensating them fairly and providing important benefits. It also includes supporting them through training and education that help develop new skills for a rapidly changing world. We foster diversity and inclusion, dignity and respect.

- Dealing fairly and ethically with our suppliers. We are dedicated to serving as good partners to the other companies, large and small, that help us meet our missions.

- Supporting the communities in which we work. We respect the people in our communities and protect the environment by embracing sustainable practices across our businesses.

- Generating long-term value for shareholders, who provide the capital that allows companies to invest, grow and innovate. We are committed to transparency and effective engagement with shareholders.

Each of our stakeholders is essential. We commit to deliver value to all of them, for the future success of our companies, our communities and our country.

Released: August 19, 2019

1. Businesses must earn the trust of their customers and communities by acting ethically and morally.

To a good company, its reputation is everything. That reputation is earned day in and day out with every interaction with customers and communities. This is not to say that companies (and people) do not make mistakes – of course they do. Often a reputation is earned by how you deal with those mistakes.

While all businesses are different, there are some fundamentals: good products, fair and transparent pricing, thoughtful and responsive service, and continuous innovation. Great companies constantly set high standards, acknowledge their mistakes and properly discipline or dismiss bad actors.

Great companies are strict about having fair dealings with their customers. I have always loved that Home Depot’s company policy is not to raise lumber prices in the immediate aftermath of a hurricane, regardless of whether it can. (I want to remind readers that banks essentially did not raise the price of credit when they renewed loans during the financial crisis.) Pricing to customers should be what’s fair – not what a company can get away with.

Banks, in particular, have to be rigorous about standards. Unlike many companies that will simply sell you a product if you can pay for it, banks must necessarily turn customers down or enforce rules that a customer may not like (for example, covenants). This makes open and transparent dealings even more important. When I hear examples of people doing something that is wrong because they could be paid more, it makes my blood boil – and I don’t want them working here. And I can’t believe it when I hear about a company, or a hedge fund, causing loans and a company to default so they can trigger credit default swap hedges – it’s completely unethical.

We must always strive, particularly in tough times, to earn the trust of our customers and communities.

2. Being a responsible community citizen locally is critical, and it is easy to understand why.

If you live in a small town and run a corner bakery, it is very easy to understand the value of being a responsible community citizen. Most businesses on “Main Street” keep the sidewalk in front of their store clean so people don’t slip and fall. They often participate in the community by supporting local sports teams or religious institutions. A bakery or a restaurant will often donate surplus food at the end of the day to a local homeless shelter. Most businesses understand that everyone doing their part to make the community a better place is both the moral thing to do and a driver of better commercial outcomes for the town.

When JPMorgan Chase enters a community, we take great pride in being a responsible citizen at the local level – just like the local bakery. We lend to and support local businesses. We help customers with banking, lending and saving. And our local corporate responsibility efforts and philanthropic programs (examples of which are described in the following features in this section) help make these communities stronger.

3. Being a responsible community citizen nationally, or globally, is more critical and more complex.

Most people consider corporate responsibility to be merely enhanced philanthropy. This is understandable. But it is far harder to understand what being a responsible community citizen means in terms of macro corporate responsibility. While we are devoted to philanthropy – we spend $330 million a year on these efforts – corporate responsibility is far more than that.

JPMorgan Chase takes an active role in large-scale public policy issues. We are fully engaged in trying to solve some of the world’s biggest issues – climate change, poverty, economic development and racial inequality – and the accompanying features that follow describe the extensive efforts we are making. With well-designed policies, we think these problems can all be solved. In the last section of this letter, I detail certain policy issues, which – if forcefully and effectively addressed – would be great for America and the world at large. We engage at this level because companies (like ours) have an extraordinary capability to help. We help not just with funding but with developing strong public policy, which can have a greater impact on society than the collective effect of companies that are responsible community citizens locally. This year, for example, our PolicyCenter published research based on the actual experiences of our customers and communities, showing how new policies could drive a more inclusive economic recovery and help small businesses. JPMorgan Chase has always recognized that long-term business success depends on community success, and that is one of the reasons for our enduring achievement. When everyone has a fair shot at participating – and sharing – in the rewards of growth, the economy will be stronger, and our society will be better.

We also believe that businesses’ extraordinary capabilities are even more powerful when put to use in collaboration with governments’ capabilities, particularly when seeking to solve our biggest economic and societal ills at the local level. As Washington, D.C., and central governments around the world struggle with partisan gridlock and an inability to get big things done, local communities are coming up with some of the best ideas to make civic society work for more people. Mayors, governors, educators, major employers, entrepreneurs, community leaders and nonprofits are making serious progress developing innovative approaches that address our greatest challenges, but their work often flies under the radar. We must elevate these thoughtful ideas and find ways to share them with others facing similar situations, enabling more communities to benefit from proven, localized solutions. After businesses have had success with some of these efforts locally, they can be adopted across the country and, in fact, around the world.

Our effort is substantial and permanent and has support throughout the company.

Importantly, these civic efforts are supported by senior leadership and are managed by some of our best people (these initiatives are not an afterthought and are sustainable). For our part, we are making significant, long-term, data-driven business and philanthropic investments. And while we try to be creative, we analyze everything, including philanthropy, based on measurable results.

Executing Our Corporate Purpose

We go to great lengths to be there for our clients, customers, employees and communities. Moreover, this unwavering commitment has been a hallmark of our company since its founding. During this time of corporate self-reflection, it’s important to understand and reaffirm the magnitude of our contributions.

Helping Clients and Customers in 2020

- We extended credit and raised capital totaling $2.3 trillion for consumers and clients of all sizes around the world, including some of the industries and communities most affected by the pandemic’s economic fallout. This includes critical financing for companies such as Boeing and its 145,000 employees. J.P. Morgan helped them raise $25 billion to help fund their ongoing operations as the pandemic led to less air travel.

- We provided consumers with $226 billion in credit to help them afford some of their most important purchases, including new homes and vehicles. This included more than $32 billion to help customers in underserved communities purchase a new home.

- We raised $1.1 trillion in capital for corporations and non-U.S. government entities and offered $865 billion in credit for corporations. For example, we helped Meals on Wheels build a new 36,000-square-foot commercial kitchen and food production facility to help maintain good nutritional health of older adults with limited financial resources.

- We raised $103 billion in credit and capital for nonprofit and U.S. government entities, including states, cities, hospitals and universities. This included funding for NewYork-Presbyterian Health System – which saw a significant increase in patients as a result of COVID-19 – to help them acquire vital medical supplies and equipment and to bring on additional staff.

- We committed more than $45 billion in lending and investments to support community development, affordable housing and small business growth in underserved communities across the United States. This included Eden Housing, a nonprofit that provides low-income residents with safe, modern and affordable housing in California’s Bay Area.

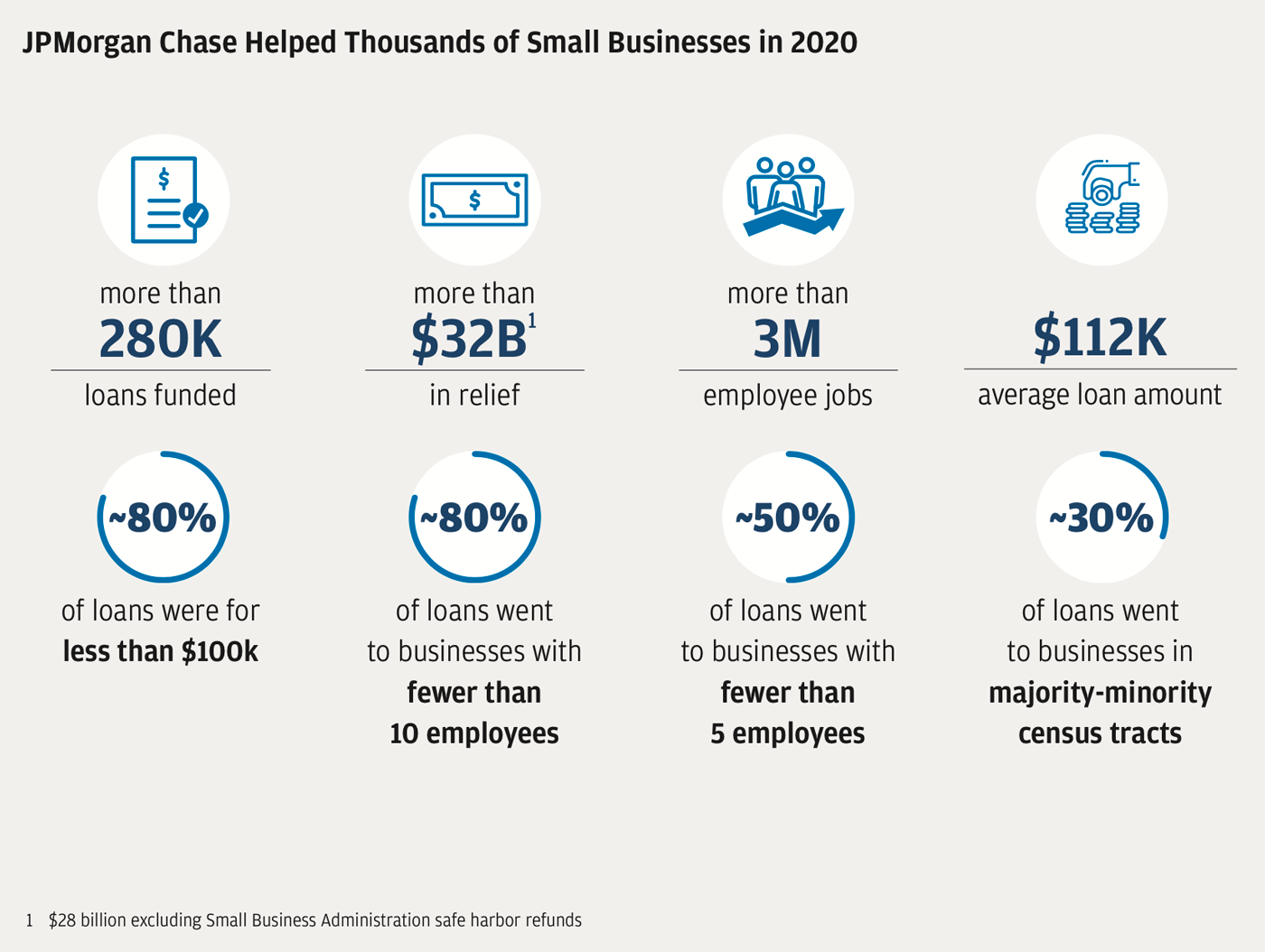

- We provided more than $18 billion in credit to small businesses around the country, as well as more than $32 billion in funding ($28 billion excluding Small Business Administration (SBA) safe harbor refunds) under the SBA’s Paycheck Protection Program (PPP). For example, we helped Kids Klub Child Development Centers — which offer preschool, daycare and after-school programming — revamp their centers to enable care for essential workers’ children.

- We provided critical development financing and attracted additional investment, such as funding through our new development finance institution (DFI) to support sustainable development. In 2020, the DFI mobilized $140 billion toward these goals — helping, for example, with Uzbekistan’s first local currency issuance in international markets to finance the country’s health, education and transport sectors and with the Republic of Georgia’s debut green bond to support that country’s access to water, power and sanitation.

- We raised $12 billion in capital and credit to help finance infrastructure projects across the United States. This included $1.3 billion in credit assistance to New York City’s Metropolitan Transportation Authority to help deal with the serious impacts of COVID-19 on the city’s transportation system and $800 million in capital for Michigan’s Department of Transportation to help rebuild the state’s roads and bridges.

- We designed branches, products, services and digital solutions to help clients and customers better manage their financial daily lives, with particular focus on underserved communities and families. Examples include low-cost, low-fee accounts, such as Chase Secure BankingSM, and financial tools, such as Chase Credit Journey and Chase Autosave. In 2020, we continued to open new branches in new markets across the United States with 30% opening in low- to moderate-income communities by 2023.

Helping Communities

- We have supported and continue to support a range of community initiatives — from assisting underserved small businesses outside of Paris to facilitating skills training for high-growth jobs in India to helping residents of Harlem increase savings and reduce debt. In 2020, we provided more than $500 million in low-cost loans, equity and philanthropic grants to address immediate needs brought on by the COVID-19 crisis, drive an inclusive recovery and advance racial equity. These efforts will help 1.3 million individuals receive financial coaching, enable 172,000 people to enroll in jobs and skills training programs, assist 64,000 underserved small businesses and create or preserve 43,000 affordable housing units.

- We have committed employee time and talent to tackling communities’ greatest challenges. In 2020, employees participated in nearly 50 Service Corps programs to help local nonprofits; mentored hundreds of Black and Latinx young men as part of The Fellowship Initiative; and supported local organizations focused on racial equity.

- We are dedicated to addressing climate change and sustainability around the world. In 2020, the firm committed to finance and facilitate $200 billion to drive action on climate change and advance sustainable development, including renewable energy, cleaner water and waste management; improve access to housing, education and healthcare; and promote infrastructure, innovation and growth around the globe.

Supporting Employees

- We have taken extensive steps to support our employees, who are our greatest strength. We offer 300 accredited skills and education programs and have helped 15,000 employees (to date) assess their skills, which may lead to opportunities for career mobility at the firm. And we have been increasing wages for thousands of employees, including branch and customer service employees, to between $16 and $20 an hour, depending on where they work in the United States, while providing an annual benefits package worth about $13,000.

- As part of our strategy to diversify our talent pipeline, we have implemented a range of changes to expand opportunities for individuals with a criminal background. In 2020, we hired approximately 2,100 people with a criminal background – roughly 10% of our new hires in the United States. And through the JPMorgan Chase PolicyCenter, we are advancing federal and state policies that help qualified workers with an arrest or conviction record compete for employment in federal agencies and with federal contractors. We are reforming Federal Deposit Insurance Corporation (FDIC) hiring rules and setting up automatic record clearing for eligible offenses to help individuals move on from their record. We also supported a measure signed into federal law in 2020 restoring access to Pell Grants for incarcerated individuals, which allows them to pursue postsecondary education in prison and increase employment opportunities after their release.

Our $30 Billion Path Forward Commitment

JPMorgan Chase introduced The Path Forward in October 2020, committing $30 billion over the next five years to address the key drivers of the racial wealth divide, reduce systemic racism against Black and Latinx people, and support employees. The firm has made tangible progress to date.

Promote and expand affordable housing and homeownership for underserved communities

- Helping Black and Latinx families buy homes and refinance loans: Our Home Lending business has committed to helping an additional 40,000 Black and Latinx families buy a home over the next five years, with the firm dedicating $8 billion in mortgages for this purpose. The firm is committing up to $4 billion in refinancing loans to help an additional 20,000 Black and Latinx households achieve lower mortgage payments. In addition, the firm is working to improve key home lending products and offerings: A $5,000 grant, for example, will help cover closing costs and down payments for people buying a home in 6,700 minority communities in the United States.

- Expanding affordable housing in underserved communities: The firm’s inaugural $1 billion social bond builds on its strategy to use its business expertise to create opportunity for underserved communities. The bond’s co-managers solely comprise minority- and women-owned businesses, as well as service-disabled, veteran-owned firms.

Grow Black- and Latinx-owned businesses

- Helping small businesses thrive: A $350 million, five-year global commitment underscores our dedication to grow Black-, Latinx- and women-owned businesses among other underserved small businesses, help address the racial wealth divide and create a more inclusive recovery from the COVID-19 pandemic. This ambitious endeavor combines low-cost loans, equity investments and philanthropy and will help reduce barriers to capital for underserved small businesses to support their immediate needs and long-term growth. As part of this commitment, the firm is investing $42.5 million in low-cost loans and philanthropy to expand the Entrepreneurs of Color Fund to more cities in the United States, in collaboration with Local Initiatives Support Corporation and a network of community development financial institutions (CDFI).

- Investing in middle-market businesses: The firm is co-investing up to $200 million alongside Ariel Alternatives and Project Black, an initiative that aims to close the racial wealth gap by investing in middle-market businesses that are minority-owned — or will become minority-owned — to develop a new class of Black and Latinx entrepreneurs.

- Expanding our business with Black and Latinx suppliers: The firm’s internal Buy Black and Latinx Portal, led by Advancing Black Pathways, encourages our lines of business to purchase goods and services from diverse businesses. This year-long campaign is designed to support the firm’s commitment to spend $750 million with Black- and Latinx-owned suppliers over the next five years.

Improve financial health and access to banking in Black and Latinx communities

- Helping 1 million people open low-cost checking or savings accounts: Chase will open 16 new community branches in traditionally underserved neighborhoods and hire 150 community managers by 2022. Branches in Chicago, Dallas, Minneapolis and New York (Harlem) have already been redesigned under this new model. This model has expanded outreach to local small businesses — and to consumers with financial education — and serves as a hub for overall community engagement. Another 100 new branches are being opened in low- to moderate-income communities across the United States as part of the firm’s market expansion initiative. We want to build trust in the communities we serve and become our customers’ primary bank. We offer Secure Banking — a low-cost, no overdraft checking account — for those new to banking, those who have had trouble getting or keeping a bank account, and for Black and Latinx unbanked and underbanked households, thereby expanding access to traditional banking.

- Strengthening diverse-led financial institutions: To promote financial institutions in underserved neighborhoods, we are providing additional access to capital, connections to institutional investors through new products and services, specialty support for Black-led commercial projects, and mentorship and training opportunities. In October 2020, the firm committed to investing $50 million in Black- and Latinx-led minority depository institutions and CDFIs. With $40 million of that investment already committed or deployed to Louisiana-based Liberty Bank, North Carolina-based M&F Bank, New York-based Carver Federal Savings Bank and Los Angeles-based Broadway Federal Bank, the total investment has been increased to $75 million, which could generate access to as much as $750 million in community lending. In addition, the firm’s new Empower money market share class will allow these institutions to develop new revenue streams by serving institutional clients.

Our Sustainability Efforts

Climate change is a critical issue of our time. Reducing greenhouse gas (GHG) emissions — the main cause of climate change — requires collective ambition and cooperation across the public and private sectors.

Coal, oil and natural gas — the primary sources of GHG emissions — have powered the world’s energy economy for many decades, advancing significant economic growth and social development for billions around the world. But our reliance on these resources now threatens the very growth they have enabled.

The challenge we face is significant. While continuing to generate power for all of our needs, big and small — lighting and heating our homes, commuting to work, and charging our phones and computers, as well as operating manufacturing facilities that produce goods used around the world each day — we also need to bring energy to the nearly 800 million people who still don’t have reliable access to electricity. And we need to find a way to do all of these things while setting a path for achieving net-zero emissions by 2050.

The fact is we’re long past debating whether climate change is real. But we need to acknowledge that the solution is not as simple as walking away from fossil fuels. We will need resources such as oil and natural gas until commercial, affordable and low-carbon alternatives can be developed to meet all of our global energy needs. This is where business and government leaders need to focus their time and attention.

While wind and solar technologies have made huge strides, they’re principally deployed for electricity generation. We don’t have clean alternatives for industrial and manufacturing energy needs, for example. Nor do we yet have solutions for heavy transportation, such as trucking and air travel. What’s more, the projected growth of technologies like electric vehicles is going to place huge pressures on the need for rare earth minerals — which also presents geopolitical and environmental challenges.

Policymakers have taken some important steps.

The Paris Agreement is one such success, but we must put a price on carbon. A carbon tax (with a commensurate carbon dividend – directly returned to the people) is an excellent way to dramatically reduce carbon while investing in communities most adversely affected by this much-needed transition. Without a benchmark like this, businesses and economies won’t be able to properly factor the cost of carbon and the benefit of alternatives into their long-term strategic planning and capital investment decisions.

Companies are figuring out how to manage amid these challenges. And many are also dealing with a growing chorus of pressure from customers, regulators, shareholders and activists with strong perspectives on how corporations and other institutions should address climate change.

When we cut through all the noise, here’s what we know to be true:

Traditional energy resources play an essential role in our global economy today. We can agree on the need to make our energy system much less carbon intensive. But abandoning companies that produce and consume these fuels is not a solution. Furthermore, it’s economically counterproductive. Instead, we must work with them.

There’s huge opportunity in sustainable and low-carbon technologies and businesses. While many of these technologies and companies are mature, many more are just getting started — and more will need to be created in the coming decades. In addition, all companies will need capital and advice to help them innovate, evolve and become more efficient while staying competitive in a changing world.

This is why we made a commitment in 2020 to align our financing activities in three carbon-intensive sectors — oil and gas, electric power and automotive manufacturing — with the Paris Agreement.

To do so, we will measure our clients’ carbon performance against sector-based GHG reduction targets that we’re setting for 2030 — with the goal of helping them reduce emissions from their direct operations and, in the case of oil and gas and automotive companies, reduce GHGs from the use of their products.

The key metric we plan to use for evaluating climate performance is carbon intensity, which is a measure of GHG emissions per unit of output. Using intensity will enable us to evaluate the relative efficiency of companies and to adjust for factors such as size, clearly showing which are performing the best (or getting better).

We also want to take advantage of the huge opportunity to support existing and new green companies and to help others lower their carbon footprint — all while advancing economic development and standards of living for people around the world. This includes helping our clients invest in significant and continuous performance improvements, new technologies, alternative energy solutions, and research and development (R&D). Through our recently launched Center for Carbon Transition, clients will have access to information resources, as well as advisory and financing solutions that will help them evolve in a changing world.

We’re also working to make our own company as sustainable as possible. We’ve committed to becoming carbon neutral for the emissions generated to power our buildings, branches and data centers, as well as those related to employee travel. A big focus of our strategy is to generate our own power using solar.

Currently, we have plans to install 40 megawatts of solar capacity across our corporate office buildings in the United States and the United Kingdom. This includes a 14.8-megawatt rooftop and carport solar installation at our corporate campus in Columbus, Ohio, which will produce about 75% of its power needs. We’re also installing 30 megawatts of solar capacity at 900 retail branch locations across the United States, which will provide approximately 35% of each branch’s power needs.

We have an opportunity to make the world a better place for ourselves, for our children and grandchildren, and for all living things that share this planet with us.

II. Lessons from Leadership

Great management is critical to the long-term success of any large organization. Strong management is disciplined and rigorous. Facts, analysis, detail … facts, analysis, detail … repeat. You can never do enough, and it does not end. Complex activity requires hard work and no uneducated guesswork. Test, test, test and learn, learn, learn. And accept failure as a “normal” recurring outcome. Develop great models but understand they are not the answer – judgment has to be involved in matters related to human beings and extraordinary events. You need to have good decision-making processes. Force urgency and kill complacency. Know that there is competition everywhere, all the time. But even if you do all of this well, it is not enough.

1. Enforce a good decision-making process.

A good decision-making process involves having the right people in the room with all information fully shared (all too often I have seen precisely the opposite). There is also the need for constant feedback and follow-up. A bad decision-making process kills. If necessary, review the information over and over – often the answer is simply waiting to be found – and if you don’t have to, don’t rush. While intuition matters, and it can be the final deciding factor, intuition is not guessing – it is usually based on years of experience, hard work and practice.

2. Examine raw data and focus on real numbers.

It is helpful to try to separate and examine actual raw data versus calculated numbers. A few examples will suffice:

You always learn a lot more when you dig deep into the numbers. Look at total car sales, the number of people employed or the actual price of goods compared with calculated data like gross domestic product (GDP), inflation or productivity. For the latter, examine all of the methodologies and assumptions that go into those calculations. For instance, productivity tries to adjust for (or simply sometimes can’t adjust for) new products that are superior to old products, such as smartphones versus dumb phones; similarly, calculations for inflation factor in something called “owners’ equivalent rent,” which generally differs substantially from actual home prices or rental costs.

Applied to corporate operations, examine the details. Many companies look at “net new accounts,” which could be going up dramatically because of prices or marketing – masking attrition or consumers’ dissatisfaction with the product. In detail, look at errors, complaints, attrition, competitors and other new entrants.

Look at market share by customer segment so as not to miss behavior shifts. Frequently, raw data tell a different story from what management may be saying: Too often management teams use the facts to justify what they already think or to celebrate what they believe is a great success.

Being true to these principles requires relentless discipline – which you should expect of us.

3. Understand when analysis is necessary and when it impedes change.

While I am fanatical about detail and multi-year analysis, it’s important to be cautious about its application. Assumptions are frequently involved, and small changes in a few variables can dramatically change an outcome.

Even net present value analysis fails to capture the true value of something after a certain period of time. For instance, people commonly look at the five-year net present value of a customer acquisition, which can mask the true compounding effect of keeping that client for 20 years. And we have often seen net present value analysis fail to capture ancillary benefits (like customer happiness) that can often be more important than the analysis itself.

Sometimes a new product or an investment should simply be considered table stakes – meaning there’s no need to do analysis at all. Think about banks adding the capability of opening new accounts digitally, for example, or maintaining a strong technology infrastructure and adopting new technologies, like cloud or artificial intelligence (AI). These could be life-or-death decisions for a company, so instead of focusing on net present value, the emphasis should be on getting the work done properly, efficiently and quickly.

Bureaucrats can torture people with analysis, stifling innovation, new products, testing and intuition.

In the last section, I go into further detail about how certain analyses fail to guide us to the right answer in public policy – particularly around complex issues like healthcare, job creation, mortgage markets and infrastructure.

4. Before conducting an important analysis, assess all relevant factors involved.

I frequently see people trying to understand a complex situation without considering all the factors involved. In the final section, I attempt to analyze China as a strategic competitor. It’s critical to weigh all the factors: cultural, psychological and historical. Also, what are the legal factors, and how is the rule of law applied? What is the country’s situation with raw materials? What is the country’s geography and relationship with its neighbors? It is important to lay out all the important variables before you start an assessment to ensure that they are all carefully reviewed and that one’s judgment is not clouded early on by overfocusing on just a few issues.

In business, this type of assessment should also be applied to your competitors and to those you deem to be future competitors, as well as to your own strengths and weaknesses. In the next section, I describe the evolving competitive landscape for banks.

5. Always deal with reality.

In business, as in life, we must deal with both certainty and uncertainty. A simple look at history and our economic past illustrates the rather unpredictable nature of things. As a result, at the firm we try to look at all the possibilities, as well as their probabilities. For example, we conduct well over 100 stress tests each week to make sure we are prepared for what we are not predicting. We even evaluate the laws and regulations we live under today and project how they might be interpreted 10 years from now – we call this “reinterpretation risk.” We look at a broad range of possibilities and probabilities to ensure that we understand, as best as we can, all of the possible outcomes – recognizing that we are not trying to make a forecast with certainty. Sometimes the action you take may not be the one that gives you the best outcome but the one that gives you a good outcome and reduces the possibilities of bad outcomes.

It also is often very difficult to capture the inflection points in the economy. Most people imagine the future as being roughly equivalent to the past, give or take a bit. However, we know there are significant inflection points, which are sometimes easy to see in hindsight but almost impossible to predict.

While we also try to keep things as streamlined as possible, making things simpler than they really are is equally flawed. Too many times people seek simple, cookie-cutter solutions that sound good but just don’t work. For example, class size in schools matters but not necessarily in all types of classes. In Vietnam, when a major city once had a rat population problem, the government devised what it thought was an easy, foolproof solution: Pay people to kill rats. All people had to do was bring in a rat tail to be paid. What the government didn’t consider was that people would breed rats for a supply of rat tails to sell. (All compensation schemes should be continuously re-evaluated.)

6. Remain open to learning how to become a better leader.

In addition to the above thoughts on analysis, assessment and good decision making, some softer leadership lessons are equally important.

As companies get bigger and more complex, leaders need to be more like coaches and conductors than players. If CEOs are running a smaller business, they can literally be involved in virtually everything and make most of the decisions – they often rely on traditional command-and-control tactics. This approach does not work as companies get bigger – the CEOs simply cannot be involved in every major decision. Command and constant feedback may be better than command and control. Here is where leaders would be better off providing clear direction and letting people do their job, including making mistakes along the way. Soft power – essentially trust and maturity – may become more important than hard power. Soft power creates respect among team members, with the coach offering honest assessment and support while allowing flexibility. Here the boss makes fewer but tougher decisions, such as removing people – when it must be done – and even then, it is handled respectfully. People will give to the best of their ability for leaders they respect and who they know are trying to help them succeed.

Respect and learn from your people. Managers and leaders get spread pretty thin. While they should have a wide grasp of many subjects, they could not possibly know everything their people know. Leaders should continually be learning from their people. They should go to a sales conference and ask lots of questions of their salespeople. Gather technology people in the room with branch managers and ask, “How are things working?” Taking a road trip should not be only for the purpose of showing the flag but also for learning from your employees and customers.

Have curiosity. It’s important to ask questions to try to understand varying points of view. Be willing to change your mind. Read everything. Don’t defend decisions of the past. Leaders should be happy when their people prove them wrong. Do not have a rigid mindset. And do not be complacent.

Skip hierarchy. If everything in a large organization must go up and down the hierarchical ladder, bureaucratic arteriosclerosis along with CYA sets in, and that company’s life expectancy is substantially shortened. It should be routine that data, memos and ideas are shared – skipping hierarchies – and aren’t vetted by all in the chain of command. This makes people more responsible for what they are doing, improves the dissemination of new information and new ideas, and speeds things up overall. In addition, it’s good to have a few mavericks who are not afraid to shake things up. The ones who challenge authority or convention often get far more done than the ones who go along to get along. Collaboration is wonderful, but it can be overdone.

Act at the speed of relevance. When leaders have plenty of time to make decisions, they should analyze all factors over and over – take the necessary time, as choices can be hard to reverse. And there are other decisions that are more like “battlefield promotions” where there’s no luxury of time, and, in fact, going slow may make things much worse. I’ve also seen people take a tremendous amount of time to make an unimportant decision, which just wastes time and slows things down.

In business, some decisions should be made carefully – for instance, putting the right people in the right job. But others, such as making pricing decisions, dealing with customer problems and handling reputational issues, must be done quickly, for these problems do not age well.

The Importance of Developing Leaders [Reprinted from my 2009 Letter to Shareholders]

Earlier in this section, I mentioned that my number one priority is to put a healthy and productive succession process in place. As I will be increasingly focused on this process, I would like to share my thoughts about the essential qualities a leader must have, particularly as they relate to a large multinational corporation like JPMorgan Chase.

Leadership is an honor, a privilege and a deep obligation. When leaders make mistakes, a lot of people can get hurt. Being true to oneself and avoiding self-deception are as important to a leader as having people to turn to for thoughtful, unbiased advice. I believe social intelligence and “emotional quotient,” or EQ, matter in management. EQ can include empathy, clarity of thought, compassion and strength of character.

Good people want to work for good leaders. Bad leaders can drive out almost anyone who’s good because they are corrosive to an organization; and since many are manipulative and deceptive, it often is a challenge to find them and root them out.

At many of the best companies throughout history, the constant creation of good leaders is what has enabled the organizations to stand the true test of greatness — the test of time.

Below are some essential hallmarks of a good leader. While we cannot be great at all of these traits — I know I’m not — to be successful, a leader needs to get most of them right.

Discipline

This means holding regular business reviews, talent reviews and team meetings and constantly striving for improvement — from having a strong work ethic to making lists and doing real, detailed follow-up. Leadership is like exercise; the effect has to be sustained for it to do any good.

Fortitude

This attribute often is missing in leaders: They need to have a fierce resolve to act. It means driving change, fighting bureaucracy and politics, and taking ownership and responsibility.

High Standards

Leaders must set high standards of performance all the time, at a detailed level and with a real sense of urgency. Leaders must compare themselves with the best. Huge institutions have a tendency toward slowing things down, which demands that leaders push forward constantly. True leaders must set the highest standards of integrity — those standards are not embedded in the business but require conscious choices. Such standards demand that we treat customers and employees the way we would want to be treated ourselves or the way we would want our own mother to be treated.

Ability to Face Facts

In a cold-blooded, honest way, leaders emphasize the negatives at management meetings and focus on what can be improved (of course, it’s okay to celebrate the successes, too). All reporting must be accurate, and all relevant facts must be reported, with full disclosure and on one set of books.

Openness

Sharing information all the time is vital — we should debate the issues and alternative approaches, not the facts. The best leaders kill bureaucracy — it can cripple an organization — and watch for signs of politics, like sidebar meetings after the real meeting because people wouldn’t speak their mind at the right time. Equally important, leaders get out in the field regularly so as not to lose touch. Anyone in a meeting should feel free to speak his or her mind without fear of offending anyone else. I once heard someone describe the importance of having “at least one truth-teller at the table.” Well, if there is just one truth-teller at the table, you’re in trouble — everyone should be a truth-teller.

Setup for Success

An effective leader makes sure all the right people are in the room — from Legal, Systems and Operations to Human Resources, Finance and Risk. It’s also necessary to set up the right structure. When tri-heads report to co-heads, all decisions become political — a setup for failure, not success.

Morale-Building

High morale is developed through fixing problems, dealing directly and honestly with issues, earning respect and winning. It does not come from overpaying people or delivering sweet talk, which permits the avoidance of hard decision making and fosters passive-aggressive behaviors.

Loyalty, Meritocracy and Teamwork

While I deeply believe in loyalty, it often is misused. Loyalty should be to the principles for which someone stands and to the institution: Loyalty to an individual frequently is another form of cronyism. Leaders demand a lot from their employees and should be loyal to them — but loyalty and mutual respect are two-way streets. Loyalty to employees does not mean that a manager owes them a particular job. Loyalty to employees means building a healthy, vibrant company; telling them the truth; and giving them meaningful work, training and opportunities. If employees fall down, we should get them the help they need. Meritocracy and teamwork also are critical but frequently misunderstood. Meritocracy means putting the best person in the job, which promotes a sense of justice in the organization rather than the appearance of cynicism: “Here they go again, taking care of their friends.” Finally, while teamwork is important and often code for “getting along,” equally important is an individual’s ability to have the courage to stand alone and do the right thing.

Fair Treatment

The best leaders treat all people properly and respectfully, from clerks to CEOs. Everyone needs to help everyone else at the company because everyone’s collective purpose is to serve clients. When strong leaders consider promoting people, they pick those who are respected and ask themselves, Would I want to work for him? Would I want my kid to report to her?

Humility

Leaders need to acknowledge those who came before them and helped shape the enterprise — it's not all their own doing. There's a lot of luck involved in anyone's success, and a little humility is important. The overall goal must be to help build a great company — then we can do more for our employees, our customers and our communities.

III. Banks’ Enormous Competitive Threats — from Virtually Every Angle

To fairly assess the competitive landscape for banks, you must fairly evaluate their strengths and weaknesses to deal with both the current competition and evolving competition. Banks have significant strengths – brand, economies of scale, profitability, and deep roots with their customers and within their communities. Many companies, including banks, have flaws of their own making – usually due to bureaucracy, complacency and lack of a deep competitive spirit. Banks have other weaknesses, born somewhat out of their success – for example, inflexible “legacy systems” that need to be moved to the cloud if they are to remain competitive. Banks are also required to deal with extensive regulations, which can hinder new competition and/or create an opening for both existing and evolving competitors. Banks fiercely compete with each other and now face fierce competition from multiple vectors.

Banks already compete against a large and powerful shadow banking system. And they are facing extensive competition from Silicon Valley, both in the form of fintechs and Big Tech companies (Amazon, Apple, Facebook, Google and now Walmart), that is here to stay. As the importance of cloud, AI and digital platforms grows, this competition will become even more formidable. As a result, banks are playing an increasingly smaller role in the financial system.

I am completely in favor of open competition, and much of the competition that I cover in this section will be good for America. One of the necessities for a healthy economy, and one at the core of America’s success, is a strong, vibrant financial system. The disciplined allocation of capital, and the constant search for new opportunities for capital, is critical to growth (a corollary of the free and intelligent movement of capital is the free movement of human talent, which, ultimately, may be even more important). America’s financial system is the best the world has ever seen, from our regulatory system and rule of law to exchanges, venture capital and private capital, banks and shadow banks. As our system changes, our government and regulators need to understand that maintaining the vibrancy, safety and soundness of this system is critical – and this includes maintaining a relatively fair and balanced playing field. While I am still confident that JPMorgan Chase can grow and earn a good return for its shareholders, the competition will be intense, and we must get faster and be more creative.

1. Banks are playing an increasingly smaller role in the financial system.

In the chart below, you will see that U.S. banks (and European banks) have become much smaller in size relative to multiple measures, ranging from shadow banks to fintech competitors and to markets in general.

Read footnoted information here

Whether you look at the chart above over 10 or 20 years, U.S. banks have become much smaller relative to U.S. financial markets and to the size of most of the shadow banks. You can also see the rapid growth of payment and fintech companies and the extraordinary size of Big Tech companies. (As an aside, capital and global systemically important financial institution (G-SIFI) capital rules were supposed to reflect the economy’s increased size and banks’ reduced size within the economy. This simply has not happened in the United States.)

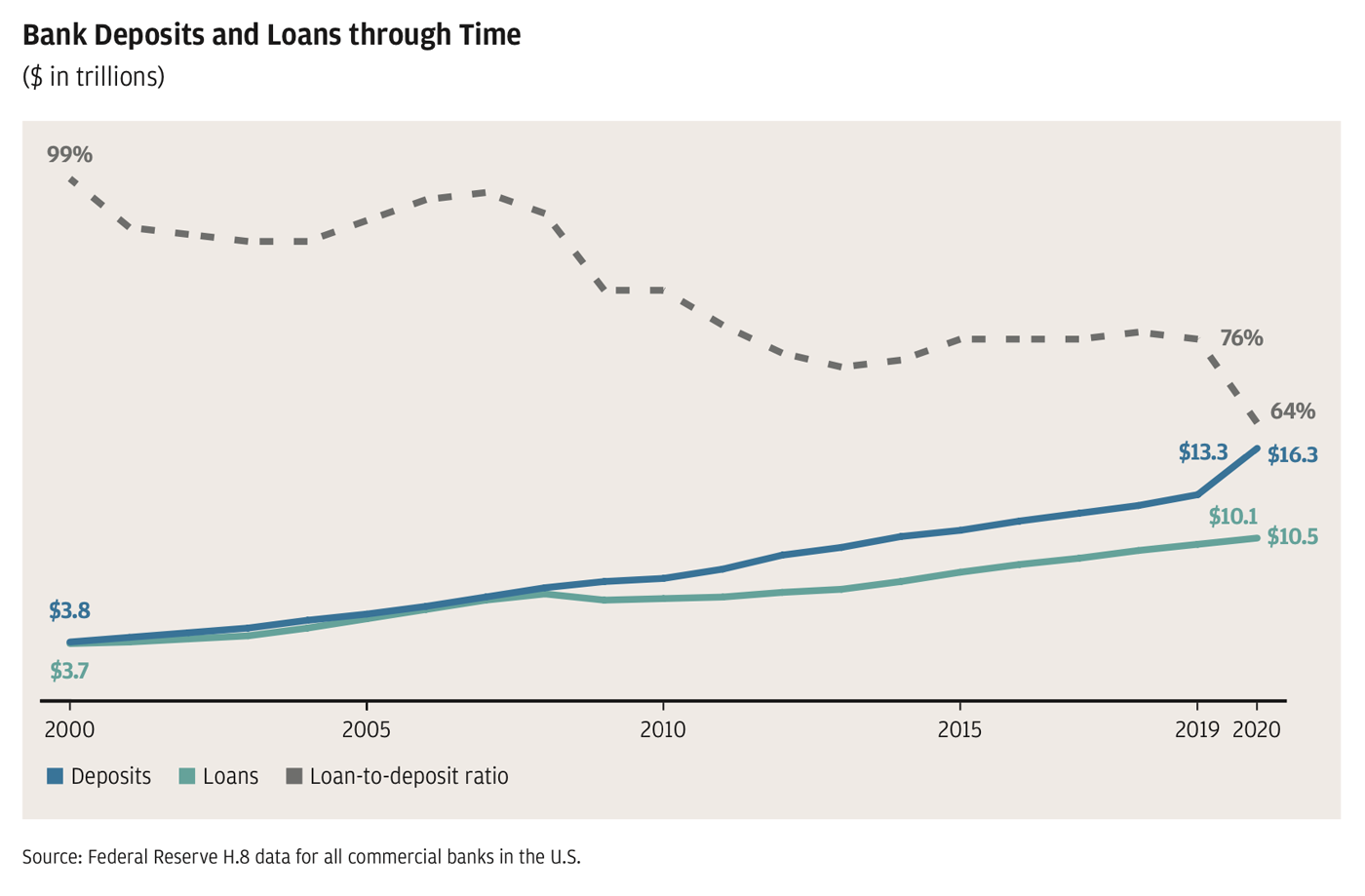

Some regulators will look at the chart above and point out that risk has been moved out of the banking system, which they wanted and which clearly makes banks safer. That may be true, but there is a flip side – banks are reliable, less-costly and consistent credit providers throughout good times and in bad times, whereas many of the credit providers listed in the chart above are not. More important, transactions made by well-controlled, well-supervised and well-capitalized banks may be less risky to the system than those transactions that are pushed into the shadows.

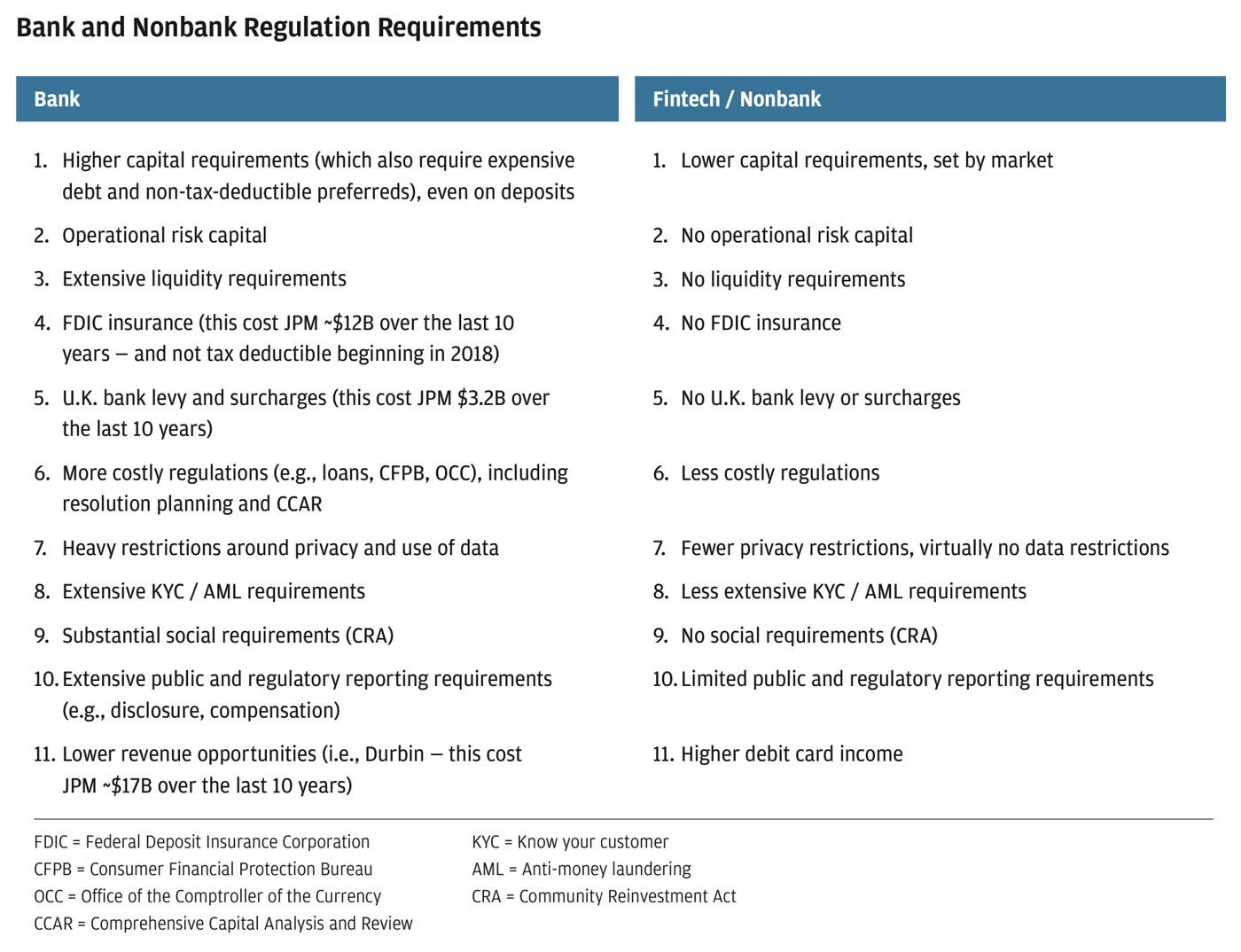

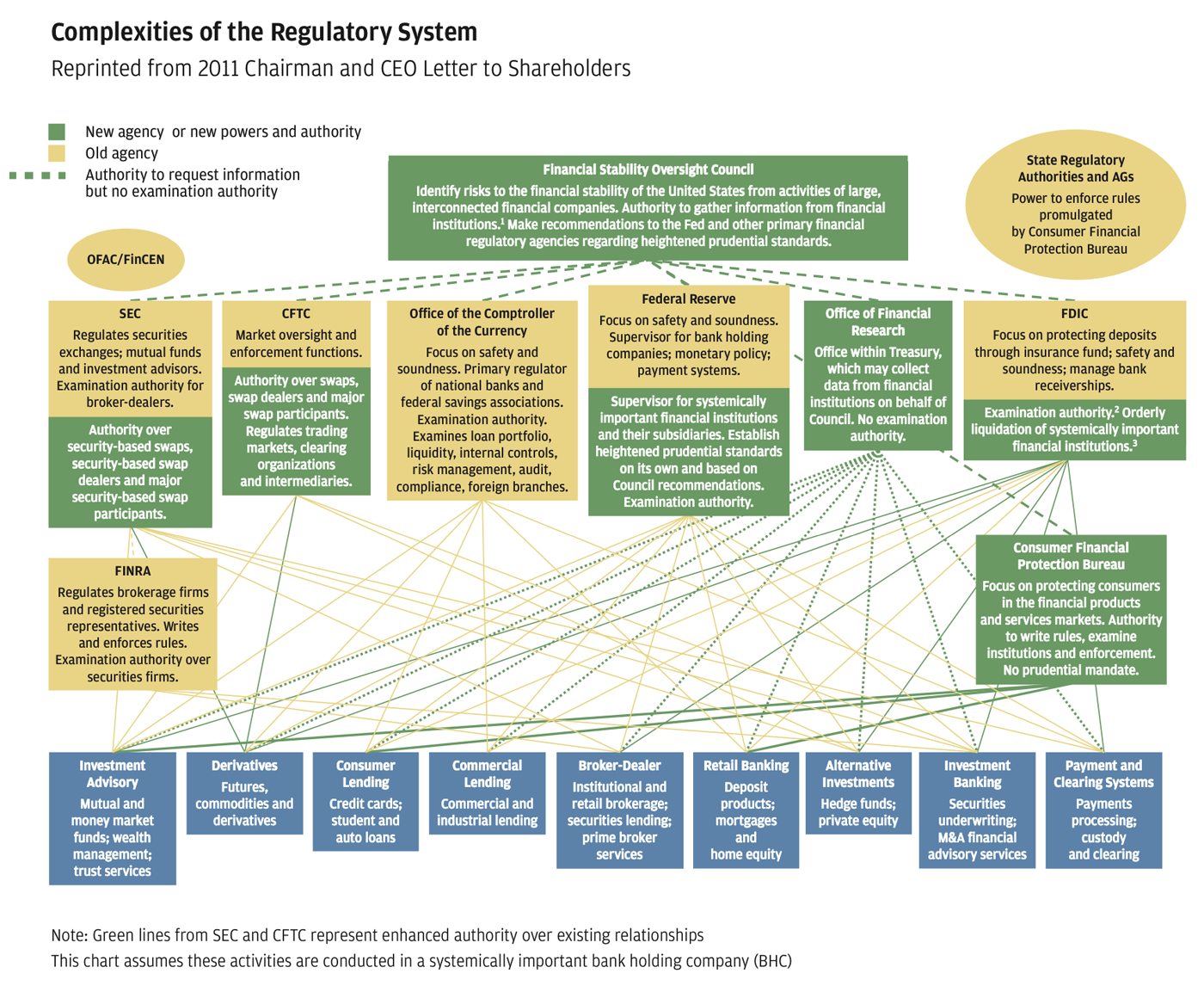

2. The growth in shadow and fintech banking calls for level playing field regulation.

The chart below shows the potential regulatory differences between being a bank and being a nonbank or a fintech company – though this varies for each type of company on each item depending upon its legal and regulatory status. In some cases, these regulatory differences may be completely appropriate, but certainly not in all cases.

When I make a list like this, I know I will be accused of complaining about bank regulations. But I am simply laying out the facts for our shareholders in trying to assess the competitive landscape going forward.

It is completely clear that, increasingly, many banking products, such as payments and certain forms of deposits among others, are moving out of the banking system. In addition, lending in many forms – including mortgage, student, leveraged, consumer and non-credit card consumer – is moving out of the banking system. Neobanks and nonbanks are gaining share in consumer accounts, which effectively hold cash-like deposits. Payments are also moving out of the banking system, in merchant processing and in debit or alternative payment systems.

We believe that many of these new competitors have done a terrific job in easing customers’ pain points and making digital platforms extremely simple to use. But growth in shadow banking has also partially been made possible because rules and regulations imposed upon banks are not necessarily imposed upon these nonbanks. While some of this may have been deliberate, sometimes the rules were accidentally calibrated to move risk in an unintended way. We should remember that the quantum of risk may not have changed – it just got moved to a less-regulated environment. And new risks get created. While it is not clear that the rise in nonbanks and shadow banking has reached the point of systemic risk, this trend is accelerating and needs to be assiduously monitored, which we do regularly as part of our own business.

A few items need further explanation. On capital requirements, you should always remember that the market determines this level, not regulators, and to the extent that capital requirements in one entity are much higher than another, activities will move. Ironically, because standardized capital and G-SIFI capital do not recognize credit risk, banks have a peculiar incentive to hold higher risk credit rather than lower risk credit. All companies have operational risk, and most companies absorb operating losses through earnings. Banks are required to hold substantial capital against this risk. (I’m not debating that there is operational risk.) And because of the Durbin Amendment, if a bank has a customer with a small checking account who spends $20,000 a year on a debit card, the bank will only receive $120 in debit revenue – while a small bank or nonbank would receive $240. This difference may determine whether you can even compete in certain customer segments. It’s important to note that while some of the fintechs have done an excellent job, they may actually be more expensive to the customer.

Finally, it’s important to point out that not only has private credit been moving to the private markets but so have companies themselves. The number of public companies in the United States has been dropping dramatically over the past two decades, which has corresponded to an even larger increase in the number of private companies. Following its peak at 8,000 in 1997, the number of public companies is now around 6,000, and if you exclude non-operating companies, such as investment funds and trust companies, the decline is even more dramatic. This is worthy of serious study. The reasons are complex and may include factors such as onerous reporting requirements; higher litigation expenses; annual shareholder meetings focused on matters that most shareholders view as frivolous or inappropriate for company actions; costly regulations; less compensation flexibility; and heightened public scrutiny. It’s incumbent upon us to figure out why so many companies and so much capital are being moved out of the transparent public markets to the less transparent private markets and whether this is in the country’s long-term interest.

We need competition – because it makes banking better – and we need to manage the emerging risks with level playing field regulation in a way that ensures safety and soundness across the industry.

3. AI, the cloud and digital are transforming how we do business.

We cannot overemphasize the extraordinary importance of new technology in the new world. Today, all technology is built “cloud-enabled,” which means the applications and their associated data can run on the cloud. This brings many extraordinary advantages, but the one that I’d like to spotlight is the immediate ability to access data and associated machine learning with virtually unlimited compute power. Essentially, in the cloud, you can “access” hundreds of databases and deploy machine learning in a split second – something mainframes and legacy systems and databases simply cannot do. To go from the legacy world to the cloud, applications not only have to be “refactored,” but, more important, data also must be “re-platformed” so it is accessible. This availability of data – and banks have a tremendous amount of data – makes data enormously valuable and digitally accessible. All of this work takes time and money, but it’s absolutely essential that we do it.

We already extensively use AI, quite successfully, in fraud and risk, marketing, prospecting, idea generation, operations, trading and in other areas – to great effect, but we are still at the beginning of this journey. And we are training our people in machine learning – there simply is no speed fast enough.

4. Fintech and Big Tech are here…big time!

Fintech companies here and around the world are making great strides in building both digital and physical banking products and services. From loans to payment systems to investing, they have done a great job in developing easy-to-use, intuitive, fast and smart products. We have spoken about this for years, but this competition now is everywhere. Fintech’s ability to merge social media, use data smartly and integrate with other platforms rapidly (often without the disadvantages of being an actual bank) will help these companies win significant market share.

Importantly, Big Tech (Amazon, Apple, Facebook, Google – and, as I said, now I’d include Walmart) is here, too. Their strengths are extraordinary, with ubiquitous platforms and endless data. At a minimum, they will all embed payments systems within their ecosystems and create a marketplace of bank products and services. Some may create exclusive white label banking relationships, and it is possible some will use various banking licenses to do it directly.

Though their strengths may be substantial, Big Tech companies do have some issues to deal with that may, in fact, slow them down. Their regulatory environment, globally, is heating up, and they will have to confront major issues in the future (banks have faced similar scrutiny). Issues include data privacy and use, how taxes are paid on digital products, and antitrust and anticompetitive issues – such as favoring their own products and services over others on their platform and how they price products and access to their platforms. In addition, Big Tech will have very strong competition – not just from JPMorgan Chase in banking but also from each other. And that competition is far bigger than just banking – Big Tech companies now compete with each other in advertising, commerce, search and social.

5. JPMorgan Chase is aggressively adapting to new challenges.

As tough as the competition will be, JPMorgan Chase is well-positioned for the challenge. But our eyes are wide open as the landscape changes rapidly and dramatically. We have an extraordinary number of products and services, a large, existing client base, huge economies of scale, a fortress balance sheet and a great, trusted brand. We also have an extraordinary amount of data, and we need to adopt AI and cloud as fast as possible so we can make better use of it to better serve our customers. We need to make our extraordinary number of products and services a huge plus by improving ease of use and reducing complexity. We need to move faster and bolder in how we attack new markets while protecting our existing ones. Sometimes new markets look too small or appear not to be critical to our customer base – until they are. We intend to be a little more aggressive here.

While we will argue for a level playing field, both in terms of how products and services are treated by regulators and possibly how competition should be treated across platforms, we are not relying on much to change. So we will simply have to contend with the hand we are dealt and adjust our strategies as appropriate.

We have mentioned that our highest and best use of capital is to expand our businesses, and we would prefer to make great acquisitions instead of buying back stock. We are somewhat constrained by how much we can grow our balance sheet because our capital charges will grow with our size, so sometimes buying back stock may still be the best option. But acquisitions are in our future, and fintech is an area where some of that cash could be put to work – this could include payments, asset management, data, and relevant products and services.

We will continue to do everything in our power to make JPMorgan Chase successful – and are confident we can do so.

IV. Specific Issues Facing Our Company

In this section, I review and analyze some of the current critical issues that affect our company.

1. Cyber risk remains a significant threat.

We cannot overemphasize the importance of cyber risk, not just to our bank (we spend more than $600 million a year on cybersecurity) but also to our customers, countries, economies and critical industries (i.e., telecom and power). We have pointed out to our shareholders before that having disciplined cyber hygiene is almost as important as the money you spend. Threats to our cybersecurity need urgent attention from our government as issues of national security and impediments to trade. Governments should build on prior agreements in the United Nations, recognizing the applicability of international law to cyberspace and enforcing obligations to hold bad actors accountable. Acknowledging that governments and their regulatory agencies are prime targets for cyber criminals, these agencies need to provide transparency to those affected by incidents (e.g., financial institutions and others that hold sensitive data), invest in the uplift to cybersecurity, and adopt safe and sound practices for data protection and handling.

Much of our extraordinary cyber capabilities are also used to train and protect our customers, particularly in the areas of risk and fraud.

2. Brexit was finally accomplished — but uncertainties linger.

Brexit was accomplished, but many issues still need to be negotiated. And in those negotiations, Europe has had, and will continue to have, the upper hand. In the short run (i.e., the next few years), this cannot possibly be a positive for the United Kingdom’s GDP – the effect after that will be completely based upon whether the United Kingdom has a comprehensive and well-executed strategic plan that is acceptable to Europe. Included among the unresolved questions is how financial services will operate. London has been a major financial center that, under all laws and regulations, could conduct business throughout Europe. For most of us, the bulk of our operations (i.e., risk, compliance, audit, legal, regulatory, market-making, investment banking, research and asset management) were performed centrally in London. It was hugely efficient for all of Europe – and for financial services companies as well. London is a magnificent place to do business in terms of the rule of law, human capital, technology, transportation, language and many other facets. But future financial regulations were left uncertain in Brexit; and it is clear that, over time, European politicians and regulators will make many understandable demands to move functions into European jurisdictions. Because of this – and because of strong European efforts to compete with London – Paris, Frankfurt, Dublin and Amsterdam will grow in importance as more financial functions are performed there. Even so, few winners are likely to emerge from this fragmentation.

During this transition, our costs (most of which will probably be passed on to customers in one form or another) will go up as functions become duplicated. We may reach a tipping point many years out when it may make sense to move all functions that service Europe out of the United Kingdom and into continental Europe. But London still has the opportunity to adapt and reinvent itself, particularly as the digital landscape continues to revolutionize financial services. Innovation is key to preparing for doing the business of tomorrow versus relying on the shifting ways of the past.

3. New accounting requirements affect reserve reporting but not how we run our business.

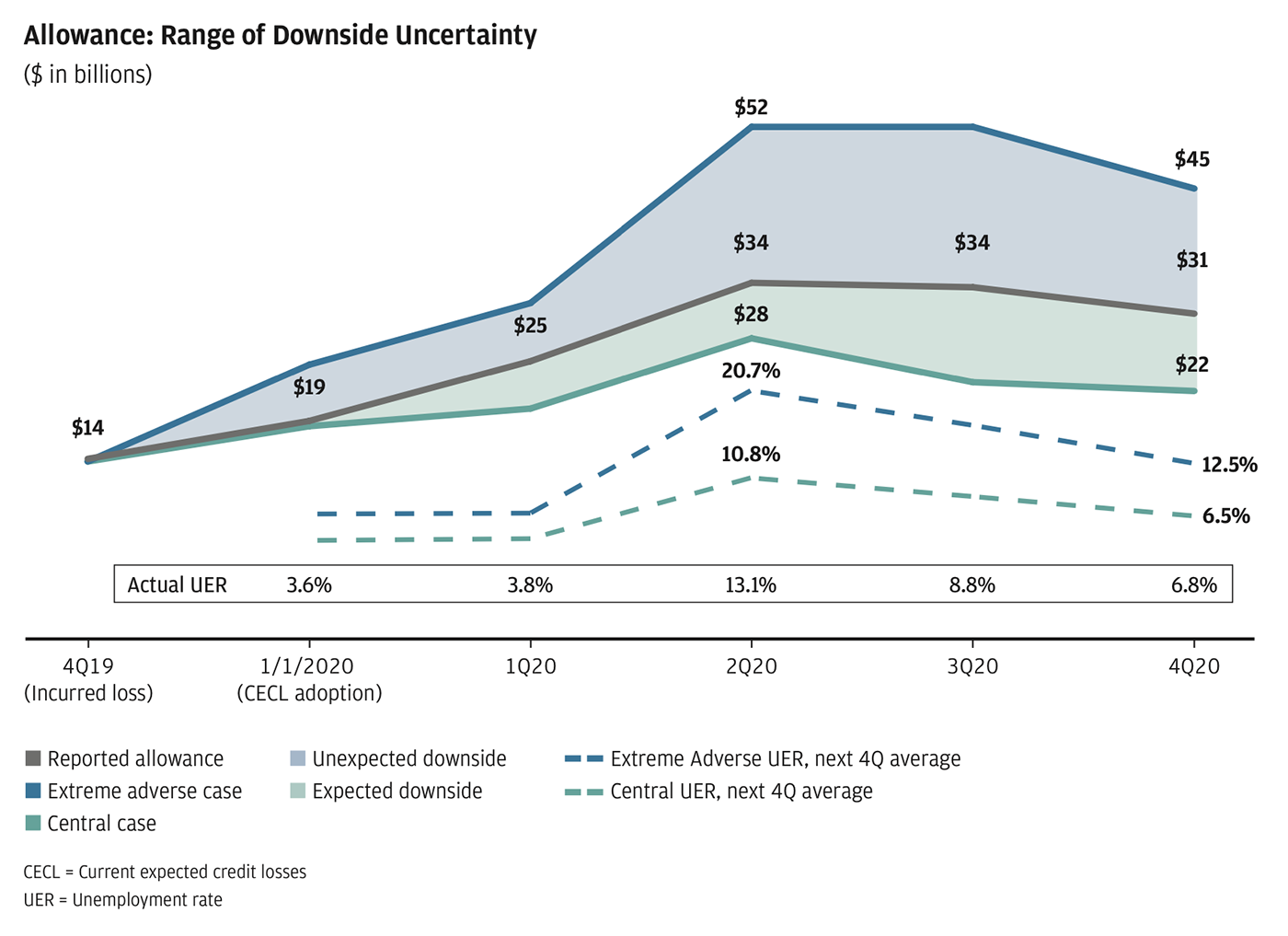

A new loan loss reserving method called the current expected credit losses (CECL) standard was adopted by large financial institutions, effective January 1, 2020. To oversimplify, there were two main changes. First, you must reserve for expected credit losses over the full remaining expected life of the loan, whereas in the past, we reserved for losses that had already been incurred using a forecast over a loss emergence period, for example the ensuing 12 months or so for credit cards. Second, you were to incorporate different reasonable and supportable macroeconomic forecasts (for multiple scenarios) in estimating losses. Given the benign macroeconomic environment when this new CECL standard was adopted, it increased reserves by only $4.3 billion, which was primarily attributed to moving to lifetime loss coverage for Card, with only a small amount of reserves for the probability of a far worse economic environment.

Hundreds of variables go into the scenarios and calculations shown in the chart above. During periods of stress, the firm leaned more heavily to the downside to reflect uncertainties not fully captured by the scenarios themselves. Uncertainties included a substantial drop in headline employment without corresponding job creation, the degree of permanent job losses, the extent and timing of federal government assistance, unknowns around vaccine efficacy against new virus strains, and the potential for economic scarring from changes in consumer behavior and the recovery of directly impacted sectors.

The best way to look at this is to analyze our loan loss reserves as of December 31, 2020. Our central case is essentially our baseline forecast (and is roughly similar to the Federal Reserve’s current forecast at the time), which would have unemployment over the ensuing 12 months at 6.5%. If we reserved to this case, our reserves would total $22 billion. But we run multiple scenarios – one of which is an extreme adverse case. This worst case, which is slightly more severe than the Federal Reserve’s extreme adverse case, would have unemployment over the ensuing 12 months at 12.5% (among other variables). If we reserved as if this scenario had a 100% chance of happening, we would require $45 billion in reserves. After probability weighting multiple scenarios, we ended the year with $31 billion in reserves.

Clearly in turbulent times, these scenarios and the probabilities assigned to them are highly uncertain and volatile. The following are also clear and extremely important: The firm earns almost $50 billion +/- pre-provision profit annually; it is able to easily handle large increases in reserves; and we could easily have done substantially more while maintaining high capital and high liquidity. This is also why we saw no reason to cut our dividend. If, however, the worst-case scenario had happened (which means it could have gotten even worse from there), we might have cut our dividend to retain capital out of prudence.

Importantly, CECL does not change risk management or the way we run the company. We have been lending, and will continue to lend, to our clients and customers throughout the pandemic with prudent risk management. Our credit risk decisions and broader risk appetite are mostly driven by our clients’ needs and market conditions rather than solely by reserve methodology. While reserve levels are an estimate reflecting management’s expectations of credit losses at the balance sheet date, they may not reflect the amount of losses ultimately realized.

4. While we disbanded Haven, we will continue to build on what we learned.

Although the United States has some of the best healthcare in the world (i.e., doctors, pharmaceutical care and innovation) and many people from other countries come here when they need serious medical attention, the problems associated with healthcare are serious, rampant and obvious. Our costs are more than twice those of the developed world without justification by better outcomes. There is no transparency in pricing, with patients legitimately complaining of hidden costs. And chronic care is not necessarily managed properly. More than 30 million Americans are uninsured, and we are falling short in basic wellness.

Amazon, Berkshire Hathaway and JPMorgan Chase set up Haven to address some of these problems, and, in the process, we learned a lot about how the healthcare system could be improved. Although we decided to disband Haven, JPMorgan Chase will continue to build on what we learned. We will invest in healthcare innovation and other approaches to improve the health and well-being of our employees and address this critical national issue. More details will be shared as we progress.

V. COVID-19 and the Economy

Within days of realizing that COVID-19 was a global pandemic that would virtually close down large parts of the world’s economies, the U.S. government moved with unprecedented speed. Fortunately, banks were part of the solution – unlike in the Great Recession. And unlike the Great Recession, the U.S. economy was actually in good shape going into the COVID-19 recession. Though there are many differences, it’s instructive to compare the recovery from the Great Recession with the expected recovery from the COVID-19 recession.

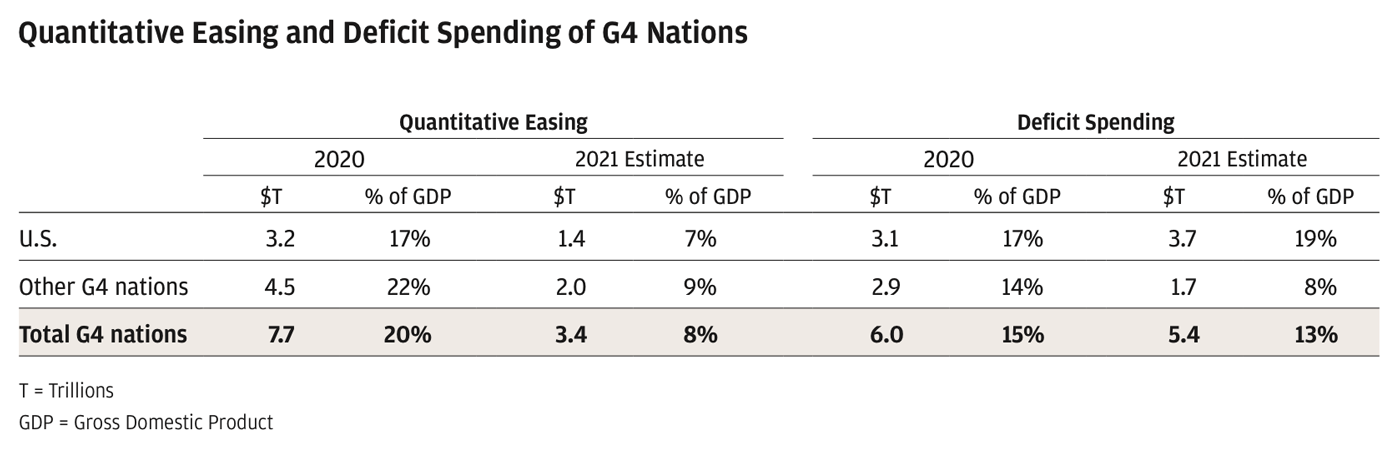

1. Bold action by the Fed and the U.S. government effectively reversed financial panic.

The Federal Reserve (critically, with the support of the U.S. Treasury) immediately rolled out facilities that financed Treasuries, corporate bonds, mortgage-backed securities and other securities that effectively reversed the financial panic taking place. A full-blown financial crisis would have made the COVID-19 recession far worse, deeper and longer. Markets reacted extremely positively, and companies, over the next nine months, raised an unprecedented $2 trillion in debt and equity at good prices, dramatically improving their financial condition and balance sheets.

Congress, importantly, also took immediate action to provide fiscal stimulus, the Coronavirus Aid, Relief, and Economic Security Act, also known as the CARES Act, totaling $2.2 trillion. This largely consisted of stimulus payments to individuals, enhanced unemployment insurance and loans, which could be forgiven, to small businesses. Please see the following sidebar for more detail on the Paycheck Protection Program.

Suffice it to say while real damage was done, the size and scope of these programs dramatically reversed the deterioration of the economy and unemployment, which hit 14.8% in April 2020 but made steady progress back to 6.7% by the end of the year – though this number underrepresents the damage that was done because of the large deterioration in labor force participation and the potential permanent loss of many small businesses.

One last important point: The speed and breadth of the programs were critical, and there is no way they could have been done perfectly. While it always makes sense to do a thorough postmortem review and to properly punish those who deliberately misuse emergency government programs, we should try to avoid excessive finger-pointing.

The Paycheck Protection Program, while not perfect, was a tremendous achievement.